Personal Wealth Management / Market Analysis

1997 and 2015: History Rhymes, But Doesn’t Exactly Repeat

Today's Emerging Markets resembles that of the 1997/1998 Asian currency crisis, but the differences make an exact repeat unlikely.

Are we headed for Asian Contagion the Sequel? In 1997/1998 a currency crisis sent the Asia/Pacific region into recession and forced three countries to head to the IMF with hat in hand. Today, amid slowing growth, rising debt, falling currencies, contracting foreign reserves and net outward capital flows, some suggest Emerging Markets are doomed to repeat history, possibly reverberating globally. But while this period does seem similar to that time generally, the specifics differ. A deeper look at the current Emerging Markets landscape suggests a replay of 1997/1998's Asian financial crisis is unlikely, and that troubles in some developing countries don't threaten the global expansion.

After booming throughout the 2003-2007 bull market, Emerging Markets (EM) have mostly slumped since. While overall EM economic growth has been nicely positive in this expansion, some (mostly commodity-heavy) EMs are now floundering-and many fear a debt crisis may develop. EM debt has increased in the last decade, growing from $4 trillion in 2004 to over $18 trillion today, according to the International Monetary Fund. Much of this debt is US dollar denominated. With EM currencies weakening against the US dollar lately, this debt is now more expensive to service. Some fear defaults will follow and ripple through EM economies. Compounding the fear is the fact some commodity-dependent Emerging Market countries are in recession (Brazil and Russia), likely making it even harder for firms there to honor outstanding debt.

The rising debt resembles the late 1990s, when Emerging Asian debt grew quickly. Back then, many nations pegged their currencies to the dollar and the resulting stable exchange rates attracted foreign investment and reduced interest rates. Many countries took advantage, issuing cheap US-dollar denominated debt to fund growth. Governments and corporates ran up big tabs. The economic boom led to over-investment, and when the Japanese yen weakened in the late 1990s, markets smelled trouble, betting countries couldn't survive the triple whammy of high debt, faltering growth and defending currency pegs.

The weak yen forced these countries, which trade heavily with Japan, to sell foreign exchange reserves and boost their own currencies to maintain their dollar pegs-an inherently unsustainable situation. Speculators attacked the Thai baht first, betting the government would deplete reserves and be forced to devalue. They were right, and markets then started sniffing out the next shoes to drop, pressuring currencies throughout Emerging Asia. Indonesia and South Korea also devalued. Both, along with Thailand, took IMF bailouts as the devaluations made dollar-denominated debt impossible to service. Singapore, Malaysia, Hong Kong and others also hit the skids, though they ultimately avoided the worst, and Asia/Pacific economies spent 1998 in recession.

Today, it's true the dollar is about as strong as it was then, and many developing countries have taken on a lot of dollar-denominated debt. But there are big differences between 1990s Asia and the current EM landscape, making a 1997 crisis repeat less likely. Arguably, the biggest contrast between now and then is that-with the exception of China and Hong Kong-virtually no developing nation still pegs their currency to the dollar. Malaysia has a fixed float, but most others trade freely. This is a direct result of the 1997/98 crisis, as countries learned the potential costs of pegged currencies-the huge devaluation shock that follows having to abandon the pegs-far outweighs the benefits. Instead, many Emerging Markets now have flexible or managed exchange rates (which fluctuate based on market forces, but central banks still influence them to some extent), including countries such as Brazil and Russia whose economies are struggling the most these days among Emerging Markets. Huge, sudden and destabilizing devaluations, similar to what occurred in 1997 and 1998 when governments abandoned their currency pegs overnight, simply can't happen in Emerging Asia today. There aren't pegs to abandon. Of course, non-pegged currencies can still depreciate (and they already have for many EMs), but these moves are less sudden and severe, and markets have time to adjust.

The perils of pegged currencies aren't the only lessons EMs learned in the late 1990s. Most Emerging Markets have much bigger foreign-currency reserves than they did then. According to the World Bank, China had $3.9 trillion in total reserves at 2014's close, dwarfing the $111.7 billion they had in 1996, before the late 1990s crisis erupted. Exhibit 1 shows other developing countries' reserves have grown similarly. Countries now have lots of cushion for depreciating currencies, and this makes a crisis even less likely to happen.

Exhibit 1: Total Reserves, 1996 versus 2014

Source: The World Bank, as of 10/22/2015.

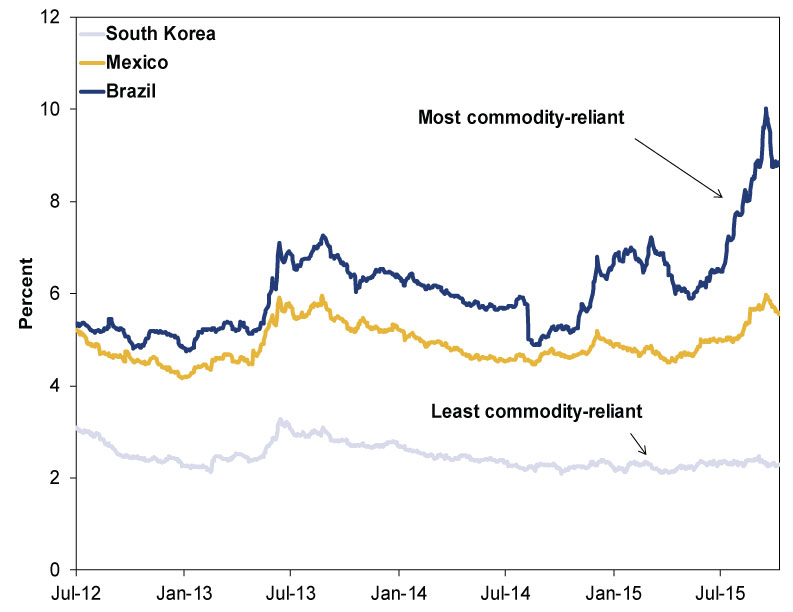

Don't just take our word for this, though. Take the market's word. EM corporate bond yields-a barometer of firms' creditworthiness-do not signal a widespread debt crisis looms. Rather, they show the more commodity-reliant countries are riskier bets.

Exhibit 2: Corporate Bond Yields for South Korea, Mexico and Brazil

Source: Factset, as of 10/22/2015. Barclays South Korea Global Corporate Index yield, Barclays Emerging Markets Mexico International Issue Index yield and , Barclays Emerging Markets Brazil International Issue Index yield, 7/13/2015 - 10/21/2015

Exhibit 3: Corporate Bond Yields for Emerging Americas and Emerging Asia

Source: Factset, as of 10/22/2015. Barclays Emerging Markets Americas International Issue Index yield, Barclays Emerging Markets Asia International Issue index yield, 7/13/2012 through 10/21/2015.

What's more, comparing yields of Mexico's domestic to external debt is worth highlighting because Mexico has a big commodity sector but isn't exclusively commodity-reliant, like Russia. Not all of its external debt is denominated in US dollars, but much of it is. Although dollar-denominated bond yields are higher than peso-denominated yields-to reflect the fact a strong dollar makes it costlier to repay-the difference is small and hasn't hugely widened since the dollar began strengthening in mid-2014. The market clearly doesn't think the strong dollar makes Mexico's external debt a crisis waiting to happen.

Look, we aren't saying all will be rosy in all Emerging Markets. But the most troubled spots are isolated, making the global fallout likely even smaller today than it was in 1997/1998. The countries in crisis in 1997 were a small part of global GDP, as are the combined GDPs of commodity-heavy EMs today. In 1997, Thailand, Indonesia, South Korea, Malaysia, and Singapore along with Brazil and Russia (drawn into the crisis later) collectively accounted for 8.2% of global GDP. Today, Russia and Brazil, the most troubled EMs today, are a combined 5.3% of global GDP. The US, UK, and eurozone on the other hand, account for 50% of global output. What's more, Brazilian and Russian issues today are mostly commodity-driven, but they are also compounded by country-specific issues, like Brazil's ongoing political scandal and Western sanctions slapped on Russia. Last we checked these are not contagious.

After dipping in 1997 when the Asian crisis broke out, the S&P 500 and MSCI World Index finished 1997 up 33.4% and 16.2%.[i] In the summer of 1998 global markets fell just over -20% when Russia defaulted, but markets quickly realized Russia's troubles-as well as the failure of massive hedge fund Long-Term Capital Management-were not the world's problems. Stocks zoomed higher in Q4, with the S&P 500 ending the year up 28.6% and the MSCI World Index up 24.8%.[ii] Meanwhile, the MSCI Emerging Markets Asia index plunged a whopping -48.2% in 1997 and another -11.0% in 1998.[iii] Weakness in one region, even extreme, doesn't necessarily spell doom for the rest of the world.

Some might say an Emerging Market debt crisis, should one occur, would have a bigger negative impact on global growth now than it did in the 1990s because the global economy is more interconnected. True enough, to an extent. But while the developed world exports a lot more stuff to Emerging Markets these days than they did in the late 1990s, the troubled, commodity-heavy economies today are actually smaller trading partners than those primarily hit back then. According to the US Census Bureau, combined US exports to Thailand, South Korea, Indonesia, Malaysia and the Philippines in 1997-the countries most affected Asia's financial crisis-accounted for just 8% of all US exports. By contrast, US exports to the most commodity-reliant Emerging Markets in 2014-Brazil, Russia, Chile, Peru, Qatar and the UAE-are just 6.6% of the total. A recession in commodity-reliant EMs would likely be less problematic for the developed world than the Emerging Asia recession was in the late 1990s.[iv]

[i] Source: Factset, as of 10/23/2015. S&P 500 total return and MSCI World Index return with net dividends, 12/31/1996 - 12/31/1997.

[ii] Ibid. 12/31/1997 - 12/31/1998.

[iii] Ibid. MSCI EM Asia Index return with gross dividends (net dividend data are unavailable), 12/31/1997 - 12/31/1998.

[iv] This last point is particularly true considering weak commodity prices are bad for commodity-heavy countries, but those same low prices benefit many other countries and companies globally.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis The New Tariffs in Town Are Still Old News2026-07-24

-

Expert Commentary This Week in Review | Market Volatility, Tariffs, SpaceX

2026-07-24

2026-07-24 -

Expert Commentary Why Ken Fisher Is Optimistic About European Stocks

2026-07-23

2026-07-23 -

Economics A Summertime Check-in on US Consumers2026-07-23

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today