Personal Wealth Management / Economics

2020’s Historic GDP Downturn—and Recovery—in Perspective

The big bounce is behind; further growth is likely, but keep expectations in check.

Many headlines noted 2020’s US economic downturn was, in some ways, the worst since WWII. GDP’s upturn since, as many also note, hasn’t fully recouped the decline. Yet it has gone a long way toward doing so, with Q3’s rebound accounting for most of the recovery thus far. Thursday’s Q4 report showed it continued but slowed, which highlights two key points: One, most of the recovery seems over. Two, a look under the hood suggests more pedestrian growth likely lies ahead.

GDP staged a big recovery in 2020’s back half, but as economic activity returns to normal, growth likely slows. After Q2’s historic GDP plunge, Q3’s 33.4% annualized rebound erased much of the lockdown-driven decline.[i] Q4 GDP followed with a 4.0% annualized gain. That slowdown was partly because of new restrictions, but also because the vast majority of the reopening rebound is behind us. With full-year numbers in, headlines focused on 2020’s -3.5% annual contraction as the deepest since 1946’s post-war demobilization. But just as noteworthy, in our view, is where Q4 finished relative to Q4 2019, GDP’s peak. It was just -2.5% below the prior high, well above the -10.1% hole at Q2’s trough. After a devastating pandemic and unprecedented economic downturn to start the year, GDP recouped a significant amount of the drop.

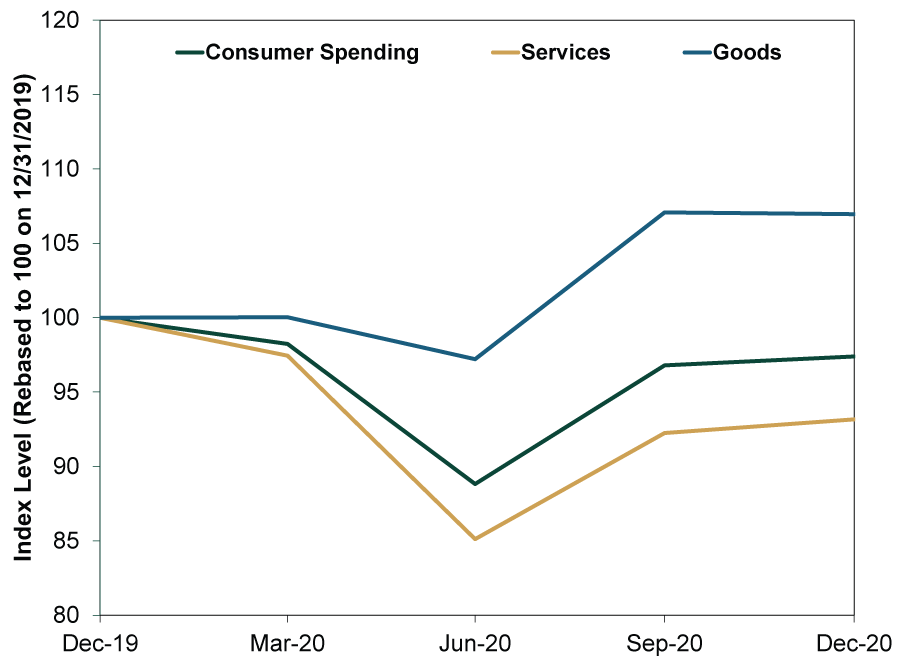

You can see this in consumer spending—or, formally, personal consumption expenditures (PCE). Exhibit 1 shows PCE (green line) and its two main components, services (yellow) and goods (blue). Overall, PCE is down just -2.6% from pre-pandemic highs.[ii] But this glosses over interesting detail. Spending on goods not only held up better in Q2 as everyone stockpiled beans and toilet paper, but it boomed in Q3 as shops reopened, passing its peak. However, goods consumption flat-lined in Q4. Households have already unleashed pent-up demand for things they could buy.

Exhibit 1: Lockdowns Still Weigh Heavily on Services Spending

Source: Federal Reserve Bank of St. Louis, as of 1/28/2021.

Services, however, seemingly have more slack remaining. Services spending—60% of PCE—is still down -6.8% from its pre-recession peak, as many major metropolitan areas closed again in Q4.[iii] It isn’t unreasonable to expect a second reopening bounce. But it probably won’t be as big as Q3’s, considering services consumption has already bounced somewhat. (In Q2, it was down -14.9% from the peak.[iv]) A bounce might also be short-lived, as goods consumption’s jump likely was. Still, it seems reasonable to expect something of a rush in services spending when the economy reopens, alleviating pain on firms that remain somewhat hamstrung by lockdowns.

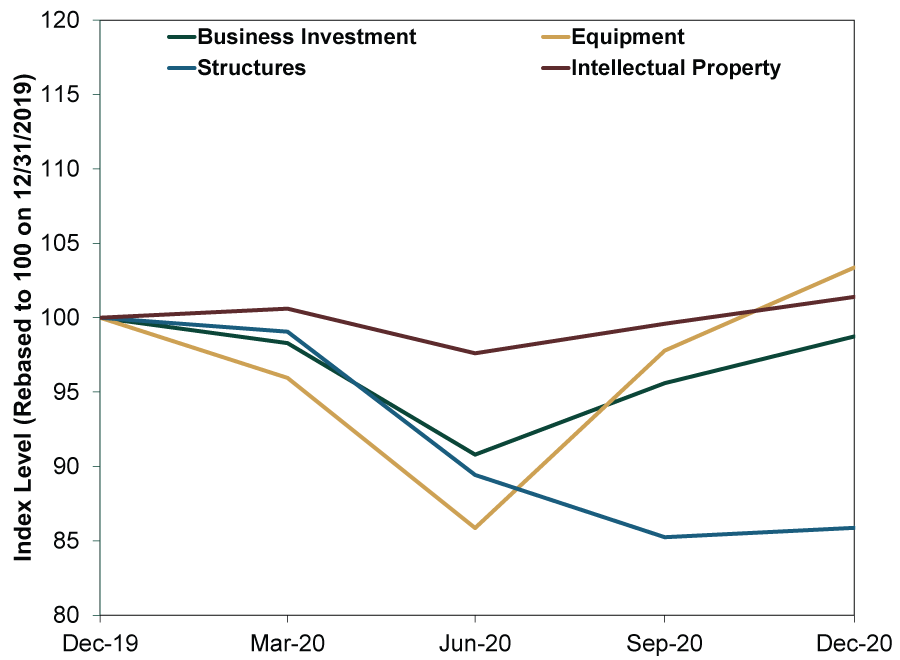

Another reason not to expect a prolonged growth surge: Businesses didn’t need to work off excesses this time around, underscoring our belief that 2020 wasn’t a traditional recession or business cycle reset. Business investment—the green line in Exhibit 2—is off just -1.3% from its high—very unusual this early in an expansion.[v] This overlooks some finer points though. While investment in equipment (yellow line) and intellectual property (maroon) are at new highs, spending on new structures (blue)—think office and commercial property development—is still hurting. Depending on how post-pandemic work and consumption patterns resume, there may be a boost here. Regardless, structures are only 15% of total business investment and likely won’t determine its overall direction.[vi] More broadly, investment’s fast recovery tells us typical late-cycle growth trends will probably resume, which generally means slower growth. But we think it also highlights the need to watch for new excesses and misallocated investment that weren’t evident in the last go ’round.

Exhibit 2: Business Investment Recovery Isn’t Uniform

Source: Federal Reserve Bank of St. Louis, as of 1/28/2021.

For stocks, slower growth is fine as long as expectations aren’t outlandish. With froth starting to flow though, keeping an eye on overall sentiment—business, consumer and market—is critical for investors. Don’t let 2020’s sharp downturn and reversal fool you into thinking we are early in the business cycle or that the bull market is young.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis The New Tariffs in Town Are Still Old News2026-07-24

-

Expert Commentary This Week in Review | Market Volatility, Tariffs, SpaceX

2026-07-24

2026-07-24 -

Economics A Summertime Check-in on US Consumers2026-07-23

-

Expert Commentary Why Ken Fisher Is Optimistic About European Stocks

2026-07-23

2026-07-23

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today