Personal Wealth Management / Economics

A Little Bit Faster Now

Fourth quarter GDP was revised higher, which is nice but presages little for the economy or markets moving forward.

Fourth quarter 2012 GDP growth was revised up from a +0.1%seasonally adjusted annual rate (SAAR)to +0.4%SAAR on Thursday. Not gangbusters, but certainly not as dour as the -0.1%first estimate released in January. In its release, the BEA noted upward adjustments to nonresidential fixed investment and exports were primarily responsible for the headline number’s increase. Personal consumption expenditures were revised down slightly, although they still contributed to growth. Government spending contracted more than expected—falling 7.0% annualized and detracting 1.4 percentage points from headline growth.

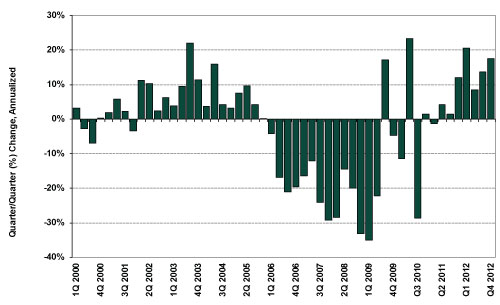

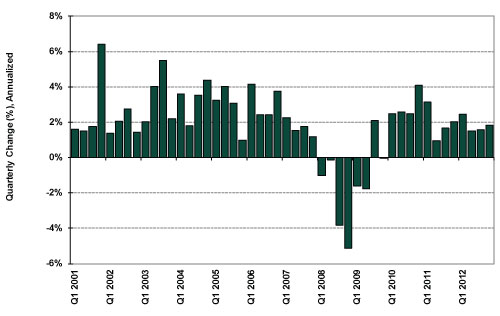

Which once again exposes the fallacies of relying on GDP as a gauge of economic health—it counts government spending positively and imports negatively, which isn’t necessarily the most accurate gauge of the real economy. As we’ve written, overall government spending has detracted from GDP for most of the current expansion, belying the strength of the private sector—the economy’s primary growth engine. Gauges of private sector activity better speak to US economic strength. For example, Thursday’s report confirmed residential investment contributed positively for the seventh consecutive quarter (adding 0.4 percentage points to headline growth) and personal consumption (adding 1.3 percentage points) contributed for the twelfth consecutive quarter, with durable consumption accounting for two-thirds of the impact. (See Exhibits 1 and 2.)

Exhibit 1: US Residential Fixed Investment

Source: BEA, Thompson Reuters.

Exhibit 2: Real US Personal Consumption Growth

Source: BEA, Thomson Reuters.

To us, the trends in these data likely presage more about economic health than the headline GDP number. Then again, while the upward revision might give some folks reason to cheer, three months after the quarter’s end, the report’s woefully backward-looking. Myriad other more recent data provide a timelier view. A high and rising LEI, strong housing reports, improvements in regional business activity, rising industrial production, growing retail sales and other gauges all suggest the economy—especially the private sector—is growing more robustly than many folks perceive.

Recent data also help shed light on one of Q4’s purported weaknesses: The fall in private inventories, which shaved 1.5 percentage point off growth. When first reported in January, many fretted businesses were slashing inventories in anticipation of lower demand ahead, signaling impending economic weakness. Well, more recent inventory data suggests those fears were unfounded. Retail inventories in January rose 1.0% from December or 5.6% from a year before, marking the largest jump since May 2011. Retail inventories (excluding autos) rose 1.3%, the largest increase since August 1995. Businesses are restocking, and sales keep rising.

Now, the directionality of inventories can be interpreted a number of different ways, but it seems likely businesses simply underestimated holiday demand in 2012, depleted inventories and are now playing catch-up. That’s a sign of economic strength, not weakness. And a much better indicator of future economic growth than last quarter’s final GDP post. (Which may still be revised again months or years from now.)

So while we can certainly cheer for a higher headline GDP number, to us, what’s more important is the ongoing fundamentals—namely, the strong private sector—that continue to underpin the US’s economic health.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Economics Quick Hit: Durably Broad-Based Growth2026-07-29

-

Market Analysis On the Chop in the Oil Market2026-07-29

-

Politics Takaichi Raises Japan’s Wall of Worry2026-07-27

-

In The News Why Kevin Warsh should think twice about hiking interest rates — even as anxiety over the Iran war grows2026-07-27

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today