Personal Wealth Management / Economics

Abenomics Part 1, Version 2.0

The Bank of Japan seems poised to move forward with long-expected monetary easing plans.

On Thursday, new Bank of Japan (BOJ) Governor Haruhiko Kuroda announced the BOJ would embark on “a new phase of monetary easing” to reach its target of 2% inflation per annum within roughly the next two years. To accomplish this mandate—set by Prime Minister Shinzo Abe—the BOJ will introduce “quantitative and qualitative monetary easing” (QQE) by doubling its monetary base, aggressively increasing long-term government bond purchases and increasing purchases of equity funds and real estate securities.

Under QQE, the monetary base will grow from about ¥138 trillion to around ¥270 trillion by the end of 2014. Monthly government bond purchases will continue at a pace of around ¥50 trillion yen but for the first time will include all maturities, including 40-year bonds. Likewise, purchases of ETFs and Japanese REITs will increase to around ¥1 trillion and ¥30 billion, respectively. It’s quite massive and a departure from Japan’s typical incrementalism.

However, don’t let the historic size of this latest iteration of quantitative easing (QE) fool you. In our view, it does little to materially move the needle in fixing Japan’s economic woes. It’s more or less a continuation of the same QE measures Japan has tried in the past to fight doggedly persistent deflation, but with little success. In that sense, the bazooka-like size of QQE may be more aimed at boosting “animal spirits” than real prices. Said different, the BOJ is attempting to push yields down across the curve to coax investors into riskier assets and (try to) modify consumption behavior in a deflationary environment.

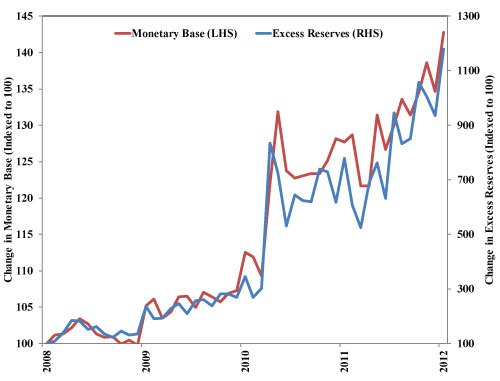

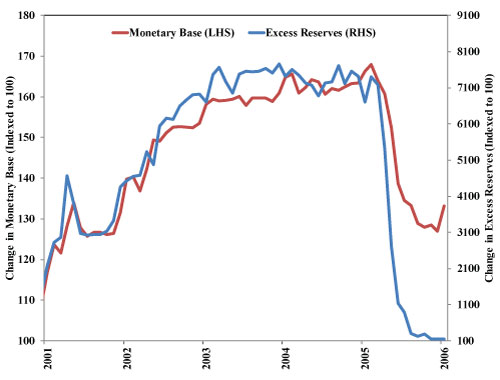

This is a movie we’ve seen before. And recently too! Just as in the US and UK, most of Japan’s QE money has ended up parked back at the BOJ as excess reserves—i.e., it isn’t materially increasing money supply in the real economy. Exhibit 1 shows that much of the QE-produced excess reserves growing in lockstep with Japan’s monetary base. And the same happened during Japan’s first QE program (2001-2006). More monetary base from here likely won’t help much—the real issue is in the velocity of money, not supply.

Exhibit 1: Japan Monetary Base vs. Banks’ Excess Reserves (2009-2012)

Source: Bank of Japan. (HT: Elisabeth Dellinger)

Exhibit 2: Japan Monetary Base vs. Banks’ Excess Reserves (2001-2006)

Source: Bank of Japan.

Kuroda is no fool—he’s likely aware of this. So perhaps putting the pedal to the QE metal is Kuroda’s way of signaling that the ball is back in Abe’s court. Recall, Abe campaigned on an economic theory focused on three primary directives: Aggressive monetary policy to boost real prices and correct (supposedly) excessive yen appreciation, fiscal policy to boost growth and structural reform to improve narrow labor markets, weak demographics, waning productivity and trade protectionism (to name a few). With Mega QE, Kuroda is making good on the monetary part—fiscal policy and structural reform is strictly in Abe’s court.

And Abe has made some progress since starting his term earlier this year—announcing measures to trim the bloated mega-conglomerates, streamline energy markets, reopen nuclear power plants and sign free trade agreements. But there’s still much more work to be done.

From here, major structural reforms to boost Japan’s economy will depend on Abe’s ability to continue influencing Parliament and, more importantly, his ability to convince the electorate painful reforms are instrumental to a brighter economic future. So far, his moves have sent his popularity skyrocketing. However, lasting economic restructuring in Japan has been challenging. We’ve seen Japan start down this road before, only to end with another prime minister on his way out (the country’s had eight prime ministers in as many years). July parliamentary elections in the Upper House will be telling. Should they go the LDP’s way, it could cement the support Abe needs to continue his progress. Stay tuned.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Business Friendly Bureaucracy or No, Britain is Growing2026-07-16

-

Economics Don’t Doubt the Old World2026-07-16

-

Market Analysis On the June Inflation Cooldown2026-07-14

-

Expert Commentary 3 Things You Need to Know This Week | US Inflation, China GDP, US Retail Sales

2026-07-13

2026-07-13

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today