Personal Wealth Management / Market Analysis

About Bitcoin and Inflation ...

Calling bitcoin an inflation hedge overlooks juuuuuuuust a few issues.

Another day, another round of inflation chatter—and, inevitably, bitcoin chatter. For there is a rumor going around that bitcoin has stolen the title of Best Inflation Hedge from gold.[i] We have seen a steady stream of articles arguing that because of its limited supply and immunity to government and central bank chicanery, bitcoin is a hard currency that will keep its value—or gain value—when inflation rears its head for real. But that logic doesn’t pass basic scrutiny, and historical data don’t exactly support it either. Now, we don’t think big inflation is imminent. However, this bogus theory seems to be worth nipping in the bud now.

For something to be a genuine inflation hedge, it should ideally have a strong positive correlation with prices—as in, when prices rise, returns increase. The faster prices rise, the faster the hedge’s price rises (and, theoretically, vice versa). That correlation should also be a long-term phenomenon that holds cycle after cycle. Bitcoin doesn’t have a long term. It is only 10 years old, and most of those 10 years were one of the longest low-inflation stretches in recent memory. During this span, bitcoin drifted sideways for years, boomed, busted, boomed again and now seems to be busting again. Notwithstanding cumulative returns, that behavior is not what one would logically expect of a hedge during a period of overall modestly increasing prices.

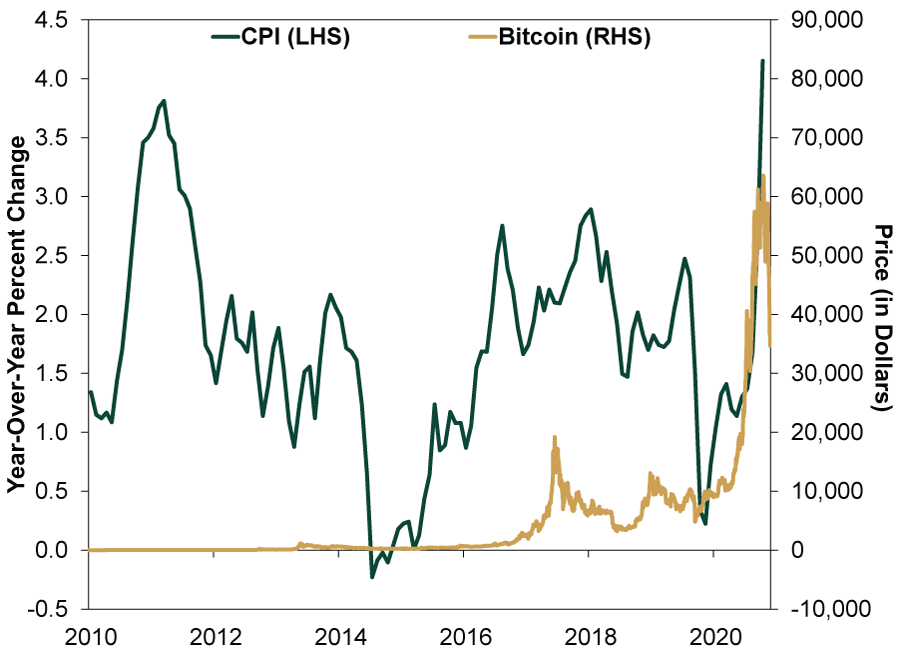

Exhibit 1: This Isn’t What Inflation Hedges Look Like

Source: Global Financial Data, Inc. and St. Louis Federal Reserve, as of 5/27/2021. Bitcoin price in USD, 7/18/2010 – 5/25/2021, and year-over-year percent change in monthly CPI, July 2010 – April 2021. Linear scale used instead of logarithmic to avoid taming bitcoin’s booms and busts.

Now, as the chart clearly indicates, moderate doesn’t mean stagnant. There were two other stretches of accelerating inflation before the present, and bitcoin delivered amazing cumulative returns during each: 2,450% from November 2010 through September 2011 and 3,438.3% from January 2015 through July 2018.[ii] But those statistics are mere trivia. The first run occurred when bitcoin was a baby and just gaining notice—people were buying for long-term speculative reasons like getting in on the next big thing at the ground floor. That isn’t a factor anymore.

The second run isn’t at all what the cumulative figure appears, because that span includes the first great bitcoin boom and bust. The peak arrived in mid-December 2017, over half a year before CPI’s inflation rate topped out at 2.9%. In those final seven months of rising inflation, bitcoin plunged -59.7%.[iii] We are going to go out on a limb and say that an actual inflation hedge would not lose -59.7% of its value while CPI inflation accelerates from 2.1% to 2.9% y/y.

Today, we seem to be living a repeat. Last year, the CPI inflation rate bottomed out in November. Since then, through yesterday’s close, bitcoin has returned 94.8%. But that overlaps an astronomical bitcoin boom and bust. CPI hit 4.2% in April (and the BLS released that report on May 12), and people now fear much worst to come. Alongside those inflation jitters, bitcoin has crashed -39.6% since April 13.[iv] Said differently, anyone who bought bitcoin as an inflation hedge over the past five weeks has probably seen their purchasing power erode much faster than the population at large. Again, not what you want if you are trying to hedge against rising prices.

The theoretical underpinning doesn’t hold up any better, in our view. The argument for bitcoin-as-inflation-hedge is that its supply has a hard limit, reinforcing scarcity and keeping it valuable as the dollar erodes. Fair enough, but while bitcoin has limited supply, the entire cryptocurrency world doesn’t. Last we googled it, bitcoin had over 10,000 cryptocompetitors, and those likely to buy bitcoin are probably the same people like to buy ethereum, litecoin, dogecoin and all the rest. The US has actually seen this movie before, sort of, during the mid-19th century, when America’s experiment with paper money involved banknotes printed by actual banks and we had no central bank. Multiple banks issued and backed many iterations of a paper dollar at once, and none of this paper ever matched the value of a gold-backed dollar, proving the simple point: Unless you have one currency, you don’t have something scarce.[v] Of course, we don’t think cryptocurrency is currency. It is, well, something else. But the idea of scarcity seems laughable when you have a theoretically limitless number of computer programmers jacking up the funny crypto supply in an unpredictable way. When Milton Friedman made that (sort-of) joke about replacing the Fed with a computer, we daresay this isn’t what he had in mind.

Again, we still think today’s inflation fears are overblown—you can see any of our recent commentaries for more on why. But we doubt inflation is dead as a phenomenon. Whenever inflation does dig its heels in for a long while, might we humbly suggest not pinning your financial well-being on a speculative bit of computer code that doesn’t really behave as it ought when inflation is on the move?

[i] Never mind that gold’s effectiveness in this regard was always more myth than reality.

[ii] Source: Global Financial Data, Inc., as of 5/27/2021. Bitcoin price change in USD, 11/30/2010 – 9/30/2011 and 1/31/2015 – 7/31/2018.

[iii] Source: Global Financial Data, Inc., as of 5/27/2021. Bitcoin price change in USD, 12/16/2017 – 7/31/2018.

[iv] Source: Global Financial Data, Inc., as of 5/27/2021. Bitcoin price change in USD, 4/13/2021 – 5/25/2021.

[v] We are deliberately omitting a few decades of fascinating economic history, including the war effort, the Panic of 1873, deep difficulties suffered by indebted farmers who didn’t want a return to the gold standard, a lot of wrangling over government intervention and the birth of the Free Silver Movement. And some other things.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis The New Tariffs in Town Are Still Old News2026-07-24

-

Expert Commentary This Week in Review | Market Volatility, Tariffs, SpaceX

2026-07-24

2026-07-24 -

Economics A Summertime Check-in on US Consumers2026-07-23

-

Expert Commentary Why Ken Fisher Is Optimistic About European Stocks

2026-07-23

2026-07-23

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today