Personal Wealth Management / Politics

All Over but the Shouting

Midterm elections brought gridlock, likely paving the way for strong stock returns.

As always, our analysis is intentionally non-partisan, focusing on political developments' likely impact on stocks. We favor neither party nor any politician and generally consider partisan bias blinding—a big risk for investors.

And with that, midterms are in the books! The polls are closed, the ballots are being tallied, and early returns show the Republicans keeping the Senate while the Democrats pick up House seats—probably enough for control. Control didn’t swing radically in either direction. While both parties will probably claim victory, for investors, the real winner should be gridlock—and stocks, as midterms’ completion ushers in the most bullish part of the presidential cycle.

Overall, the contest went largely as we expected. The president’s party lost relative power, as is typical, although it doesn’t seem like the Democrats picked up vastly more than the historical average of 30.[i] Even if Republicans end up gaining a few more Senate seats than we thought likely, it doesn’t really change the balance of power. Whether they pick up two, four or more seats, the net result is likely still a split Congress, with very little of consequence passing over the next two years. Beltway insiders might spend weeks musing about the political implications of Indiana and Missouri’s Senate seats flipping to the GOP, but that is sociology—not a stock market issue. Same goes for the madcap four-way race to fill the Mississippi seat opened by Thad Cochran’s retirement, which heads to a November 27 runoff. Ditto, also, for the issue of whether Nancy Pelosi will survive a potential House leadership contest. The nitty gritty of who won where means far, far less to stocks than the upshot of gridlock, in our view.

Most importantly, the midterm uncertainty is gone. Even with a Mississippi runoff in the cards, the Senate doesn’t hang in the balance. All the guessing is over, as is the angst over potential late-breaking surprises. To the extent midterm uncertainty contributed to stocks’ correction (sharp, sentiment-driven drop of -10% or worse) this autumn, that headwind is gone. In our view, now stocks can enjoy the tonic of falling uncertainty—and the typical bullish aftermath of midterms.

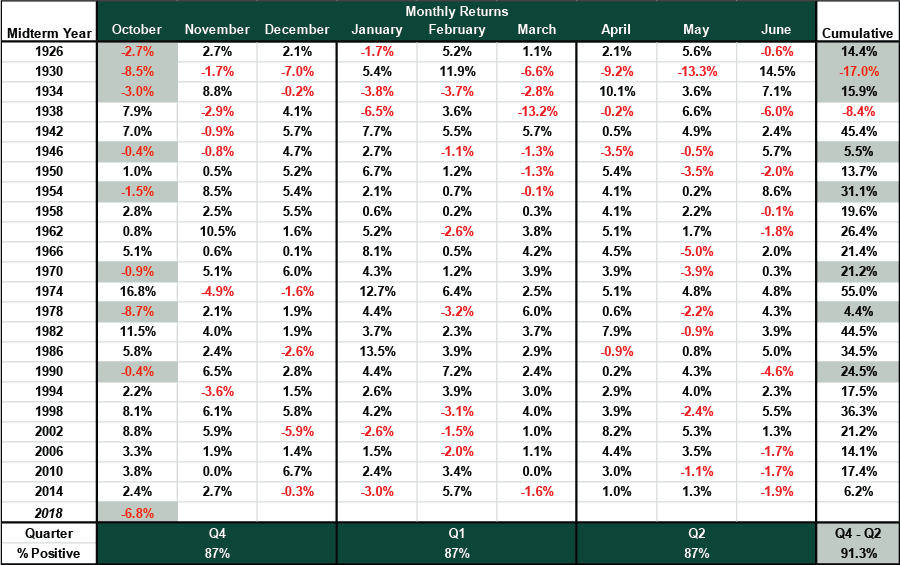

Historically, the S&P 500 has risen far more often than not in the midterm quarter and the following two quarters. In each, the frequency of positive returns is 87%—far higher than stocks’ typical 64.6% frequency of gains in non-midterm calendar quarters.[ii] That isn’t a statement about magnitude, but it does speak to stocks’ overwhelming tendency to rise as gridlock deepens after midterms. Historically, short-term volatility hasn’t derailed this positivity. In six of the eight years when at least one of these three quarters was negative, the full nine-month stretch was still positive cumulatively. Only twice were cumulative returns from September 30 of the midterm year through the following June 30 negative—1930, as the Great Depression deepened, and 1938, as World War II’s shadow descended across Europe. Overall, this nine-month stretch was positive an astounding 91.3% of the time.[iii] Better still, this overlaps with the third year of the presidential cycle—the most consistently positive, with the highest average return.

Investors might logically ask whether stocks’ lousy October makes this time different, but we doubt it. As Exhibit 1 shows, it isn’t at all unusual for stocks to have a rocky month or three during the nine-month stretch but still finish the period positive. October 1978 was even worse than October 2018—but returns from 9/30/1978 – 6/30/1979 were still positive. 1934, 1966, 1974 and 2002 also saw some painful speedbumps along the way to positive returns. While the past isn’t predictive, this history does speak to the importance of keeping a longer view, focusing on fundamentals and not getting distracted by short-term wobbles.

In short, nothing about Tuesday’s results alters our forecast. We remain bullish and expect strong returns over the foreseeable future, powered partly by gridlock and falling uncertainty. Some argue stocks will sag without a strong Congressional majority to push through more fiscal stimulus, but our forecast never depended on big action from Congress. Neither did stocks. Last year’s tax cuts were only ever ancillary to our outlook, and to say stocks need another round is to ignore the many, many other positive factors in markets’ favor. That list includes a growing global economy, nicely positive yield curves and a better-than-appreciated political landscape in Europe. Add in more opportunities for falling uncertainty as the ECB ends quantitative easing, Brexit becomes official and European Parliamentary elections come and go, and we think the future looks very bright indeed.

Exhibit 1: A Negative Month Needn’t Derail Post-Midterm Positivity

Source: Global Financial Data, Inc. and FactSet, as of 10/18/2018 and 11/6/2018. S&P 500 monthly total returns, 1926 – 2018.

[i] Source: US House of Representatives, as of 7/13/2018. https://history.house.gov/Institution/Party-Divisions/Party-Divisions

[ii] Source: Global Financial Data, as of 10/16/2018. S&P 500 total return frequency of quarterly positivity in midterm miracle and non-midterm miracle periods, Q1 1926 – Q3 2018.

[iii] Ibid. S&P 500 total return frequency of positivity in midterm miracle nine-month periods, Q1 1926 – Q3 2018.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary 3 Things You Need to Know This Week | US Inflation, UK GDP, RBA

2026-08-10

2026-08-10 -

Market Analysis Four Overlooked Costs With Dividends2026-08-10

-

Market Analysis Rechewing Fed Independence Fears2026-08-10

-

Market Analysis Quick Hit: The July Jobs Nothingburger2026-08-07

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today