Personal Wealth Management / Economics

Amid Early-Year Fed Fretting, Stay Cool

The first rate hike in a tightening cycle isn’t inherently bearish.

The new year is off to something of a rocky start, particularly for Tech stocks, with many wagging an accusatory finger at the Fed. No sooner had the world finished digesting the central bank’s plans to double the pace of “tapering” its quantitative easing (QE) asset purchases, then minutes from the December meeting suggested monetary policymakers determined the economy has largely met their self-imposed criteria for hiking rates. Moreover, they said “it may become warranted to increase the federal funds sooner or at a faster pace than participants had earlier anticipated.”[i] Now Fed watchers think the first rate hike could come in March, when QE is scheduled to end, and they are pinning the blame for the S&P 500’s -1.9% drop Wednesday on this development.[ii] Perhaps—negativity can strike for any or no reason, and Fed pronouncements always get undue attention. But don’t dwell on short-term reactions. Over more meaningful stretches, there is no evidence rate hikes automatically hurt stocks.

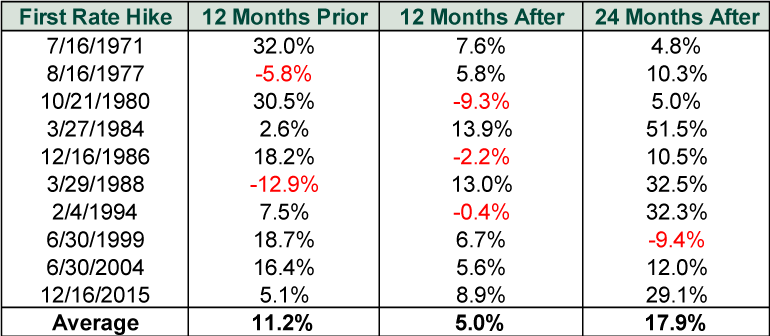

Exhibit 1 shows the history of S&P 500 returns surrounding the first rate hike in all Fed tightening cycles since 1971. As you will see, returns were positive in the first year after the rate hike 7 out of 10 times. Returns over the next two years were negative just once. Nothing here screams that rate hikes are auto-bearish.

Exhibit 1: S&P 500 Returns Surrounding Initial Rate Hikes

Source: FactSet, as of 1/5/2022. S&P 500 price returns, 7/16/1970 – 12/16/2017.

Now, the time from the first rate hike to the bull market’s eventual peak varies, ranging from a little over a month (1980) to more than six years (1994). The 1986 and 1999 hikes happened less than a year before those bull markets ended, but it was a string of counterproductive moves—not the first rate hike itself—that eventually ended the cycle. In 1987, the Fed’s much more aggressive tightening later in the year, coupled with global currency management efforts, caused a liquidity shortage that contributed to the August – December bear market, in our view. In 1999, we think the Fed’s decision to keep rates lower for longer ahead of Y2K forced them to play catch up in the New Year, leading them to invert the yield curve—which probably made the dot-com bubble crash a bit earlier than it otherwise would have, although that counterfactual is unknowable. Meanwhile, in 1980, it wasn’t just that Paul Volcker’s Fed raised rates, but that the yield curve was already inverted when they hiked aggressively to battle double-digit inflation.

That isn’t the case today. There is a healthy 1.6 percentage-point gap between 3-month and 10-year US Treasury yields.[iii] We think this is the most meaningful section of the yield curve as it best approximates banks’ business model—borrowing at short rates, lending at long rates and profiting off the spread. Even though we think long-term rates are likely to stay range-bound this year—meaning, we don’t see them rising much (if at all)—the Fed still has plenty of latitude for one or more hikes. An error is something to watch for, but acting in advance of that would be wrong, as an inverted curve alone isn’t a bull market killer. False signals abound, and inversions usually must be deep, lasting and global to truncate an economic expansion. Stocks are good at seeing through such noise.

Again, none of this precludes potential rate hikes hitting sentiment for a while. Maybe interest rate jitters spook markets into a pullback or even a correction (a sharp, sentiment-fueled drop of -10% to -20%). Or maybe they don’t—there is no way to know. Short-term swings ride on sentiment, which is inherently unpredictable. But if things look rocky for a bit, stay cool, remember that history suggests it is fine to fight the Fed, and remember false fears often look “right” for a spell when negativity strikes. But markets climb a wall of worry constructed chiefly from plausible-seeming false fears, and we suspect that will follow the current dust-up, too.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis The New Tariffs in Town Are Still Old News2026-07-24

-

Expert Commentary This Week in Review | Market Volatility, Tariffs, SpaceX

2026-07-24

2026-07-24 -

Economics A Summertime Check-in on US Consumers2026-07-23

-

Expert Commentary Why Ken Fisher Is Optimistic About European Stocks

2026-07-23

2026-07-23

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today