Personal Wealth Management /

Another Take on Yield Jitters: Dividends Versus Interest?

There isn’t much evidence yield chasers drive returns.

Interest rate jitters took on a new flavor late last week, when the 10-year US Treasury yield briefly jumped higher than the S&P 500’s dividend yield. If bonds pay more than stocks, the thinking goes, then there is no alternative goes out the window as a thesis to own stocks. People investing for income will allegedly flip from dividend-paying stocks back to bonds, removing one of this bull market’s—and the 2009 – 2020 bull market’s—supposedly key drivers. We have long seen these pure yield chasers as mostly mythical, considering people whose long-term goals and time horizon require low expected volatility probably won’t rush headlong into a more volatile asset class for its yield alone. But philosophy isn’t the only strike against that thesis. Throughout history, bond yields have topped dividend yields much, much more often than not, and we don’t see any evidence that has been bearish for stocks.

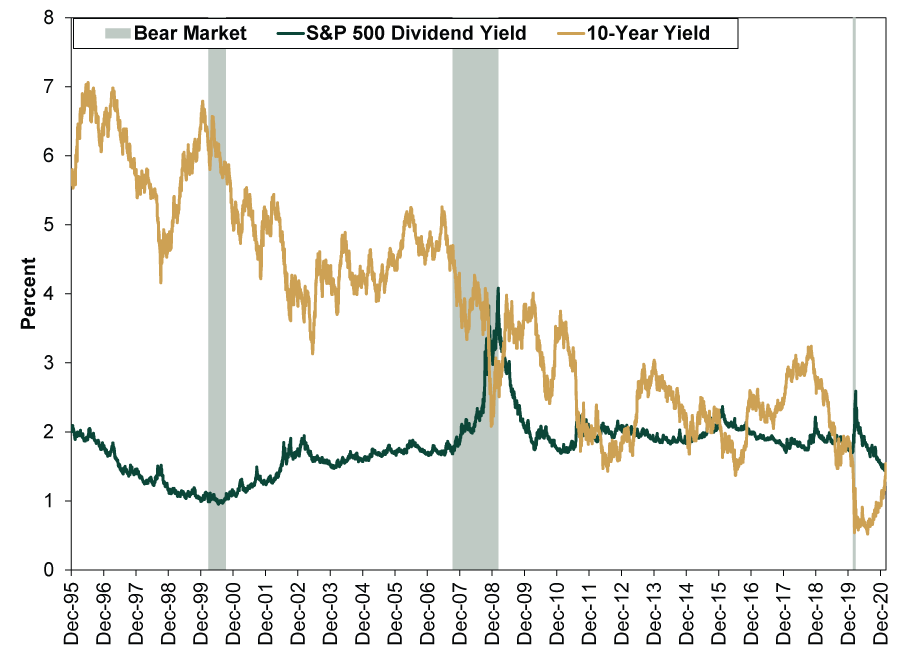

Exhibit 1 shows the S&P 500’s dividend yield and 10-year US Treasury yield since 1995, which is as far back as daily data go. As you will see, the last 11-ish months are an anomaly. Before that stretch, dividend yields topped bond yields consistently only eight times—twice during stock bear markets and six times during bull markets. That split and the overall rarity, in our view, is your first hint that this isn’t a significant market driver.

Exhibit 1: A Brief History of S&P 500 Dividend Yields and Bond Yields

Source: FactSet, as of 3/1/2021. S&P 500 dividend yield and 10-year US Treasury yield (constant maturity), 12/31/1995 – 2/28/2021.

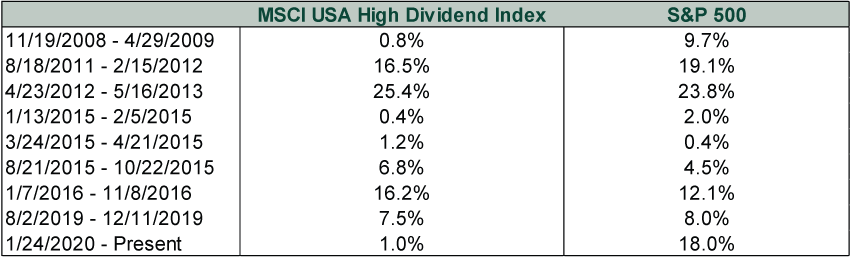

Your second clue comes from high-dividend stocks’ relative returns during these stretches. If yield chasers were a) real and b) a significant force, then you would logically expect high-dividend stocks to beat the broad markets when dividend yields exceed bond yields. As Exhibit 2 shows, however, that hasn’t been the case. We took all stretches of dividend yield leadership in the prior chart, including the present, and calculated returns for the S&P 500 and MSCI USA High-Dividend Yield Index during each period. (To avoid letting market wiggles create super-short data sets, we define a stretch as any period where interruptions to dividend yields’ leadership over bond yields lasted less than four weeks.) Here, too, there is no pattern. The S&P 500 led five times, and high dividend stocks led in four.

Exhibit 2: Yield Chasers Aren’t Driving Returns

Source: FactSet, as of 3/1/2021. MSCI USA High Dividend Index and S&P 500 total returns in the periods shown.

Perhaps most notably, high-dividend stocks’ worst underperformance happened during the current stretch—exactly when the yield chasers have allegedly been driving returns. If that were actually true, then we would expect these yield chasers to be bidding share prices much, much higher than this. Maybe not enough for the high-dividend index to actually outperform the S&P 500, which gets a boost from some high-flying Tech-like stocks that don’t pay material dividends, but it probably wouldn’t be virtually flat over the past 13 months.

Now, none of this precludes short-term volatility as these jitters persist in the next few weeks. Sometimes investors need to feel like they were “right” about an alleged negative for a bit before they get over it. But history and reason argue against a big setback for stocks just because dividend yields sink back below bond yields—in our view, it would just be a return to normal.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Why the SOX “Bear Market” Isn’t Foreboding2026-07-21

-

Politics Blunting Burnham?2026-07-21

-

Expert Commentary 3 Things You Need to Know This Week | Q2 Earnings, ECB Meeting, Trump Accounts

2026-07-20

2026-07-20 -

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—July 13 - July 172026-07-20

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today