Personal Wealth Management / Market Analysis

Brexit or No, People Are Buying UK Bonds

The record-high current account and Brexit dread were supposed to destroy demand for UK gilts. Someone forgot to tell the market.

The UK had a hugely successful 30-year bond auction this week, and ordinarily that would not be news. But people have been worried about demand for gilts, believing the high current account deficit and looming specter of "Brexit" will scare off investors and drive yields skyward, imperiling Her Majesty's finances. Compounding matters, two big European banks resigned as primary dealers in recent months, blaming regulatory barriers. After an auction for £4 billion worth of five-year gilts just barely went off on January 20, most presumed a failed sale (when the full offering isn't sold) was only a matter of time.

Since that auction, the current account deficit has risen to record highs, and Brexit fears have hit fever pitch. On January 20, Prime Minister David Cameron hadn't finished renegotiating Britain's EU membership terms with his fellow EU leaders. Since then, he has wrapped up talks and scheduled the vote (for June 23), warnings of economic doom should the UK leave have hit headlines daily, and polls have narrowed considerably. If you follow the popular narrative, this should have further eroded gilt demand.

Yet it hasn't.

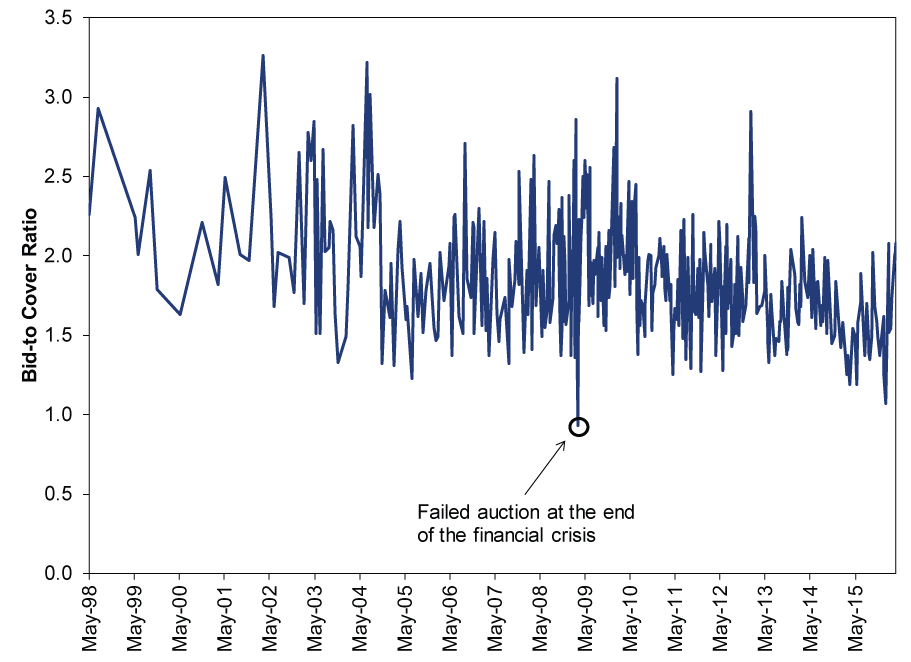

As the very messy chart in Exhibit 1 shows, demand bounced back. Bid-to-cover ratios-the amount of bids relative to the amount of bonds on offer-are back where they've been for most of this bull market. And in line with the 2002-2007 bull market. That dismal January auction looks more and more like an outlier.

Exhibit 1: A Messy Chart of UK Gilt Demand

Source: UK Debt Management Office, as of 4/14/2016. Excludes index-linked gilts.

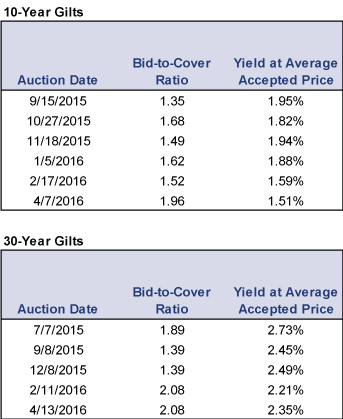

Importantly, it didn't take significantly higher yields to boost demand. Actually, yields were mostly lower at those more successful auctions. On January 20, those five-year gilts the Treasury could barely sell (the bid-to-cover ratio was just 1.07) yielded 1.1%. On March 2, a similarly sized lot of five-year gilts attracted a 1.54 bid-to-cover ratio, yet yields were lower-0.86%. April 5's five-year gilt auction saw demand of 2.01 times the amount offered, with yields even lower at 0.80%. Longer-term auctions have witnessed a similar trend, as Exhibit 2 shows. If the current account deficit and Brexit potential made UK bonds significantly riskier, Exhibit 2 would not exist.

Exhibit 2: A Less Messy Table of UK Gilt Demand

Source: UK Debt Management Office, as of 4/14/2016. Excludes index-linked gilts.

Now, some will likely argue the recent improvement stems from some changes the UK's Debt Management Office made to the auction process in an effort to boost demand, and it's a fair point-but don't overstate it. One, the changes were implemented in early April, and demand had rebounded by February. Two, the changes aren't all that significant. Banks were told to boost their minimum bids from 2% of the rolling six-month average of gilts sold at auction to 5%. But that higher bid is for pricing purposes only. They didn't have to actually raise the amount they bought. As DMO head Robert Stheeman explained: "We have introduced the expectation that banks should bid for a minimum of 5 per cent because we want them to participate more fully in the overall price formation process. But the minimum we expect them to successfully bid on is still 2 per cent. We want to see what prices they would be comfortable owning 5 per cent at." And it turns out they are comfortable owning 5% at higher prices and lower yields. Which, again, speaks volumes about how markets perceive the UK's creditworthiness.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Politics Blunting Burnham?2026-07-21

-

Market Analysis Why the SOX “Bear Market” Isn’t Foreboding2026-07-21

-

Expert Commentary 3 Things You Need to Know This Week | Q2 Earnings, ECB Meeting, Trump Accounts

2026-07-20

2026-07-20 -

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—July 13 - July 172026-07-20

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today