Personal Wealth Management / Market Analysis

Brexit Referendum Countdown Begins

The referendum is on the calendar, but Brexit talk is still mostly noise as far as markets are concerned.

Four months from now, we will know how much longer these flags will fly together. Photo by Chris Ratcliffe/Bloomberg via Getty Images.

Well, there you have it. UK Prime Minister David Cameron secured a deal to reform his country's EU membership, and voters will have their say on June 23. Get ready for four months of arguing, fear-mongering, overthinking market volatility, analysis of London Mayor (and PM hopeful) Boris Johnson's haircuts, polling, dissection of said polling and, for good measure, more arguing and fear-mongering. Or, much more simply, four months of noise. None of it will be terribly edifying for investors. It won't predict the likelihood of a vote for "Brexit" or yield actionable portfolio tactics. It will be entertaining if you're into political theater, but that's about it. If you'd rather tune out the circus, it probably won't do your investments any harm, as nothing here radically changes UK stocks' fundamental outlook.

No one can know today how the referendum will go. Polls aren't predictive. It won't be decided on campaigners' personalities. The relative merits of Cameron's deal might not even factor in much. Some voters will favor the status quo regardless, whether for fear of the unknown or a genuine belief in the EU's benefits. Others will favor leaving regardless. A large chunk of voters identifies as undecided, and no one issue will tip that entire bloc one way or the other. Nor will one single politician's influence. Different appeals and issues will resonate with different people.

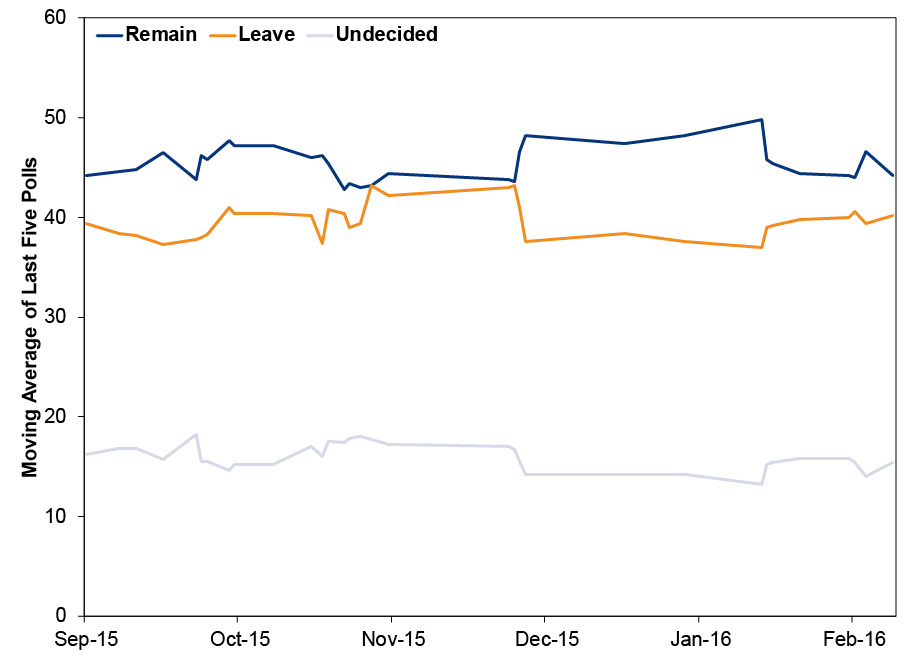

Much is being made of the latest polls, but at best, they give only the baseline for sentiment heading into the campaign. As Exhibit 1 shows, surveys give the "Remain" campaign something of an edge, but the margin of error here is fairly wide, and some polls are much closer than others. Surveys conducted online show much stronger support for "Leave" than telephone polls do, and it's anyone's guess which is more accurate. Pollsters theorize that online respondents are more politically aware (since they self-select) and therefore aren't an accurate sample. We can see the merits of that argument. Telephone surveys are more genuinely random. Then again, these are the same polling outfits that had well-documented troubles gathering a representative sample of likely voters before last year's general election, and as far as we know, none have devised and applied a solution (or at least, not one with any record of success). About the only useful thing at this point, most likely, is the demographic breakdown-and only because it shows where each campaign's hurdles are highest and how turnout among various subgroups might influence the result. Other surveys, like those purportedly showing businesses favor staying in the EU, are too narrow to reveal much-the latest surveyed all of 10 firms.

Exhibit 1: "Brexit" Referendum Polling

Source: UKPollingReport, as of 2/22/2016.

So don't read into the widely hyped poll showing only 42% of respondents would vote to stay (vs. 40% for Leave) when surveyed right after the unveiling of Cameron's deal. One survey doesn't make a trend, it's an online poll, and the polling outfit, ICM, has shown a pretty even split between Remain and Leave for months.

One key question as the campaign unfolds: Will the concessions Cameron secured from Brussels be enough to win over moderate euroskeptics? On paper, he got just about all of what he asked for. EU leaders gave the UK an explicit opt-out from further political integration, to be enshrined in the EU Treaties at a later date. Britain also gets a firm exclusion from eurozone financial regulations, the banking union and any future eurozone bailout funding. All EU countries will now have the ability to stall eurozone or banking union legislation they find onerous, provided the opposition can form a qualified majority. On the immigration front, Cameron won the right for member-states to reduce in-work benefits to EU migrants for a seven-year period[i], index exported child benefits to the economic conditions in the country where the child lives (effectively reducing welfare payments sent to Eastern Europe), and restrict migration if EU leaders agree it's necessary for economic purposes.[ii] The remainder of the agreement included some squishy pledges to reduce bureaucracy, enhance the single market and rev up free trade negotiations. The UK's opt-out from certain aspects of the EU judiciary was reaffirmed, but not strengthened.

All of this wasn't enough to satisfy one high-profile euroskeptic Conservative MP: the aforementioned Boris Johnson, who sits in Cameron's cabinet (for now) alongside his mayoral responsibilities. After spending weeks seemingly on the fence, Johnson announced his support for the Leave campaign late Sunday, and the press went nuts. Many called it a gamechanger for the Leave movement, which until now has been fractured and largely feckless, citing his fairly wide popularity among Conservative voters and a 2015 poll showing voters considered him one of the most trustworthy politicians on EU matters. Though, that same survey showed voters considered Cameron a smidge more credible, and we can't help but wonder if they'd cancel each other out. (We also reckon neither gent's opinion carries much weight with Labour supporters, who overall lean much more pro-EU.) In short, it seems quite short-sighted to read the pound's post-Boris plunge as the market saying "Game Over." Short-term volatility rarely means much. Note, also, UK stocks rose Monday.

Moreover, there isn't much evidence campaigners' names and personalities factor in all that much. Those who back certain politicians on either side of the campaign are already fairly predisposed to agree with their views on EU membership-it's part of the package-and Johnson's euroskeptic tendencies aren't exactly new news.[iii] It also remains to be seen how compelling voters will find Johnson's argument in favor of leaving. At the moment, it seems to amount to "Vote Leave so we can get an even better deal, with more guarantees of national sovereignty." We remember when Greece tried that last year. It didn't work. The UK has a vastly stronger negotiating hand than Greece did, and the economic consequences are far different, but there could be severe political consequences to interpreting a "Leave" vote as "Renegotiate." For what it's worth, Cameron said the vote is one and done, and the EU agreement clearly states it expires the instant a "Leave" vote is final.

As for what happens if voters do opt to leave the EU, the short answer is, no one knows yet. Officially, it would trigger Article 50 of the Lisbon Treaty, which opens a two-year exit negotiation.[iv] During those likely long and drawn out talks, whoever is running the UK[v] will hash out a new relationship with the EU, likely focusing on continued single market access. Parallel to that, they'll also have a chance to negotiate new bilateral trade deals, presuming membership in the European Economic Area (which would probably preserve the UK's participation in all existing EU free trade agreements) is a non-starter.[vi] For markets, this lengthy process would probably be a blessing. Regardless of whether staying or leaving would be a bigger net benefit, markets tend to dislike sudden, sweeping change. Having to discover and adapt to new rules overnight can discourage risk-taking, and markets aren't fans of the shock. A long exit process, by contrast-with negotiations playing out publicly and dissected endlessly in the media-lets markets slowly discover and price in the likely changes, negating the shock factor. The lingering uncertainty might present a headwind (similar to regulatory overhang in the wake of the financial crisis), but stocks can also do fine in that environment.

But markets will cross that bridge when and if they come to it. For now, there really isn't anything actionable for investors on the Brexit front. Making big portfolio changes based on an unpredictable referendum four months away-one whose outcome isn't inherently positive or negative for UK stocks either way-would be myopic and unwise. Volatility might linger, but the referendum's approach shouldn't be a fundamental negative for UK stocks, particularly with economic drivers fairly strong. It's one variable, but not a reason to be bearish. Ultimately, markets will wait and see, and we'd suggest investors do the same.

[ii] Here's the relevant language from the agreement: "In addition, if overriding reasons of public interest make it necessary free movement of workers may be restricted by measures proportionate to the legitimate aim pursued. Encouraging recruitment, reducing unemployment, protecting vulnerable workers and averting the risk of seriously undermining the sustainability of social security systems are reasons of public interest recognised in the jurisprudence of the Court of Justice of the European Union for this purpose, based on a case by case analysis."

[iii] There are also some domestic political considerations here-namely, Johnson's mooted desire to succeed Cameron. The press (and Cameron) speculated his announcement is an attempt to curry populist favor ahead of a potential leadership campaign, which would probably pit him against Chancellor George Osborne and Home Secretary Theresa May. For the moment, this is all just noise, probably not a swing factor for UK stocks.

[iv] There is also some chatter about Scotland, which is overall more pro-EU than England, and the possibility for a second independence referendum if Leave wins. But that's all speculation at this point and impossible to handicap.

[v] Most believe Cameron will step down if Leave wins.

[vi] You'd think it would be, as EEA participation would subject the UK to all EU regulations and require contributions to the budget, without any parliamentary representation or other policy say-so. But, stranger things...

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary This Week in Review | Global PMIs, SpaceX, RMD Planning

2026-07-10

2026-07-10 -

Market Analysis Trim Your Angst on Economic Measurement Tweaks2026-07-09

-

Politics Long-Term Forecasts and Court Verdicts: The Latest in British and French Politics2026-07-09

-

Corporate Information How You Benefit from Fisher Investments' Transparent Fee Structure

2026-07-08

2026-07-08

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today