Personal Wealth Management / Market Analysis

Bully for Bullion?

Investors seem too hot to trot for gold.

These are shiny, but not a wise long-term investment. Photo by Dario Pignatelli/Bloomberg via Getty Images.

What's shiny, yellow and up nearly 17% this year? Gold! And boy, have people noticed. The two biggest gold ETFs have attracted huge inflows this year, and those inflows gained steam as gold's rise stole more headlines. Those headlines hyped gold's supposed ability to hedge against stock market volatility and a Fed that keeps rates lower for longer as other central banks cut further below zero. Investors aren't just gobbling up gold itself-trading volumes in call options are spiking. Yet underneath it all, gold's supply and demand fundamentals haven't radically shifted. Global production hit another new high last year, even as prices plumbed a new low, suggesting the industry still hasn't responded to price signals. That means anyone going hog wild for gold now is likely making a purely sentiment-based play-a risky move that probably doesn't jibe with most long-term investors' goals.

Gold isn't special. Or, at least not as an investment. Its elemental properties are one of a kind, but that's about where its specialness ends. Yes, it's shiny. Yes, it used to back money. But it isn't a financial safety blanket-it has fallen during plenty of bear markets and geopolitically troubled times. It isn't an inflation hedge-it fell for most of 1980 and 1981, when US inflation hit double digits, and slid for most of the 1990s, when inflation routinely topped 2%. And it isn't a stable store of value-it has fallen, a lot, over time. It is just a commodity, and one with few industrial uses. Outside jewelry, there is little physical demand. Hence sentiment tends to be the swing factor, triggering huge swings in either direction.

On the supply side, gold fundamentals don't look terribly favorable. Commodity cycles are typically long, as production requires long lead times and high up-front investment. New mines can take years to get off the ground[i]. As a result, producers aren't very nimble. They can't respond to price signals swiftly. Like oil producers, they often keep production going after prices turn, so they can recoup at least some of that up-front cost. Investment in new mines might fall, but it takes years for this to flow through to production totals. Eventually it does, and prices turn-and keep rising as producers are slow to ramp investment back up, beginning the cycle anew.

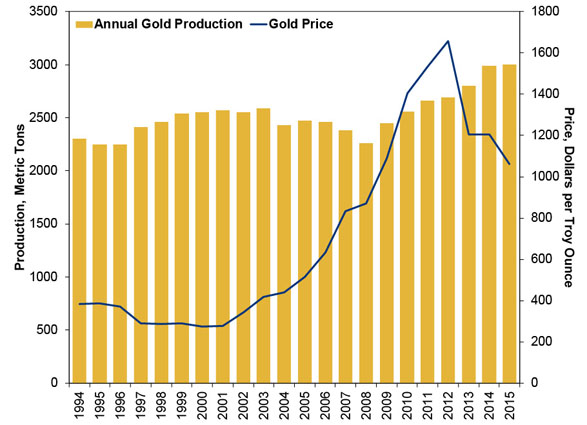

As Exhibit 1 shows, producers haven't really cut back yet. Even as gold hit a five-year low late last year, production hit a new all-time high. That's a strong indication sentiment bears most of the responsibility for gold's recent run.

Exhibit 1: Gold Production and Prices

Source: FactSet, as of 2/29/2016. Annual world gold production and year-end price, 1994 - 2015.

Sentiment is running extremely hot right now, if all that options trading is any indication. Investors are rushing to make a leveraged bet on a commodity that's still mired in a supply glut. That isn't normal, rational, clear-thinking behavior. It looks an awful lot like excessive optimism, a scenario where folks should always tread extremely lightly or not at all.

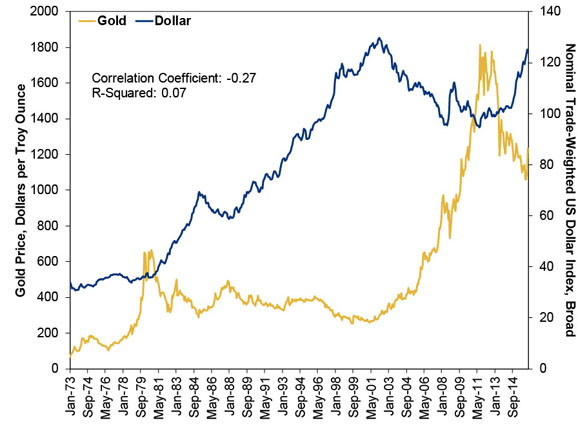

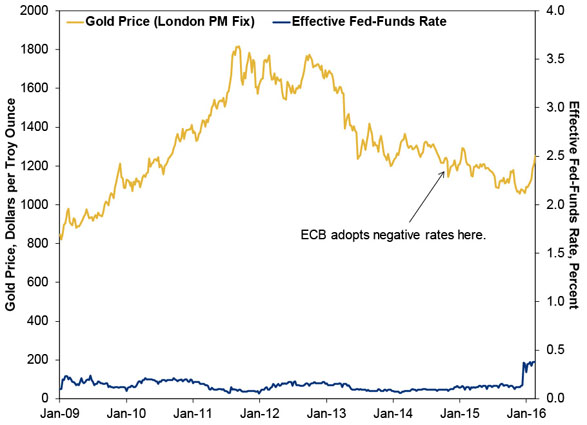

Nothing about today's financial landscape makes gold a fundamentally attractive buy now, as far as we're concerned. The dollar has weakened, yes, but gold and the dollar have no set relationship, with statistically meaningless correlation stats (Exhibit 2). And Exhibit 3 should completely gut the myth that gold has anything to do with where the Fed sets short-term rates or how negative rates go in Europe.

Exhibit 2: Don't Holler About Gold and the Dollar

Source: Source: St. Louis Federal Reserve, as of 2/29/2016. London PM Gold Fix and Nominal Trade-Weighted US Dollar Index (Broad), 1/1/1973 - 2/29/2016.

Exhibit 3: Ben Bernanke and Janet Yellen Walk Into a Bar ... of Gold

Source: St. Louis Federal Reserve, as of 2/29/2016. London PM Gold Fix and Effective Fed-Funds Rate, weekly (ending Wednesdays), 1/1/2009 - 2/24/2016.

Because gold is so volatile, with sentiment swings a key factor, successfully investing in it requires extraordinary short-term timing. We aren't aware of anyone with a demonstrated history of repeatedly nailing gold peaks and troughs. Markets are impossible to predict and time with precision over short periods, whether commodity, stock, bond, currency or some other similarly liquid market. Sentiment turns on a dime and frequently detaches from reality, as gold has proven these last few weeks. Maybe it's just us, but staking your financial future on something so squishy seems foolhardy indeed.

[i] This is a figure of speech, because obviously there is a lot of digging in this process. Though we guess it is sort of literal, too, as gold mines do have physical structures above-ground. We'll let you choose your own figure of speech and suggest "into the ground" as an awkward, yet semi-viable alternative.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis The New Tariffs in Town Are Still Old News2026-07-24

-

Expert Commentary This Week in Review | Market Volatility, Tariffs, SpaceX

2026-07-24

2026-07-24 -

Expert Commentary Why Ken Fisher Is Optimistic About European Stocks

2026-07-23

2026-07-23 -

Economics A Summertime Check-in on US Consumers2026-07-23

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today