Personal Wealth Management / Market Analysis

Chart of the Day: Growth and Value Trends Are Global

US and European value stocks have more in common than you might think.

Friday morning, a widely syndicated Bloomberg article caught our eye. As we summarized in our coverage in MarketMinder’s “What We’re Reading” section, it theorized that since European value stocks have lagged US value stocks this year—while US value stocks have beaten their growth counterparts—European value must be due for some catch-up and major outperformance. As qualitative evidence, it offered Europe’s relatively delayed COVID vaccine rollout and reopening, presuming those factors are value stock fairy dust. We see a few glaring problems with this thesis, and they are worth spending a bit of extra time on, lest our readers be fooled into basing hasty portfolio decisions on flawed logic.

For one, markets deal efficiently with widely known information. It has been readily apparent for months that European trends, overall and average, would probably trail the US by a couple of months. When events are that widely anticipated, stocks don’t just sit around and wait for them to happen—they reflect them well in advance. So, in our view, to say European value stocks don’t yet reflect vaccines and reopening there is to say markets aren’t efficient, which we think is dangerous territory to base any theory on.

Beyond that, the European value catch-up thesis misses a key point about growth and value leadership trends: They are global. If value isn’t leading in the US, it probably won’t lead in Europe. In our view, the reasons for this are twofold. One, market cycles are generally global, not local, and growth/value leadership ties into the broader bull/bear cycle. (See this for more.) Two, growth/value trends also stem from global economic trends, and you rarely get wide divergence among developed-world countries on that front. We are slowly moving out of the reopening mini-boom and into what looks likely a post-pandemic trend of slower growth. Yes, even in Europe, considering GDP there is quite close to its pre-pandemic peak. In slower-growth environments, investors usually flock to big companies with recognizable brand names and a proven ability to crank out earnings through thick and thin. In other words, growth stocks.

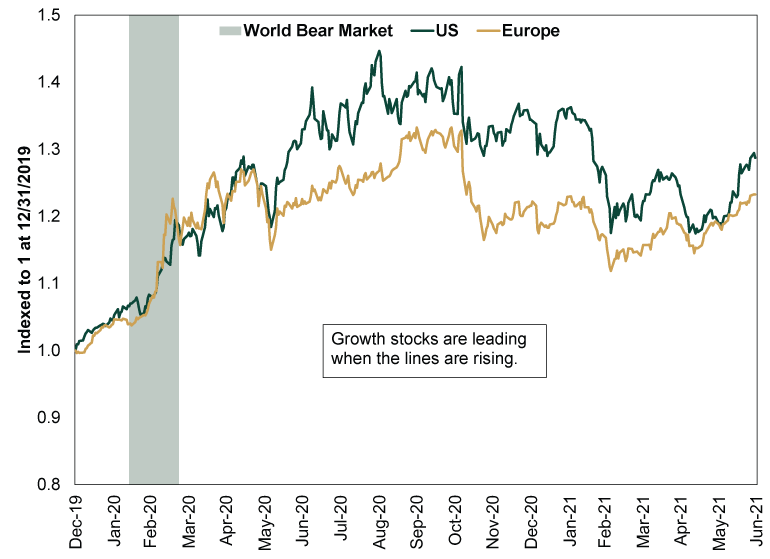

But don’t just take our word for all of this. Consider our chart, which shows growth’s returns relative to value in the US and Europe since the beginning of last year. The US line divides the Russell 3000 Growth Index by the Russell 3000 Value Index. The European line divides the MSCI Europe Growth Index by the MSCI Europe Value Index. When the lines are rising, it means growth is beating value. Note how they move in near-lockstep directionally. The magnitudes differ, but the directional wiggles are near-identical.

Exhibit 1: Growth Vs. Value, Transatlantic Edition

Source: FactSet, as of 7/9/2021. Russell 3000 Growth and Russell 3000 Value total returns and MSCI Europe Growth and MSCI Europe Value returns with net dividends, 12/31/2019 – 6/30/2021. Indexed to 1 at 12/31/2019.

So rather than chase European value on the thesis that laws of physics require it to rise up to meet US value, we suggest thinking bigger picture: Value-heavy categories, regardless of geography, look unlikely to lead over a material length of time for the foreseeable future.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis The New Tariffs in Town Are Still Old News2026-07-24

-

Expert Commentary This Week in Review | Market Volatility, Tariffs, SpaceX

2026-07-24

2026-07-24 -

Economics A Summertime Check-in on US Consumers2026-07-23

-

Expert Commentary Why Ken Fisher Is Optimistic About European Stocks

2026-07-23

2026-07-23

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today