Personal Wealth Management / Economics

China’s Gangbusters Loan Growth

China likes doing things on a grand scale; its recent stimulus is no exception.

China is slowing! We know, we know, that isn’t exactly breaking news. For much of the last year, data showing downticks in the Middle Kingdom’s economic growth rate have resurrected (again) Chinese hard landing fears, with many fretting global fallout. Now, growth is slower, and we think weakening private sector demand from China weighed on developed world export growth in late 2018. But it seems like a mistake to us to extrapolate this forward. Chinese authorities have many ways they can boost growth—and they have enacted some. Yet many seem skeptical China’s moves will do much. However, loan growth’s January surge hints at the impact coming soon.

Although many believe the trade dispute between the US and China is driving China’s slowdown, we think it stems mostly from Chinese policymakers’ crackdown on China’s “shadow banks” last year. These non-traditional private lenders predominantly financed small and midsize firms, which make up most of China’s private sector and drive economic growth. When private sector funding dried up, the economy slowed more sharply than many expected, goading action from China’s leaders. That action entailed a slew of measures, including roughly $200 billion worth of fiscal stimulus, another $125 billion earmarked for urban rail projects, $200 billion in local government bonds funding infrastructure—allowing municipalities to issue them ahead of schedule—and a variety of tax breaks worth approximately $300 billion.

China is also employing monetary stimulus. China’s central bank—the People’s Bank of China (PBoC)—cut the reserve requirement ratio (RRR) for large banks from 17% last year to 13.5%. Small banks’ RRR is down from 13.5% last year to 11.5%. This means China’s banks have more capacity to lend. But that doesn’t automatically direct funding where it is most needed, as banks tend to prefer lending to large state-owned enterprises, which have an implicit government guarantee. So the PBoC set up a lending facility effectively subsidizing credit to private small and medium-sized businesses. Skeptics wonder why data largely don’t show an effect, perhaps seeing it as a sign the measures are feckless. But this was never going to hit the economy right away. Monetary policy typically hits at a lag. However, January lending data suggest it is starting to fertilize some green shoots.

China Goes Big

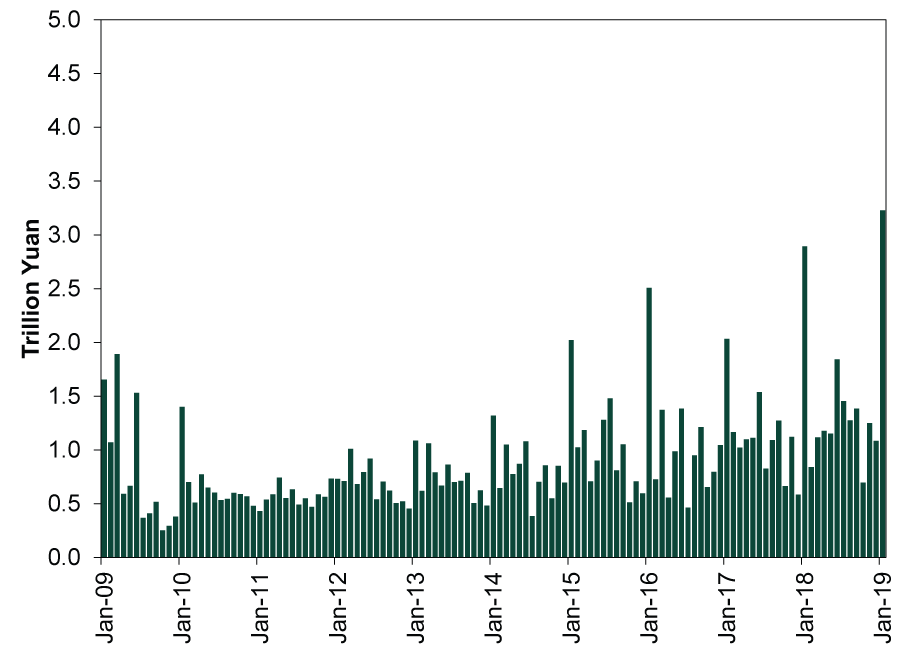

New loans denominated in yuan (aka renminbi, RMB) hit 3.23 trillion—with a T—in January. That is almost half a trillion US dollars of new lending in one month. This triples December’s figure and doubles January 2009, when Beijing sought to cushion China from the global financial crisis—and succeeded. Now, as Exhibit 1 shows, January’s lending surge is typically seasonal—as banks try to hit lending quotas before the Lunar New Year—but even compared to recent years’ average of ¥2.36 trillion in new January loans, this year’s is 37% bigger.[i]

Exhibit 1: New Yuan-Denominated Bank Loans

Source: FactSet, as of 2/28/2019. RMB loans, monthly change, January 2009 – January 2019.

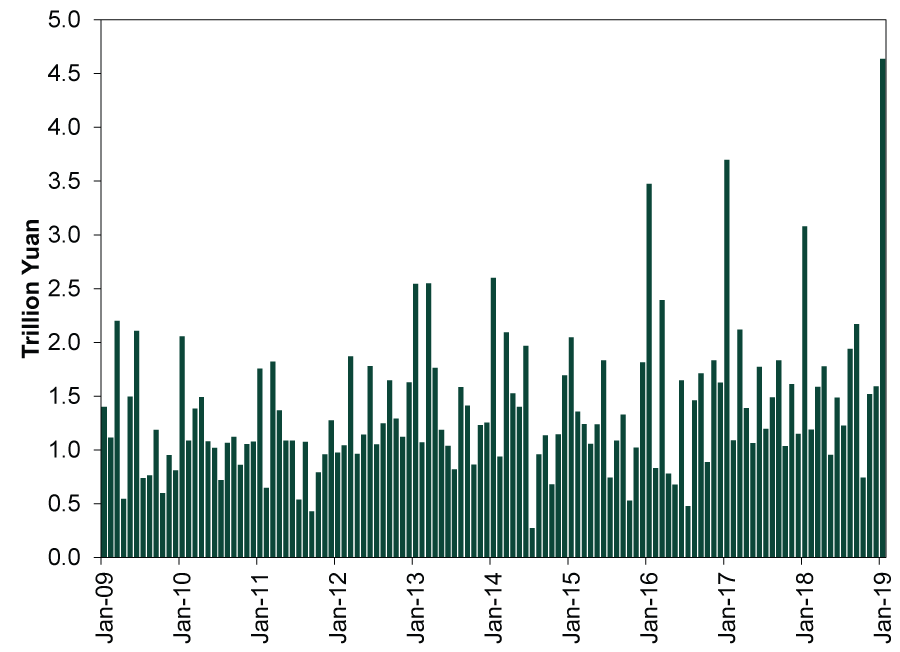

Besides bank loans, there is a boom in corporate bond issuance, although it does seem private firms are still having trouble there. Last December, the National Development and Reform Commission—China’s economic planner—eased restrictions on companies with solid balance sheets (a debt ratio less than 85%) and credit histories (no default in the last 3 years). The official stamp of approval helped net financing of corporate bonds hit half a trillion yuan in January, a three-year high. All this has driven new total social financing—all loans, including shadow banks’, bonds and other funding China’s financial system provides to its private sector—up to a record high ¥4.64 trillion in January. (Exhibit 2) That said, bond funding is going mostly to local government backed state-owned enterprises. Of the 657 firms issuing bonds so far this year, only 78 are private, as small businesses still face significantly higher rates than state-backed ones.[ii] This is something officials are trying to tackle though, and what matters for near-term growth is the improved flow of credit overall. Directing it to the private sector was always going to be a trial-and-error process.

Exhibit 2: Total Social Financing Jumps in January

Source: FactSet, as of 2/26/2019. Social Aggregate Financing to the Real Economy, Flows, January 2009 – January 2019.

But Monetary Stimulus Works With a Lag

While the scale of new loans and debt issuance is impressive, it doesn’t immediately translate into economic activity. It is possibly behind February’s improvement in the private-sector centric Caixin Purchasing Managers’ Index new orders subcomponent, which flipped into expansionary territory.[iii] But that is just one isolated read—it might be a few months more before a Chinese recovery becomes apparent in output-related data. Once a company has secured funding, it has cleared only the first hurdle. Although ¥4.64 trillion ($687.88 billion) in new financing burning a hole in your pocket might be a nice problem to have, unless it is put to work, it won’t add to GDP or other output measures. Once it is spent and invested—and re-spent and reinvested—it should circulate through the economy and boost growth eventually. But it takes time and won’t hit all at once.

Complicating matters, Chinese New Year, which fell on February 5 this year, also distorts and delays monthly economic data releases. Because lunar calendars deviate from the Gregorian calendar (the one we use), seasonal distortions often make it hard to compare economic data year-over-year. The Lunar New Year wanders between January and February, but with festivities lasting a couple weeks, it can also skew data as late as March, as most firms plan around the celebrations. December data can even be inflated, as firms race to lock in orders before shutting for weeks. Reliable reads on the economy—at least from official sources—on how lending is impacting growth, may not be available until the second quarter.

Yet stocks don’t wait for confirmation of economic trends. A nascent economic pickup is perhaps behind the MSCI China Index’s 16.2% year-to-date jump (in yuan terms to remove currency effects).[iv] As we wrote recently, stocks usually move before economic data can confirm a turn. Now, Chinese stocks have historically been a less-reliable economic indicator, considering the gauge has cycled through several bear markets over the past 10 years even as Chinese GDP has grown nicely. But the bounce, coupled with other forward-looking measures like loan growth and purchasing managers’ index new orders, seems to suggest stimulus starting to hit. Hence, a hard landing zapping global stocks still looks unlikely.

[i] Source: FactSet, as of 2/28/2019. RMB loans, monthly change, average of January 2015, January 2016, January 2017 and January 2018.

[ii] “China Starts the Year With a Corporate Bond Boom,” Shen Hong, The Wall Street Journal, 2/20/2019.

[iii] “China’s Manufacturing Activity Shrinks Again in February but at Slower Pace,” Yawen Chen and Ryan Woo, Reuters, 2/28/2019.

[iv] Source: FactSet, as of 3/4/2019. MSCI China Index returns with net dividends in yuan, 12/31/2018 – 3/1/2019. In US dollars, it returned 16.0%.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis The New Tariffs in Town Are Still Old News2026-07-24

-

Expert Commentary This Week in Review | Market Volatility, Tariffs, SpaceX

2026-07-24

2026-07-24 -

Economics A Summertime Check-in on US Consumers2026-07-23

-

Expert Commentary Why Ken Fisher Is Optimistic About European Stocks

2026-07-23

2026-07-23

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today