Personal Wealth Management / Market Analysis

China’s PMI Dip: Another Brick in the Wall of Worry

Manufacturing PMI contractions aren’t unusual in China.

Thursday brought the first look at how China’s electricity shortage is affecting the economy, and the results weren’t exactly pretty: The government’s official manufacturing purchasing managers’ index (PMI) sank to 49.6 in September, implying contraction. Caixin’s PMI, which includes a host of smaller private firms, technically broke even at 50.0, but its production subcomponent remained in contractionary territory, according to the press release from Caixin and IHS Markit. These survey results were all pundits needed to conclude that China’s energy crisis is adding to economic pressures, jeopardizing the global recovery from lockdowns. In our view, that is just a tad hasty, and the likelihood that global markets will have to reckon with a hard landing in the world’s second-biggest economy remains low.

Interpreting PMIs correctly requires a clear understanding of both their quirks and their history. They do not measure—or even attempt to measure—how much activity increases from month to month. That responsibility lies with output measures like industrial production. PMIs, by contrast, are surveys. Businesses report on whether output, new orders, employment, supplier delivery times and sentiment rose or fell versus the prior month. Then the agency producing the PMI compiles all the results and computes them into an index. The index’s reading, roughly, is the percentage of businesses reporting increased economic activity overall. If it exceeds 50, a majority of firms reported expansion, which implies the sector grew. If it is below 50, it implies contraction. So September’s 49.6 manufacturing PMI means a slight minority of firms reported expansion.

But because the PMI doesn’t measure how much businesses grew, the relationship between PMIs and output is fuzzy at best. If only 49.6% of businesses reported growth, but they grew by more than the others contracted, then output can still rise in a given month. So while we think PMIs are handy, as they are generally the first economic indicator released for a given month, we think it is best to take them with a grain of salt. Don’t get too excited by incremental moves down or up, especially when they are very close to 50, like China’s latest figures.

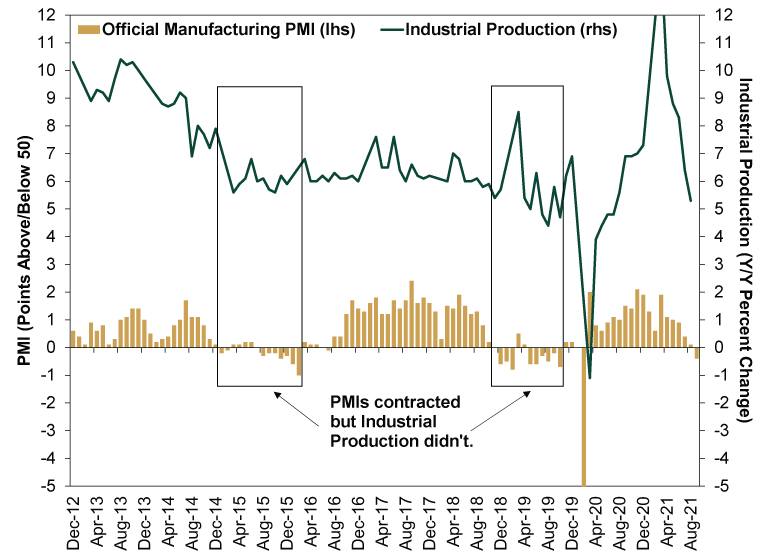

China’s own history vets this out. The official manufacturing PMI has had two lengthy contractionary spells in recent history—one in 2014 – 2015 and one in 2019. As Exhibit 1 shows, industrial production continued growing both times. It slowed somewhat at points, but the growth rates remained healthy overall, and China continued contributing mightily to global GDP growth. The only time a contracting PMI signaled an actual economic contraction was in February 2020, when China’s COVID lockdowns were at their strictest.

Exhibit 1: Chinese Manufacturing PMI and Industrial Production

Source: FactSet and National Bureau of Statistics, as of 9/30/2021.

Granted, China wasn’t dealing with rolling blackouts during either of those spells, but it wasn’t without headwinds. In 2014 and 2015, manufacturing globally hit the skids, but China got an extra thumping from the government’s efforts to curb supply excesses in steel and other industries. In 2019, it was a continued crackdown on the shadow banking realm and local government debt issuance, which triggered a broad economic slowdown.

In our view, the electricity shortages are just the latest in a long line of external headwinds Chinese businesses have had to deal with—and they have become very good at doing so over time. Necessity is the mother of invention, and factory owners don’t want to close shop just because their power supplier has gone dark. Plus, China has a long history of intermittent power outages due to the retail price limits imposed on suppliers—this bout is just getting more international attention than usual. Many businesses keep generators on hand to compensate, and a Wall Street Journal piece this week reported the loud hum of generators echoing across entire cities. That isn’t a great solution, but it likely cushions output a lot more than today’s PMI coverage might lead you to believe.

The great global power freakout has all the hallmarks of a classic ghost story for stocks—the sort of tale that often accompanies volatility and corrections (sharp, sentiment-driven drops of -10% to -20%). The S&P 500, which fell -1.2% today, isn’t yet in correction territory, but it could get there.[i] It is pretty easy to see how China’s power woes could collide with Britain’s gas lines and Europe’s natural gas shortage to continue spooking people globally for a while longer. The issue is one society hasn’t had to deal with for a while, and it raises everyone’s favorite bogeyman: comparisons with the 1970s. But the great thing about when ghost stories and volatility collide is that, whether or not said ghost story actually caused said volatility, people naturally conflate correlation and causation. They see the thing they fear having the effect they feared, and they think, I was right. Then, when stocks recover, human nature dictates they will think the problem has run its logical course and isn’t a threat anymore. That knocks one item off their worry list, lifting sentiment a bit. That gradual warming is what bull markets are made of—a textbook case of stocks climbing the wall of worry.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis On the June Inflation Cooldown2026-07-14

-

Expert Commentary 3 Things You Need to Know This Week | US Inflation, China GDP, US Retail Sales

2026-07-13

2026-07-13 -

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—July 6 - July 102026-07-13

-

Expert Commentary This Week in Review | Global PMIs, SpaceX, RMD Planning

2026-07-10

2026-07-10

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today