Personal Wealth Management / Market Analysis

China’s Wild and Crazy Week

Volatility in China is rekindling hard landing fears, but we'd suggest too much is being made of the swings.

Global markets tumbled Thursday, deepening 2016's early decline as turmoil on Chinese markets once again spooked investors worldwide. For the second time this week, Chinese domestic markets closed early after a -7% intraday drop triggered new circuit breakers. Thursday's slide happened after the central bank surprised investors by devaluing the yuan by -0.5%. Together, these developments sparked fears of a Chinese government struggling to bolster its weakening economy, perhaps signaling the long-dreaded hard landing has finally arrived. But this interpretation seems premature and overstated. China's markets are no stranger to big volatility or head-scratching intervention, and nothing that has happened this week is out of the ordinary-or out of step with China's long-running, gradual, intentional slowdown. China can roil sentiment, as it has this week, but there should be minimal lasting global impact. We don't believe anything that happened this week has the power to cause a bear market.

Wild Swings and Faulty Circuit Breakers

For the second time this week, steep declines in Chinese stocks triggered a new mechanism that stopped trading altogether. The mechanism-commonly called "circuit breakers"-suspends trading for 15 minutes when the market falls -5% intraday. If the decline deepens to -7% after the market re-opens, it closes for the day. Chinese regulators cooked up this system after last summer's wild swings on local exchanges, and it went live Monday. Most agree it was an abject failure, creating a self-fulfilling prophecy of heightened volatility. Circuit breakers' purpose is ostensibly to allow panicked traders to take a deep breath, calm down and get over the urge to sell immediately. But the circuit breakers seemed to have the opposite effect. On Monday, the second circuit breaker kicked in seven minutes after the pause ended. Thursday, it took just one minute. Turns out investors used the pause to flood the system with sell orders, worried they'd be stuck if they couldn't trade at all. Instead of preventing a sell-surge, the mechanism ostensibly caused it. Officials seemed to agree, as they killed the circuit breaker later Thursday.

Now, what causes volatility on any given day is always a big question mark, and it's probably unfair to pin it on market structure alone. But the big global fear, that China's plunging market implies its economy is weakening more than many previously thought, is probably overstated. Unlike most developed markets, whose stock markets are fairly good leading indicators of economic activity, China's stock market is largely divorced from its economy. Local markets are wild and crazy, driven mostly by retail investors, many of whom trade on margin and view stocks more as a speculative bet than a long-term investment. Heavy restrictions on corporate insider and institutional trading further muddy the market, as does chronic intervention (like the ongoing ban on large shareholders' selling). All reduce liquidity and diminish price discovery. Recent history illustrates this nicely. China's market has suffered three -20% or worse drops since 2009, yet China's economy grew all the while.

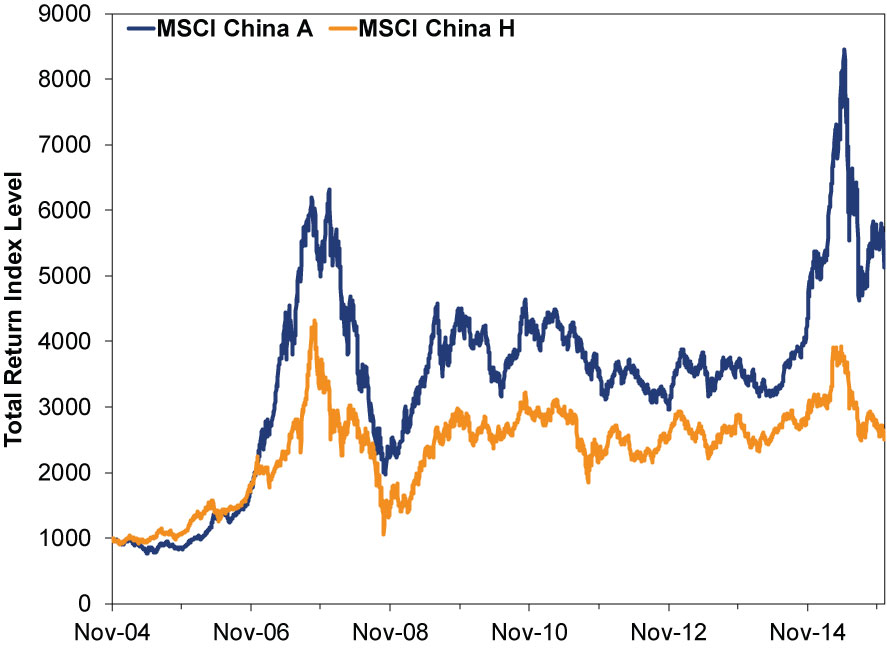

You can also see this in the disconnect between China's A-shares-local firms traded on local exchanges-and H-shares, which are local firms traded on the Hong Kong exchanges. A-share markets are largely off-limits to foreigners. Most foreigners trade H-shares, making them a more efficient gauge. H-shares also don't have oddly constructed circuit breakers. This week, they had far less volatility. On Monday, when A-shares fell -7.4%, H-shares fell only -3.6%. That's a sizable drop, but less than half the mainland's magnitude.[i]

While sentiment surrounding mainland volatility can hit global markets temporarily-as we saw last August as well as this week-China's firewalls largely prevent lasting spillover. Mainland markets are mostly walled off to foreign investors, save for a small pilot program allowing very limited participation. Capital controls greatly limit the amount of money flowing in and out of the country. There is just no real transmission mechanism for equity weakness there to go global. As Exhibit 1 shows, the divergence between A-shares and H-shares stretches back over a decade. If even China's twin markets aren't so connected, then mainland markets have very little to do with markets abroad.

Exhibit 1: A-Shares Vs. H-Shares

Source: FactSet, as of 1/7/2016. MSCI China A and MSCI China H returns with net dividends, 11/30/2004 - 1/6/2016.

An Overstated Yuan Devaluation

Last August 11, the central bank caused a stir when they set the yuan's reference rate (the midpoint for that day's trading) -2% below the prior day's close and changed how the yuan would trade moving forward. Instead of setting the reference rate directly, officials said it would be based on the previous day's closing price and market makers' quotes. The daily trading band would remain at +/- 2%, though aside from that limit, the change nominally injected more market forces into the currency. Since then, they have allowed the yuan to depreciate gradually, while reportedly intervening to strengthen it at times. But this week, they surprised markets by setting the reference rate lower on Wednesday and Thursday.

Many misinterpreted this as a desperate move to stoke exports or other parts of the economy, believing this is a sign the long-dreaded hard landing has arrived. But this seems like a stretch. The latest intervention amounted to setting the reference rate -0.5% lower on Thursday (following a -0.2% reset on Wednesday), which is puny and very unlikely to materially impact export growth. Devaluations aimed at boosting exports are usually orders of magnitude larger. (Not that they're a panacea-an article for another day.)

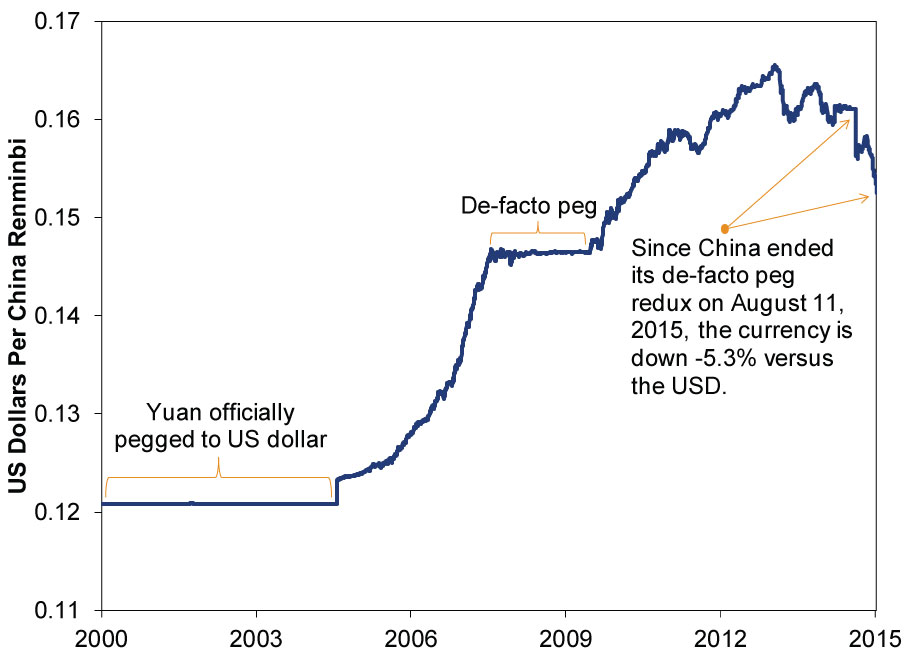

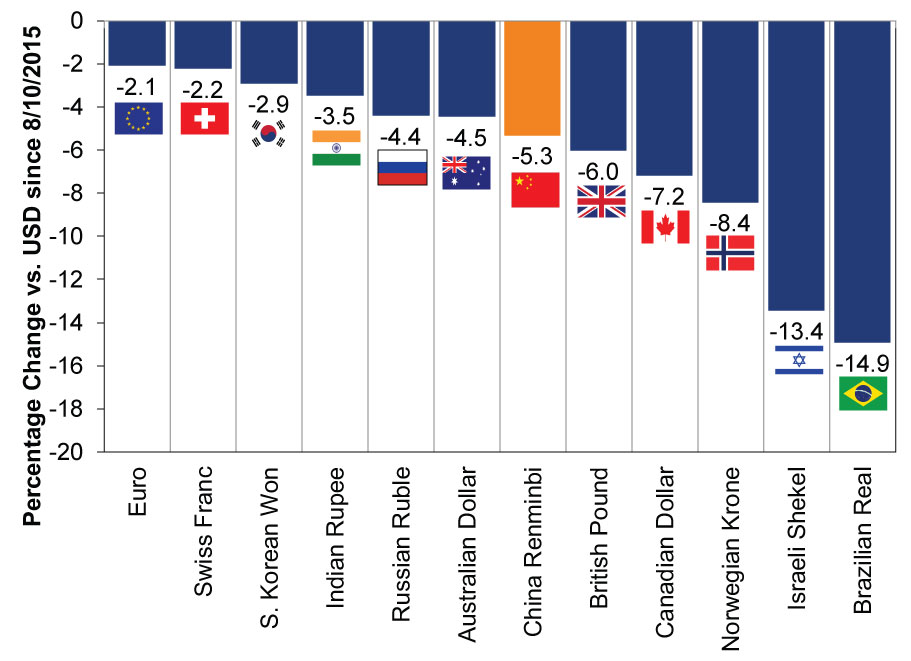

Exhibits 2 and 3 put the yuan's recent move into better perspective. Though it's down -5.3% versus the US dollar since last August 11 (as of 1/6/2016), it's still significantly higher than where it was for much of the 2000s. Also, that -5.3% decline is a lesser move than a handful of other world currencies over this period. Why don't folks fret the Israeli shekel falling -13.4% or the Norwegian krone dropping -8.4% over the same timeframe? The falling yuan gets attention solely because folks aren't used to it wobbling.

Exhibit 2: The Yuan Since 2000

Source: FactSet, as of 1/7/2016. US Dollars to China Renminbi, 12/29/2000 through 1/6/2016.

Exhibit 3: Selected Global Currency Declines Since 8/10/2015

Source: FactSet, as of 1/7/2016. Percentage change vs. the US dollar since 8/10/2015 for the euro, Swiss franc, South Korean won, Indian rupee, Russian ruble, Australian dollar, Chinese yuan, British pound, Canadian dollar, Norwegian krone, Israeli shekel and Brazilian real.

We won't waste pixels speculating on why the PBoC decided to do this-they're a black box, and we don't have spies on the inside. But it is worth noting the offshore currency market-which is more freely traded than the strictly controlled domestic market-valued the yuan about 2.2% lower versus the dollar than the onshore rate as of Wednesday's close. So for all the talk of China manipulating the yuan downward, this appears more like cushioning a depreciation. Make of that what you will, but in our view it is nothing more than market liberalization is a glacial process. As for worries about capital flight, this is a long-running trend. Officials have spent over half a year drawing down foreign exchange reserves to offset the outflows, yet their war chest remains huge and China keeps growing.

It's true you can't have free capital movement, a fixed exchange rate and sovereignty over monetary policy. There is a reason economists call this the impossible trinity, and China has hit speedbumps while trying to juggle its currency markets and capital controls. It will probably hit more speedbumps in the future. But speedbumps aren't crises, and the current situation would have to snowball for this to materially threaten China's economy. The current trickle of capital crossing the border and the yuan hiccups attract eyeballs, but this is a country with over $3 trillion in forex reserves.

Most of the sensationalism from this week misses a bigger and potentially more meaningful takeaway: China is gradually opening its economy to the outside world, something the Communist Party seems loath to do but is a positive long-term development. Allowing money to move outside its borders is likely to be a bumpy process given the overall size of China's economy. Officials have fueled uncertainty along the way with a series of policy decisions that didn't quite work as intended-to be expected in a largely trial-and-error process. But allowing capital markets to function more freely is always a good thing, in our view, and this is a small step toward that.

[i] FactSet, as of 1/7/2016. Price level percentage change in the MSCI China A and MSCI China H indexes on 1/4/2016.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary This Week in Review | Fed Meeting, US GDP, Eurozone GDP

2026-07-31

2026-07-31 -

Economics Q2 US GDP’s Stealthy Strength2026-07-31

-

Market Analysis Don’t Fret the EU’s Low Summertime Gas Storage Levels2026-07-31

-

Economics On Fires and GDP2026-07-30

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today