Personal Wealth Management / Market Analysis

Chinese Fundamentals: Likely Fine, Not Falling

Investors may be pleasantly surprised by China’s improving economic data.

China’s August economic results are in, and overall, the data showed continued improvement. The economy appears stable and growing at a healthy rate, and the long-dreaded hard-landing appears increasingly unlikely—an underappreciated positive for global markets.

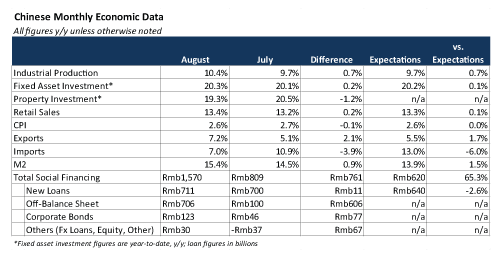

Nearly across the board, China accelerated and beat expectations—illustrating broad-based stabilization in the wider economy. Of particular note, industrial production had its best reading since March 2012, and together with China’s most recent PMIs, the results suggest Chinese manufacturing data are rebounding nicely. Retail sales were also robust and exports accelerated, with shipments to the US and EU up for the second consecutive month. On the whole, August economic data signal a fundamentally fine China—growth may be slowing from recent years, but that’s likely more a function of China’s gradual economic development than weakness.

Exhibit 1

Source: Thomson Reuters Datastream and Bloomberg

Perhaps the most interesting data point, though, was total social financing. Overall, credit came in considerably higher than expected, hitting a four-month high and nearly doubled from July, with the increase almost entirely concentrated in off-balance sheet lending. Shadow financing had dropped to RMB 100 billion in July as the government cracked down on shadow lending—much of which failed to reach the broader economy earlier this year. Looking ahead, a key question is whether officials simply overcorrected in July and are now permitting shadow financing at sustainable levels, or if plans to rein in profligate lenders were just talk and nothing has really changed.

Despite the August bounce, it’s unlikely lending will be an economic tailwind moving forward. Structural reform and liberalization of the financial sector and other key areas of the economy are among the new administration’s highest priorities as it transitions away from an investment-led growth model toward consumption. While the agenda creates short-term dislocations as the rules of the game change, economic policy will be increasingly focused on the quality of growth over quantity, which is more efficient and sustainable in the long-term. Thus, while August’s financing data may be an incremental positive for sentiment, I’d caution against drawing big growth implications from it.

But that doesn’t take away from other August economic data showing strength largely underestimated by general sentiment. Hard-landing fears linger, but they appear increasingly overwrought. With data firming, investors should soon see the country’s economic reality is better than they’ve believed. Not that China will see the double-digits growth of yore, but as it’s grown off a bigger base each year, the country still contributes considerably to global GDP and corporate revenues. Thus, as the reality of just-fine Chinese growth surpasses expectations, investors should gain further confidence in future corporate profitability globally, giving stocks a nice sentiment lift.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Corporate Information How You Benefit from Fisher Investments' Transparent Fee Structure

2026-08-04

2026-08-04 -

Corporate Information How Fisher Investments' High-Touch Service Helps You2026-08-04

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets — July 27 - July 312026-08-03

-

Expert Commentary 3 Things You Need to Know This Week | US Jobs, Trade Balance, Earnings Reports

2026-08-03

2026-08-03

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today