Personal Wealth Management / Market Analysis

Contrasting US and European ‘Reopening’ Plans

Different paths to easing business restrictions highlight a subtle shift in a key question for investors.

Late last week, the US and Germany announced plans to reopen their economies following weeks-long COVID-19-induced business closures—and the plans highlight rather different approaches. In short, Germany—and much of Continental Europe—seems to be moving faster than America’s very gradual, rather disjointed approach. It all highlights what we think is a matter worth watching going forward: the disparate progress toward lifting restrictions. We think this is key to the duration of business interruptions, which could drive either relief or disappointment for markets.

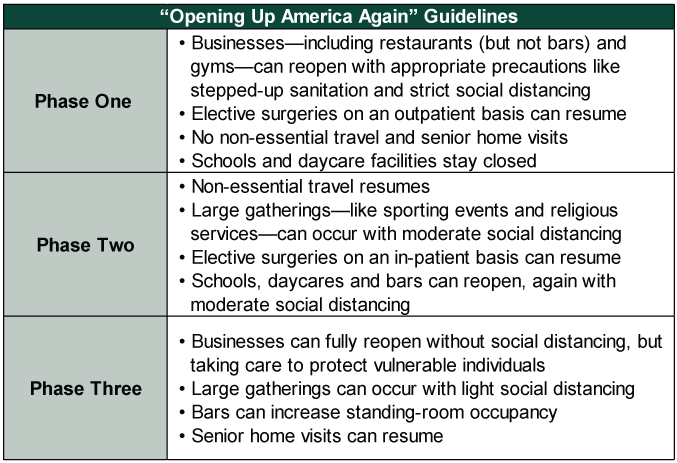

Last Thursday, citing slowing caseloads and ample hospital capacity, President Trump unveiled new White House guidelines for “reopening” America’s economy. The plan sets out a three-phase approach for states’ and municipalities’ lifting social distancing and other restrictions on business. But before they enter this, they must meet certain initial criteria, including:

- Falling positive COVID-19 tests and cases over 14 days

- Hospital readiness to cope with a potential resurgence in cases, including intensive care units

- Widespread testing availability to find asymptomatic COVID-19 carriers

- Tracing ability to track and contain emerging cases

Upon meeting these conditions, states and municipalities can then begin a phased reopening process summarized in Exhibit 1.

Exhibit 1: Federal Guidelines for Phasing Out Restrictions

Source: White House, as of 4/16/2020.

These guidelines highlight what will likely be a very gradual and uneven approach. In Thursday’s press conference unveiling the plan, President Trump stressed that state governors and local authorities were ultimately in charge of reopening their jurisdictions—which adds more uncertainty over timing. Some states, which already met the initial criteria, would be able to progress as soon as Friday—and three did, with Texas, Vermont and Minnesota announcing very small-scale reopening efforts that seem mostly symbolic to us. Many speculate Nebraska, North Dakota, South Dakota and Wyoming may soon enter a more complete phase one restart.

Yet quite a few states extended their lockdowns last week:

- Wisconsin extended its shutdown order to May 26

- New York to May 15, along with six other east coast states in its COVID-19 governors’ coalition (Connecticut, Pennsylvania, Delaware, New Jersey, Rhode Island and Massachusetts)

- Missouri to May 3

- Idaho, Tennessee and Michigan to April 30

- Georgia to April 29

- South Carolina to April 27

Perhaps Florida illustrates the divisions over this best. Friday, Governor Ron DeSantis lifted state-level restrictions on public use of beaches. But a day later, he announced that the state’s schools would be closed for the remainder of the school year. Whether this amounts to loosening or extending restrictions is, therefore, open to interpretation.

While California didn’t extend its shelter-in-place order, it doesn’t have to, considering the current one is indefinite. The state is also part of a West Coast governors’ pact with Washington and Oregon. Together with hard-hit New York and its East Coast coalition, they comprise about 38% of US GDP.[i] Without meeting even the initial requirements yet, their path forward is very unclear. If this large slice of US GDP remains largely offline, an economic recovery could take time to arrive, potentially making the lofty Q3 GDP forecasts we recently highlighted too optimistic.

By contrast, Continental Europe seems to be taking a faster approach to reopening. The latest country to announce measures is Germany. Similar to the US, German reopening requires coordination between federal and state governments. Chancellor Angela Merkel is working with Germany’s 16 state premiers to restart schools and businesses. Non-essential small businesses—shops less than 800 square meters—can reopen April 20; hair salons on May 4. Most schools are also set to reopen May 4, except for kindergartens and daycares, where social distancing is practically impossible to ensure. (However, the government will provide childcare services for small children whose parents return to work.) Outside of these limited categories, however, it is still unclear when other types of businesses and venues can reopen. Restaurants, bars, theaters, concerts, sporting events and religious services face indefinite lockdowns, with bans on large gatherings lasting at least through August.

All these details—the policy conditions to end lockdowns and the emerging timelines to do so—help set market expectations. But right now, they aren’t adding a lot of clarity. It will take time to see how the end of social distancing goes. If it is quick or even just slow and consistent, markets may have already seen their low. But a stop-and-start or very slow reopening with extended lockdowns in major metro areas could amount to reality missing expectations. Then too, expectations could also adjust—or overreact, if sentiment becomes too pessimistic on potential lockdown extensions. For now, we think it is too early to say—one reason among many that no one can yet be sure March 23 was the bear market’s low. But as the outlook becomes clearer, we think how expectations form in light of incoming policy details—and how that compares to the likely reality—will be key to what stocks do from here.

[i] Source: US Bureau of Economic Analysis, as of 4/17/2020.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary This Week in Review | Q2 Market Recap, June US Jobs, Trade Deal Update

2026-07-03

2026-07-03 -

Market Analysis Declaring Fed Independence Fears False2026-07-01

-

Market Analysis Why El Niño Doesn’t Necessitate Portfolio Shifts2026-07-01

-

Market Analysis Reader Mailbag: June 20262026-06-30

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today