Personal Wealth Management / Market Analysis

Crude Reality

US crude oil production is surging, but will allowing exports make gas prices do the same?

The oil industry has changed a wee bit since this picture was snapped in 1925. Photo by Hulton Archive/Getty Images.

The US is witnessing a revival! A renaissance! A revolution! Since 2005, US oil production has exploded (pun intended). Thanks to the ongoing shale revolution primarily based in North Dakota’s Bakken fields, Texas’s Eagle Ford and Texas and New Mexico’s Permian Basin shale deposits (among many others), US oil output has risen by about one Iraq since 2006. North Dakota’s oil production alone surpassed 1 million barrels of production a day in April, a 26.1% y/y rise! But if the US is so flush with crude oil, many wonder, why are gasoline prices not falling precipitously? If the shale revolution has helped—has it?—would less shale oil mean even higher prices? In other words, if Congress lifts the ban on crude oil exports, will the pain at the pump get even worse? We’ve seen those questions a fair bit lately, and a great Wall Street Journal op-ed gave the answer Thursday: Simply, crude oil isn’t gasoline! Many variables contribute to any price movement—for gas, domestic crude oil production is just one factor. Investors worried over pain at the pump shouldn’t fret over potential exports of US crude.

If US crude oil production and gas prices were as intertwined as most folks think, the relationship would be foolproof. Gas prices would fall as US crude production rises. But as Exhibit 1 shows, there is little correlation between oil production and gas prices—both are up big during the shale boom, telling us there is more to this story than meets the eye.

Exhibit 1: US Monthly Production of Crude Oil Vs. Average US Gas Prices

Source: US Energy Information Administration, as of 6/19/2014. Monthly US Field Production of Crude Oil and US All Grades All Formulations Retail Gasoline Prices, from April 1993 to March 2014.

US energy legislation and global markets can explain much of the disconnect. US crude oil exports are restricted by law—a never-repealed result of inflation fears and protectionist policy from the 1970s. But refined products—like gasoline—are open to the world. The US imports and exports the stuff, so our gas prices are largely set by global markets and their corresponding supply and demand forces. US crude is just one supply factor, and an imperfect one considering oil is refined for many other uses too. Local legislation matters for gas prices, too: For example, California’s reformulation requirements are a de facto ban on “imports” from other states, which cuts it off from cheaper gas around the country. Other states, like Michigan, require gasoline to have certain levels of octane, ethanol and/or fuel additives, limiting their supply options. Taxes also weigh, increasing real costs at the pump: Total US state and federal gas taxes average 49.9 cents/gallon—about 13% of today’s average gas price.

Gas prices have many more (and more meaningful) drivers than US crude, and so does gas supply. US crude production alone can’t meaningfully boost global gas supply—the infrastructure simply isn’t there to do so. To turn crude into gasoline, you have to refine it, but there is a big mismatch between US crude production and refining capacity. US refineries were built to process heavy (generally cheaper) crude oil imported from Mexico, Canada and Venezuela. Most shale crude, however, is a lighter grade that refineries can’t efficiently process. So they’re willing to purchase US crude only at a steep discount to make up for the extra production costs, disincentivizing business with US crude producers. Building refineries specially equipped for shale oil could help, but building the facilities and infrastructure (obtaining the licensing and other logistics) could take years.[i]

Transportation infrastructure creates another bottleneck for crude oil producers. Most US refineries are along the Gulf of Mexico in Texas, Louisiana and Mississippi or in the Midwest around the Great Lakes. But the oil comes from North Dakota, Colorado, Wyoming, Oklahoma and the inner Northeast—relatively new geographies for oil production, so robust transport routes just aren’t there. Trains have been the transportation of choice so far, but they aren’t ideal—issues include environmental concerns if they derail. And other potential options—*ahem* the Keystone pipeline—haven’t been able to supplement shipping needs.

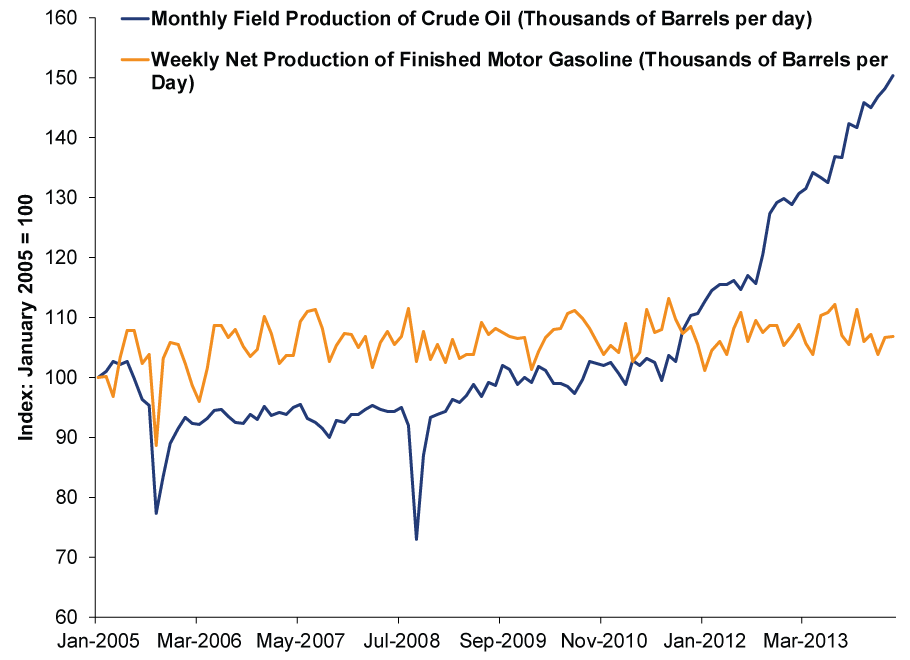

Because of these hangups, US gasoline production hasn’t matched crude’s rise. As shown in Exhibit 2, net gasoline production is merely stable. It didn’t jump with shale.

Exhibit 2: Crude Oil Production vs. Gasoline Production Since 2005

Source: US Energy Information Administration, as of 6/20/2014.

Lifting the ban on crude oil exports and opening the market to the global economy, though, could help this—there are plenty of refineries outside the US that can handle the light crude that comes from shale. End the restriction, let firms export, and shale oil becomes gasoline that much easier, boosting total supply globally—good for prices.

At least, in a perfect world—there are a lot of other variables here, like potential supply disruptions in other big producers. It’s too far in the future to game. Still, in our view, any steps toward a more efficient energy market would be a long-term, if incremental positive. For investors, not only would oil producers benefit from having a new global market to tap—likely helping revenue-growth light oil producers—but it would also reduce the probability of a 1970s-style oil and gas shock.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary This Week in Review | Fed Meeting, US GDP, Eurozone GDP

2026-07-31

2026-07-31 -

Economics Q2 US GDP’s Stealthy Strength2026-07-31

-

Market Analysis Don’t Fret the EU’s Low Summertime Gas Storage Levels2026-07-31

-

Economics On Fires and GDP2026-07-30

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today