Personal Wealth Management / Economics

Dazed and Confused by Inflation?

Don't fret inflation; America is worlds away from the 1970s.

High inflation, like bell bottoms, probably isn't coming back. (Photo by Tom Kelley Archive/iStock by Getty Images.)

Inflation isn't running too hot or too cold nowadays-it's just about right. Depending on your measure-so many to choose from!-US inflation is 1.5% y/y - 2.1% y/y. Nevertheless many folks are hyper-focused on it, fearing a 1970s inflation rerun is imminent with the Fed allegedly printing so much money, unemployment so low or consumer credit galloping. Or, or, or. Whatever the case, they think high inflation will wallop stocks. But US inflation isn't problematic now and we believe fears of where it will go-as well as the potential impact on stocks-are overwrought.

Inflation is widely misunderstood, even among economists. As Milton Friedman famously described, inflation is always and everywhere a monetary phenomenon: Too much money chasing too few goods and services. Yet many economists claim inflation depends on how close we are to "full employment"-tying price changes to wages. But there is little clear evidence of such a relationship. The Fed thinks unemployment at 4.5% - 4.8% should spur price gains, yet inflation is slowing alongside 4.3% unemployment.[i] Some Fed people are now questioning their own models and assumptions, which makes sense. As our pal Milton showed in the late 1960s, employers compete for workers with inflation-adjusted compensation. Thus, saying wages drive inflation amounts to saying inflation drives inflation, which isn't true. The so-called wage-price spiral is a myth.

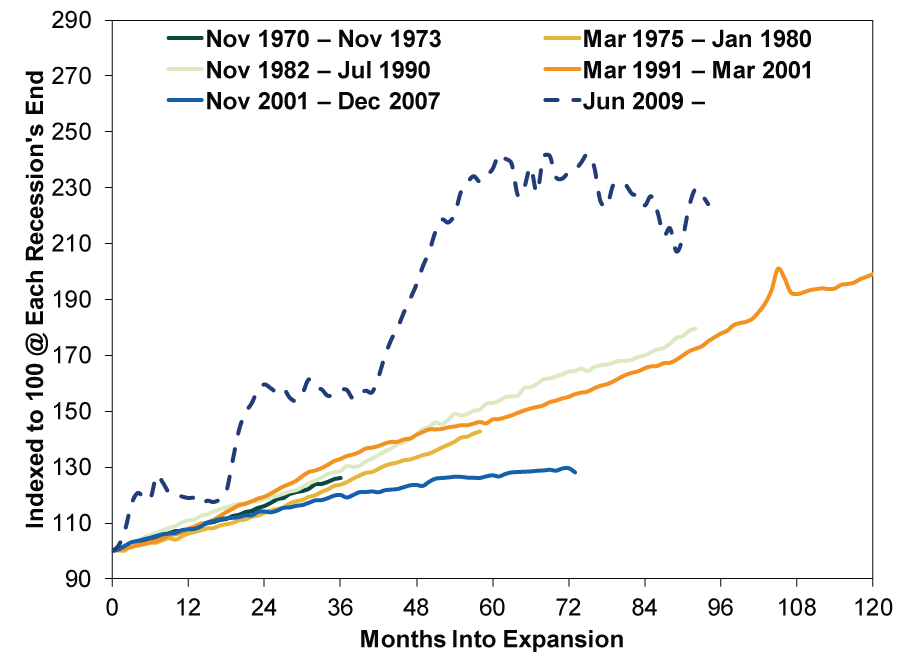

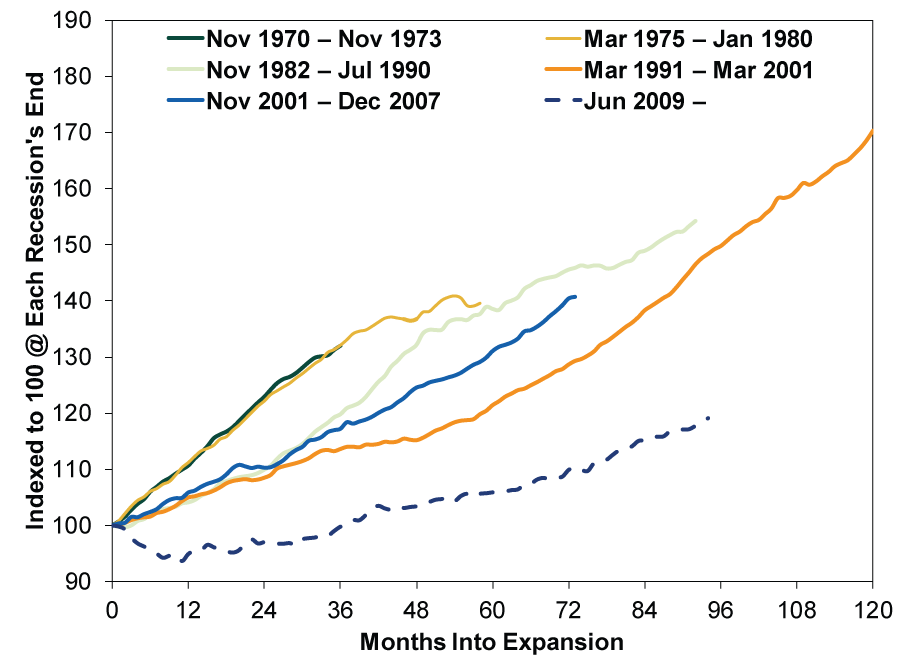

Still others argue currently low inflation is mysterious because the Fed has allegedly printed oodles of dough. Yet the Fed doesn't print money-or even influence money supply all that directly. The private banking system creates most money. Through quantitative easing (QE), the Fed created bank reserves, which it used to buy assets from banks. But most of that is sitting on bank balance sheets. The increase in broad money supply comes only if banks use those reserves to back new loans-how banks create new money. For every $10 in reserves (whether Fed reserves or customers' deposits), a bank can "create" $9 through new loans, which can in turn underpin more loans downstream. While QE's bond buying sent reserves soaring, it also lowered long rates, narrowing the gap between those and short-term rates. That made lending less profitable. Unsurprisingly to us, broad money supply grew tepidly in this cycle. (Exhibits 1 and 2) Inflation could rise some if bank lending surges before the Fed can sop up those excess reserves, though banks have their own reasons for wanting cash-rich balance sheets. Assuming sky-high inflation is around the corner is very premature.

Exhibit 1: Cumulative Monetary Base Growth

Source: Federal Reserve Bank of St. Louis, National Bureau of Economic Research, as of 8/16/2017.

Exhibit 2: Cumulative Broad Money (M4) Growth

Source: Center for Financial Stability, National Bureau of Economic Research, as of 8/16/2017.

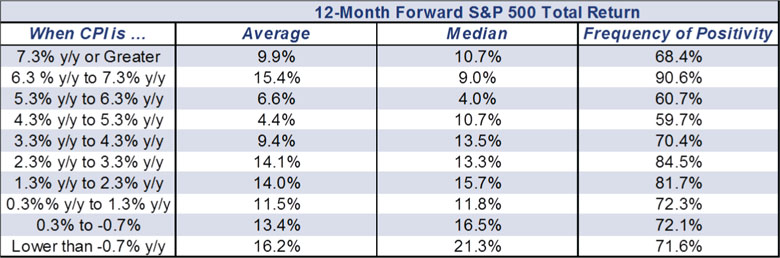

Even if inflation does rise, that doesn't inherently mean very much for stocks' direction. Inflation is key for bonds. Most bonds pay a fixed rate of interest. If inflation jumps, the fixed rate loses purchasing power. This leads bond investors to demand higher rates to compensate, and bond prices and yields are inversely correlated. Stocks, however, have no such direct connection. Stocks' earnings are nominal; so are their prices. How they move is much more about the gap between sentiment and reality than anything. Exhibit 3 shows S&P 500 forward 12-month total returns during various periods of inflation at 1 percentage point intervals from its long-term average, 3.3%.[ii] The results show largely what we'd expect: Stocks rise much more often than they fall in 12-month stretches, so averaging them out shows positivity across the board-no real[iii] influence. Underscoring this, lowflationary and deflationary periods post the best median returns of the bunch: Those occurrences cluster mostly around the end of recessions, as deflation tends to occur late in a downturn. Forward-looking stocks tend to jump at about that point-before recessions end.

Exhibit 3: S&P 500 Price Returns During Low and High Inflation Regimes

Source: Global Financial Data, Inc., Federal Reserve Bank of St. Louis, as of 8/15/2017. Forward 12-month S&P 500 total returns (calculated monthly) and headline Consumer Price Index (year-over-year), January 1914 - August 2016 (there are no forward 12-month periods complete later than this point).

Many baby-boomer investors may look at that exhibit and say, "yah, but the 1970s!" An understandable reaction! For many in that generation, this was their early adulthood. Given it is modern America's most inflationary episode, many anchor their recollections of inflation to this extreme period of prices rising double-digits. But it is worth recalling how the decade actually transpired-for inflation, the economy and stocks. For one, high inflation didn't come super suddenly. The Consumer Price Index pierced 4% y/y in June 1968-and rose further from there. Most of this is tied to monetary policy that remained too loose for too long, even when prices rose. To battle it, the government did the exact wrong thing: Nixon's price controls. Fixing wages and prices in August 1970 stifled production as price signals (and incentives) went haywire. Nixon strong-arming then-Fed head Arthur Burns into keeping interest rates low compounded the problem. OPEC's October 1973 oil embargo boosted oil prices. In April 1974, when the administration abandoned controls, the shortages and rationing that followed launched inflation skyward-an unintended, but also predictable, consequence of heavy-handed government meddling.

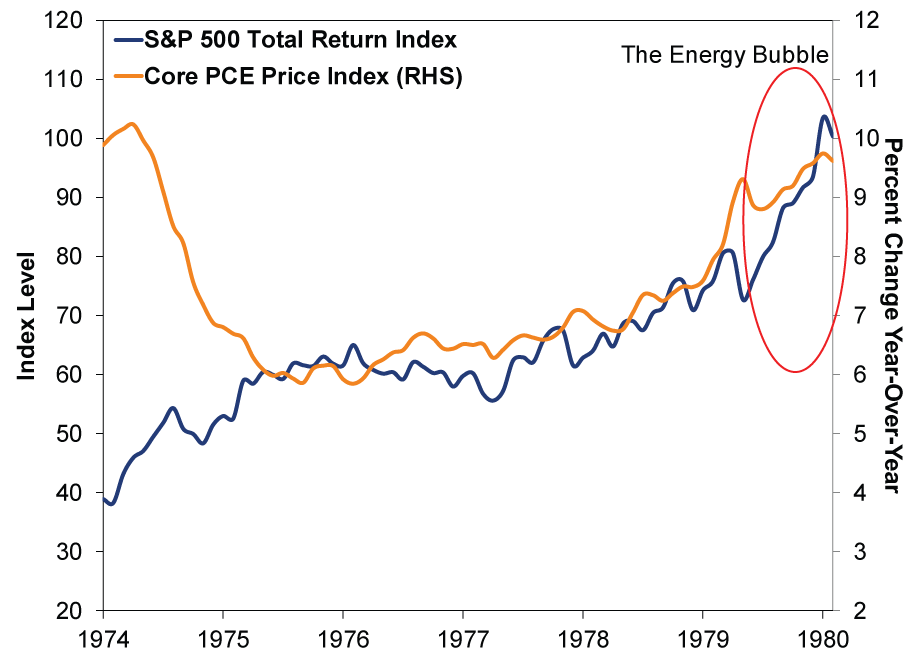

All this negativity, perhaps a bit exacerbated by Watergate, triggered the 1973 - 1974 bear market and recession, which coincided with rising inflation. But it is more likely stocks fell in anticipation of the recession and inflation brought by those poor policy choices than inflation alone. Stocks bottomed in November 1974, before the recession ended and while inflation was at 7.4% y/y-more than four percentage points above its 3.3% y/y average from 1914 to 2017. Inflation remained above that long-run average for the remainder of the decade, peaking in 1980 at 14.8%. Stocks mostly drifted higher for the balance of the decade, before the Energy Bubble inflated and burst, as then Fed-head Paul Volcker fought a renewed resurgence in inflation by hiking rates far and fast. So to sum up: Government policy to battle inflation can wreak havoc on stocks. But inflation, even high inflation, isn't automatically bearish.

Exhibit 4: Stocks Not Always Hurt by High Inflation

Source: Global Financial Data, Inc., Federal Reserve Bank of St. Louis, as of 8/21/2017. S&P 500 total return index and Personal Consumption Expenditures excluding Food and Energy Price Index, November 1974 - December 1980.

[i] Using the Fed's latest "longer run central tendency" unemployment projection (which they've continually adjusted lower throughout this cycle).

[ii] Stock returns from 1914 to 1926 are not hugely reliable, in our view, but we include them here in the sense that the BLS takes inflation data back to 1914 and we wanted to be complete.

[iii] That is an inflation joke for you econonerds.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Politics Blunting Burnham?2026-07-21

-

Market Analysis Why the SOX “Bear Market” Isn’t Foreboding2026-07-21

-

Expert Commentary 3 Things You Need to Know This Week | Q2 Earnings, ECB Meeting, Trump Accounts

2026-07-20

2026-07-20 -

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—July 13 - July 172026-07-20

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today