Personal Wealth Management / Politics

Debunking Yellen’s Yellin’ About the Debt Ceiling

Treasury Secretaries’ engaging in debt ceiling hyperbole is an old tradition.

Editors’ Note: MarketMinder is politically agnostic. We favor no politician nor any political party and assess political developments for their potential economic and market impact only.

Welp, looks like summer isn’t the only thing ending this week. According to a Wall Street Journal op-ed from Treasury Secretary Janet Yellen this week, the US government will soon have exhausted its so-called “extraordinary measures” to keep meeting all spending “obligations” without taking on more debt, leaving Uncle Sam with no more room under the debt ceiling. Like pretty much every politician jawboning about this today, she alleges this means America will “default on its obligations,” and pundits have let the claim stand untested. Without wading into the political fight here, please let us set the record straight, if only so that investors don’t panic unnecessarily.

We do this not to single out Yellen amid today’s noise or relative to her predecessors at the Treasury, for they have all done this. Saying failure to raise the debt ceiling leads to default is a rite of passage for Treasury Secretaries. Steven Mnuchin and Jack Lew each did it, as did Tim Geithner before them. If you somehow make it through your stint without engaging in this particular exaggeration and wordplay, then you are apparently a bit of an outlier. So in other words, our beef here is with the time-honored conceit—not the latest person engaging in it. Actually, she has our deepest sympathies, as making this sort of argument publicly probably hurts intellectually.

Here, specifically, is what the op-ed says:

In a matter of days, millions of Americans could be strapped for cash. We could see indefinite delays in critical payments. Nearly 50 million seniors could stop receiving Social Security checks for a time. Troops could go unpaid. Millions of families who rely on the monthly child tax credit could see delays. America, in short, would default on its obligations.

The U.S. has never defaulted. Not once. Doing so would likely precipitate a historic financial crisis that would compound the damage of the continuing public health emergency. Default could trigger a spike in interest rates, a steep drop in stock prices and other financial turmoil. Our current economic recovery would reverse into recession, with billions of dollars of growth and millions of jobs lost.[i]

It is a timeless bit of rhetorical gymnastics. Indeed, if the Treasury exhausts extraordinary measures, there are some things it won’t be able to pay. The op-ed enumerates some of them. But curiously absent from that list? Repayment of bond principal and interest payments on outstanding government debt. Failure to do that is the technical definition of default. The op-ed, cleverly, does not outright say we will default on debt. Rather, echoing past Treasury Secretaries and the vast majority of politicians on both sides of the aisle, it simply redefines “default” as applying to all federal accounts payable. Then it jumps from there to a paragraph that is squarely about debt default without announcing the topic change.

The difference here is more than just semantics. The US government not paying a supplier or cutting select entitlement payments on time isn’t a credit event. It isn’t good, mind you—we aren’t arguing anything close to that. But drawing equivalence between borrowing to pay the monthly child tax credit to paying interest on bonded debt is going too far, in our view. See it this way: The government can unilaterally change the terms of entitlements, and Americans would have little recourse (other than a vote). It is almost akin to changing your kid’s allowance. If you miss paying your kid’s allowance one week, you have not defaulted. It will not affect your standing with your bank and your ability to get a loan. If you fail to pay interest on your mortgage or credit card on time, that has different ramifications.

One grand irony here is that while the second paragraph rightly says America has never defaulted—and that an actual default would be quite bad—it implies to the casual reader, through its fuzzy verbiage, that America has never missed the obligations in the preceding sentence. That isn’t really true, considering those items are more in line with a government shutdown. We have had a couple dozen of those over time, and none had the dire consequences described. None caused a recession. None caused a bear market. None made interest rates soar and stay there. None made it impossible for the Treasury to tap capital markets. None made millions of jobs disappear.

In our view, it is important for investors to understand all this for what it is: politicking. You, dear reader, likely aren’t the op-ed’s primary target audience. The real audience is Congress—the goal here, as with all past debt ceiling showdowns, is to use heightened language to goad Congress into action. It arrives via interviews and newspaper articles, rather than strongly worded letters to lawmakers, to add some urgency and remind Congresspeople that they don’t want to have to answer for a prolonged standoff at midterms next year. It is also probably an effort to stake out talking points and an angle for the midterms in case there is a prolonged standoff.

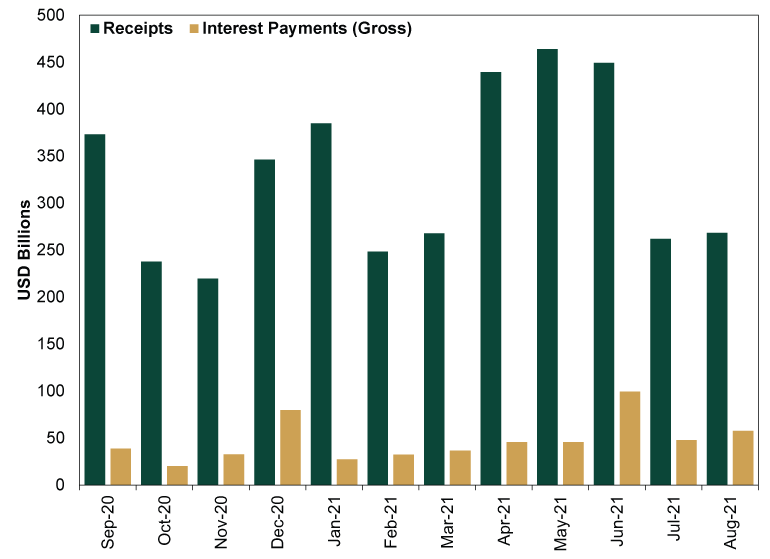

Therefore, we encourage you to stay above the fray and focus on what truly matters: the exceedingly low likelihood of an actual default even if Congress stalls for a long while. Bond principal payments are covered, as hitting the debt ceiling doesn’t prevent the Treasury from issuing new debt to refinance a maturing bond. That leaves interest payments, which the Treasury can manage easily. Exhibit 1, which refreshes a chart we ran in July, shows interest payments and tax revenues in each of the past 12 months. Even with revenues being a bit lumpy due to the timing of estimated tax payments and other factors, they dwarf interest expenses each month, with plenty left over for a good number of other accounts payable. Considering the Treasury has both the ability to prioritize interest payments over all others and a de facto Supreme Court mandate to do so, via the justices’ interpretation of the 14th Amendment, an actual default is incredibly unlikely.

Exhibit 1: Federal Revenues Still Dwarf Interest Payments

Source: US Treasury, as of 9/20/2021.

While debt ceiling standoffs aren’t bearish, they do sometimes hit sentiment and contribute to market volatility. Some argue this contributed partly to Monday’s big wobble, along with events in China (see our coverage of that here). In our view, that makes seeing through the political fog crucial. Don’t let hyperbolic coverage fool you into making knee-jerk portfolio reactions. Keep your head firmly in reality, look past short-term volatility and stay focused on your long-term goals.

[i] “Janet Yellen: Congress, Raise the Debt Limit,” Janet Yellen, The Wall Street Journal, 9/19/2021.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis The New Tariffs in Town Are Still Old News2026-07-24

-

Expert Commentary This Week in Review | Market Volatility, Tariffs, SpaceX

2026-07-24

2026-07-24 -

Expert Commentary Why Ken Fisher Is Optimistic About European Stocks

2026-07-23

2026-07-23 -

Economics A Summertime Check-in on US Consumers2026-07-23

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today