Personal Wealth Management / Economics

Digging Into Earnings

Q1 earnings season is winding down. What do the data show?

Some folks seemingly fixate on slow GDP growth and suggest stocks’ rise in recent years has been “too fast” and detached from economic reality—a credit-fueled bubble, perhaps. Yet earnings tell a very different tale. And the next chapter is seemingly being written as we speak.

With 451 S&P companies reporting as of Friday, Q1 2013’s earnings season is winding down, and thus far the story is unchanged from recent quarters. While earnings growth rates may have slowed, analysts’ estimates are simply proving too dour. Of the firms reporting thus far, 67% topped analysts’ estimates—above the long-term average of 63% and matching the average over the last four quarters. The overall growth rate is 5.3% y/y—but that’s far ahead of start-of-quarter estimates predicting 1.5% growth. And actually, four years into a bull market and economic expansion, that’s pretty solid growth. After all, earnings aren’t rebounding from a low trough like they were in the bull market’s heady early years—they’re building upon record highs.

Revenues on average have been less robust in the quarter. In fact, rounded to the nearest whole number, the growth rate has been zero percent, and the percentage of firms beating has slowed to less than half.

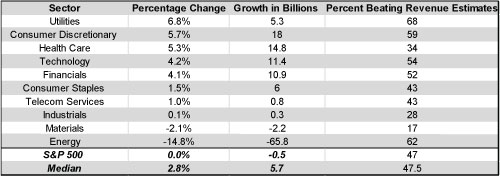

However, the data are more interesting under the hood. The median sector grew revenues 2.8% y/y in Q1—slower than Q4 2012’s 4.1% median revenue growth. This was weighed down greatly by two sectors’ declining revenues—Energy and Materials—heavily impacted by declining commodities prices. Also highly cyclical, the Industrials sector managed 0.1% y/y growth. While this decline was seemingly expected for Energy—62% of firms beat revenue growth estimates, only 28% of Industrials and a paltry 17% of Materials firms beat. Hence, it may be somewhat odd to look at the headline rate and not the moving parts underneath. In fact, the other seven S&P sectors logged 4.0% y/y revenue growth. Exhibit 1 shows S&P 500 sectors ranked by reported Q1 year-over-year revenue growth.

Exhibit 1: Year-Over-Year S&P 500 Revenue Growth by Sector

Source: Thomson Reuters, This Week in Earnings, 05/10/2013; Fisher Investments Research.

Ultimately, this makes sense in the grand scheme of this bull market. Early, as cyclical firms cut costs and see incremental increases in business, revenues jump higher. But as the cycle matures, comparisons get much harder (true for the broader economy as well). This likely weighs on cyclical firms’ earnings in maturing bull markets—particularly since cost-cutting likely already occurred and ran its course at such economically sensitive firms. The slowing growth rate of maturing cycles likely doesn’t favor such firms—instead, firms with greater cost controls in less cyclically sensitive fields seem likely to lead. This is a factor favoring mega-cap stocks.

Mega-cap firms are concentrated in less cyclical industries, and, given their significant economies of scale, they have the ability to better manage the bottom line in an era of weakening (though still growing) top-line sales. And you can see this in the data: the mega-cap stocks reporting thus far have beaten earnings at a better clip than non-mega cap stocks (67.4% vs. 61.5%), despite mega-cap sales missing more often. They’re simply managing costs better than analysts fully appreciate.

Overall, we’d suggest this is an environment supportive of those firms with more earnings growth stability—those, on average, of higher quality and higher return on equity—mega-cap stocks.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Economics Quick Hit: Durably Broad-Based Growth2026-07-29

-

Market Analysis On the Chop in the Oil Market2026-07-29

-

Politics Takaichi Raises Japan’s Wall of Worry2026-07-27

-

In The News Why Kevin Warsh should think twice about hiking interest rates — even as anxiety over the Iran war grows2026-07-27

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today