Personal Wealth Management /

Does the US Stand Taller With a Strong Dollar?

Does a stronger dollar mean anything for the economy or stocks?

Cue the John Phillip Souza! The dollar is on the march higher lately, strengthening against most major currencies worldwide. And according to some, that's proof the US economy has a leg up over the rest of the world! But currency strength or weakness doesn't tell you much about economic vibrancy-and it tells you nothing about stock market direction. Our bullish outlook has nothing to do with the expected rise or fall of the greenback.

Currencies only move relative to one another, so arguably the best gauge of what "the dollar is doing" is the Broad Trade-Weighted US Dollar Index, which tallies the moves of the dollar versus 26 other major currencies, weighted by our total trade in each. Since reaching its low for the year on July 9, the dollar has risen fairly consistently versus most currencies. The Broad US Dollar Trade Weighted Index is up in seven of the last nine weekly reads, with the currency up over 2% during the span.[i] A narrower gauge measuring the USD against six currencies is up more, over 5% in the same period.[ii](Unsurprisingly, most media accounts cite this second, bigger figure. More eye catching, we guess.)

The punditry's explanations for these moves are many and varied. Some cite "political shocks" elsewhere-Iraq, Ukraine, the Scottish referendum-and claim these events made the dollar look that much greener. Others cite the eurozone's uneven recovery. The US is their "safe haven,"[iii] if you will, from these global trouble spots. To many, a strong dollar also makes the US economy far more attractive than its peers.

This is all a pretty ironic twist on the whole "weak-currency-is-better" meme of the last few years. People figured you needed a weak currency to give exports a big boost-goosing the economy. Bestselling books argued countries would consistently one-up (one-down?) each another in an effort to weaken. Japan specifically targeted a weak yen. In the UK, some worried the pound was far too strong. Just last week some thought ECB President Mario Draghi's secret motive was to weaken the euro. Heck, this is why folks feared a strong dollar in the 1990s! Which was in turn ironic when people feared a weak dollar in 2004 and 2005!

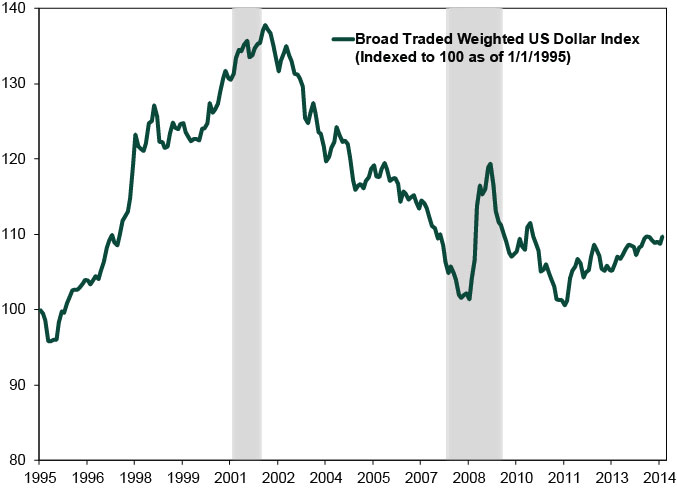

The truth, as one might surmise from these contradictory theories, is currency swings don't tell you much about a country's economic health. Hence, each side has plenty of evidence to support its case. The dollar began the last recession (December 2007 - June 2009) weak, until the panic hit and the greenback surged. But before the recession ended, the dollar weakened anew-and kept right on unevenly weakening until 2011. Then it began strengthening. In the 1990s expansion and 2001 recession the dollar overall rose throughout. Throughout the 2002 -2007 expansion, the dollar was falling relative to the broad trade-weighted index. Currencies sometimes rise with the economy and other times don't; and they sometimes fall during recession until they don't. (Exhibit 1)

Exhibit 1: Broad Trade-Weighted US Dollar Index

Source: Federal Reserve Bank of St. Louis, as of 09/14/2014. 01/01/1995-09/14/2014. Gray shading denotes official US economic recessions, as dated by the National Bureau of Economic Research.

Currency swings also don't tell you how the rest of the world is doing compared to the US. For instance, the euro is currently weak compared to the US dollar. And people attribute this to a relativelyfrail eurozone economy. But a currency's relative price isn't determined by its relative economic standing. While sentiment can drive currency wiggles in the short term (as it can cause any market to gyrate), supply and demand are generally the primary drivers of the dollar's relative strength over time. Since central banks control money supply, monetary policy has a big influence. Tighter monetary policy typically means a slower-growing money supply and higher rates, which investors like-often moving the exchange rate higher. Folks value rarity and higher yields! Looser monetary policy tends to have the opposite effect, and since June, the ECB has been loosening. Euro-denominated bond yields are largely down across the board, and many now yield less than their US counterparts. That, coupled with folks' expectations for the Fed winding down quantitative easing, likely makes the US dollar relatively stronger.

Regardless, a strong (or weak) dollar has no meaningful correlation to stocks. The dollar was weak relative to a broad basket of foreign currencies in 2004, 2006 and 2007-and stocks rose! And it was strong in 2001 and 2008 when stocks fell. The dollar was also weak in 2002-stocks fell. And strong in 2005-stocks rose. It was weak in a majority of 2009-stocks jumped up again. Further, since Q1 1995, the S&P 500 Total Return Index has risen 54 of 77 quarters. Of those 54 quarters, the dollar was up 28 times and down 26. Basically a coin flip! When the S&P was down, the dollar was up 12 times and down 11. Again, coin flippy![iv]

Listen, we're plenty optimistic about markets and the economy-and we expect the US to lead. But not because the dollar is strong, which historically won't indicate direction. There are just so many more inputs that go into what moves the economy and markets.

[i] Source: Federal Reserve Bank of St. Louis.

[ii] Ibid. That means the same as the above. Which we probably could have just typed at this point.

[iii]This term, frequently repeated in the media, is pretty much meaningless. Show us a safe haven, we'll show you a risk to it.

[iv] Source: FactSet, as of 09/15/2014. S&P 500 Index Total Return Level, 12/30/1994-03/31/2014. Federal Reserve of St. Louis, as of 09/15/2014. Trade Weighted US Dollar Broad Index, 01/01/1995-04/01/2014.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary This Week in Review | Global PMIs, SpaceX, RMD Planning

2026-07-10

2026-07-10 -

Market Analysis Trim Your Angst on Economic Measurement Tweaks2026-07-09

-

Politics Long-Term Forecasts and Court Verdicts: The Latest in British and French Politics2026-07-09

-

Corporate Information How You Benefit from Fisher Investments' Transparent Fee Structure

2026-07-08

2026-07-08

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today