Personal Wealth Management / Market Analysis

Don't Overrate the Eurozone Slowdown

Slowing in recent economic data has many fearing last year’s eurozone growth was a sugar high—a sign of dour sentiment.

IHS Markit’s eurozone Purchasing Managers’ Indexes (PMIs) ticked down and missed expectations in May—building on a trend dating back to February. Q1 2018 GDP growth slowed, as did April retail sales, which also missed expectations.[i] These slowing data—combined with fear surrounding Italian politics—lead many to believe the eurozone is weakening. Possibly even sliding toward recession! Last year’s acceleration? A pipe dream, they claim. Hence, sentiment tallies like ZEW’s surveys are plunging and the financial media is full of fearful headlines. In our view, this is overwrought. The negative reaction to expansionary data shows investor sentiment remains overly dour towards the eurozone—typically a bullish cocktail.

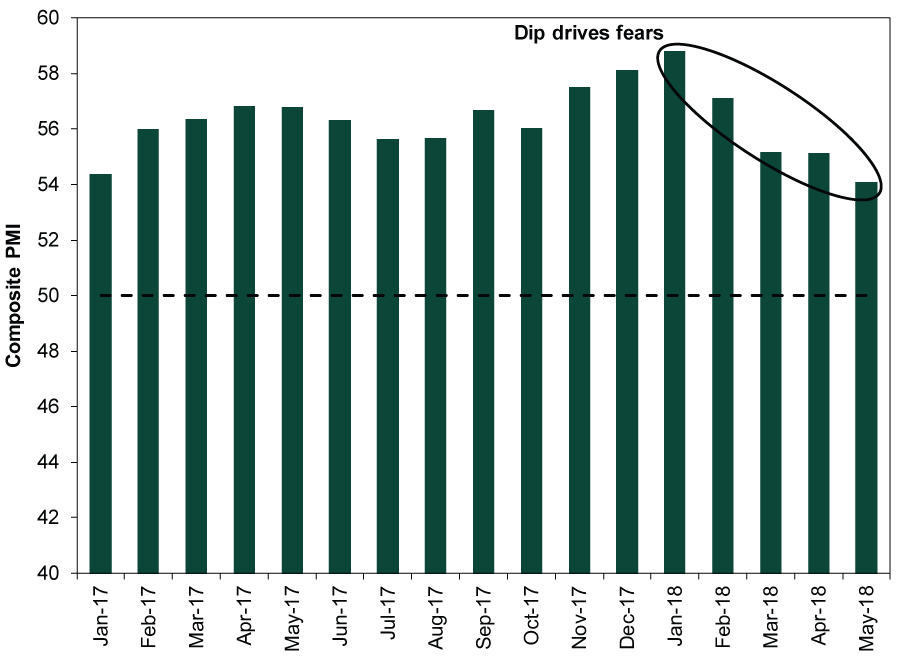

Exhibit 1: Eurozone Composite PMI Dips

Source: FactSet, as of 6/5/2018. IHS Markit Eurozone Composite Purchasing Managers’ Index, January 2017 – May 2018. Dotted line (50) represents divide between growth and contraction.

Exhibit 1 shows the Composite PMI (which combines manufacturing and services) since last January--you can easily see the attention-grabbing downtrend since February. Headlines warn "Eurozone Data Signals Recovery Has Peaked" and "Euro Zone Business Slowdown Suggests Best Days May Be Over." One analyst went so far as to quip that, "[regarding eurozone growth] we, unfortunately, might have to refer to the famous Looney Tunes catchphrase 'That's all folks!'"

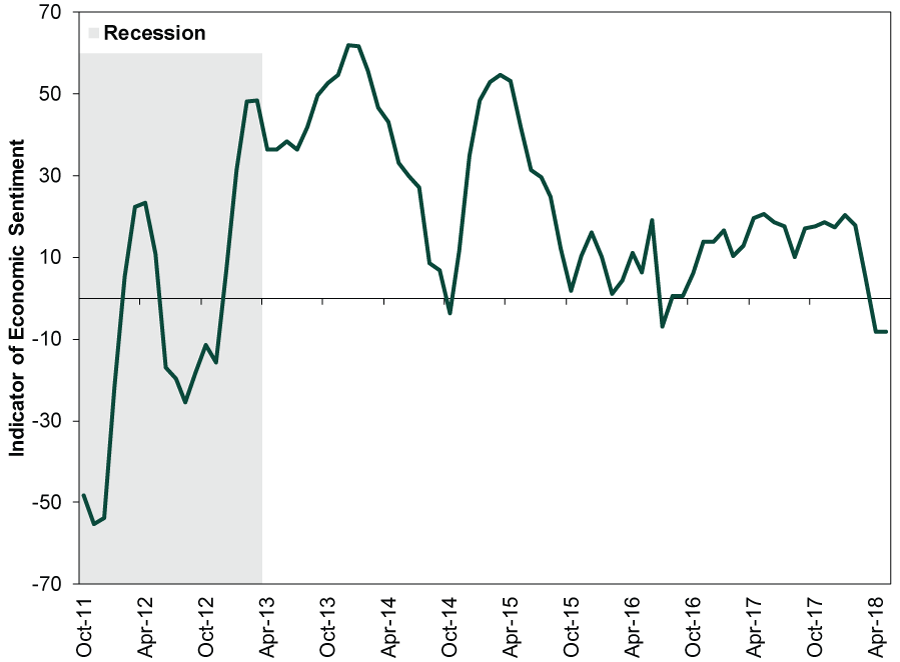

Sentiment surveys echo this gloomy outlook. The Eurozone Sentix Investor Confidence survey has fallen in every month this year. Germany’s ZEW Indicator of Economic Sentiment—a widely followed survey of German business leaders—fell to levels not seen since November 2012, during the eurozone debt crisis.

Exhibit 2: German Sentiment Hits Multi-Year Lows

Source: FactSet, as of 5/30/2018. ZEW Indicator of Economic Sentiment, September 2011 – May 2018. Shaded area represents eurozone recession per the Centre for Economic Policy Research, as of 6/5/2018.

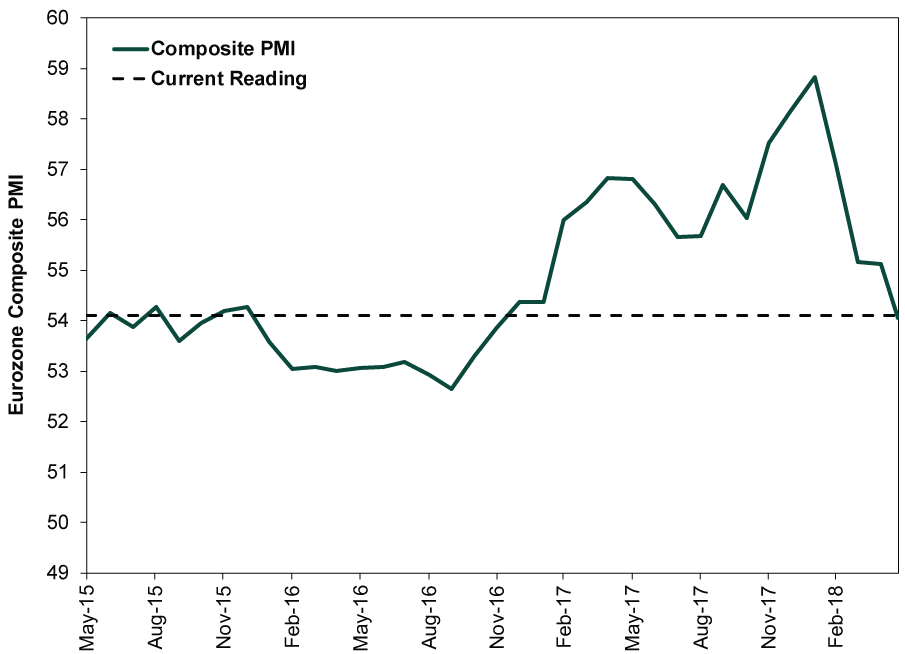

However, like plenty of other eurozone economic data, PMIs remain expansionary, and it isn’t unusual to see data series fluctuate—up and down—during an expansion. PMIs are surveys, with the reading being the percentage of responding firms reporting expansion. May’s 54.1 reading easily clears 50, indicating more firms grew than contracted—generally, a sign expansion continued. Also, PMI surveys measure only the breadth—not the magnitude—of growth. Hence, it is possible lower PMIs obscure accelerating growth, if that growth is concentrated. So the downtick suggests growth narrowed, but it says little about the strength—or weakness—of said growth.

Now, many acknowledge these data are expansionary. But they project the decline forward—concluding contraction looms. But PMIs (like basically all economic data) aren’t serially correlated. As Exhibit 3 shows, there have been several downtrends in recent years that later reversed. Further, current PMI levels are still higher than much of 2015 and 2016, when the eurozone economy grew fine.

Exhibit 3: PMIs Are Volatile but Remain Expansionary

Source: FactSet, as of 6/7/2018. IHS Markit Eurozone Composite Purchasing Managers’ Index, May 2015 – May 2018.

Moreover, while Composite PMIs fell in France and Germany, Spain’s rose to a three-month high and Italy’s was unchanged. That doesn’t mean you should ignore the eurozone’s two biggest economies, but it shows the currency bloc isn’t uniformly trending into an abyss. While many bemoan the weaker figures, there are caveats to consider. As IHS Markit noted, “While prior months have seen various factors such as extreme weather, strikes, illness and the timing of Easter dampen growth, May saw reports of business being adversely affected by an unusually high number of public holidays.”

Meanwhile, forward-looking measures like PMIs’ new orders sub-index, The Conference Board’s eurozone Leading Economic Index (LEI) and positively sloped yield curves point to continuing growth. Like headline PMIs, new orders’ slowdown doesn’t change the fact the gauge is still in expansionary territory. Meanwhile, eurozone yield curves, one of the most forward-looking indicators going, remain nicely positively sloped. As of June 4, the spread between 10-year government bonds and overnight rates in the four largest eurozone economies (Germany, France, Spain and Italy) was moderately positive, ranging between 0.41 and 2.56 percentage points.[ii] The 10-year minus 3-month spread is even wider, due to negative deposit rates’ influence in the eurozone. Because banks borrow short term to fund long-term loans, the fact long rates are nicely above short rates means lending is profitable. That is an incentive for them to lend, increasing the likelihood businesses are able to access capital to fund future growth.

In other words, though reaction to data is dour, reality is far brighter—and should remain so. Such a backdrop provides an easy hurdle for the healthy eurozone economy to clear. And, should that materialize, the resulting positive surprise to folks expecting further weakening from here should provide a tailwind to eurozone stocks.

[i] Eurostat, as of 6/5/2018. Q1 2018 eurozone GDP and April 2018 eurozone retail sales volumes.

[ii] FactSet, as of 6/4/2018. German, French, Spanish and Italian yield spreads.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Politics Blunting Burnham?2026-07-21

-

Market Analysis Why the SOX “Bear Market” Isn’t Foreboding2026-07-21

-

Expert Commentary 3 Things You Need to Know This Week | Q2 Earnings, ECB Meeting, Trump Accounts

2026-07-20

2026-07-20 -

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—July 13 - July 172026-07-20

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today