Personal Wealth Management / Market Analysis

Don’t Overthink the Summertime Rally

Trying to time the market is always a fool’s errand, in our view.

Is the stock market rally since mid-June the real deal? That question has been on many minds lately, particularly amid this week’s renewed negativity (Thursday’s positivity notwithstanding). In an effort to deliver the answer, many analysts are comparing how the past two and a half months stack up with past rebounds. That is an understandable impulse, but we think it stems from a flawed place. Inflection points are only ever clear in hindsight, and stressing over them can lead to myopic behavior.

That logic doesn’t stop the financial community from trying, though. Analysts are busy drawing myriad conclusions about the summertime rally. One found “bear market rallies rarely claw back more than 50pc of the previous loss. When they go beyond this point, it is usually a sign that the rally is the real deal.”[i] Some are less optimistic, arguing technical indicators don’t support more gains.[ii] Others have tallied up similar two-month jumps over the past 65 years to glean something about today’s upturn, though their takeaways are inconclusive.[iii]

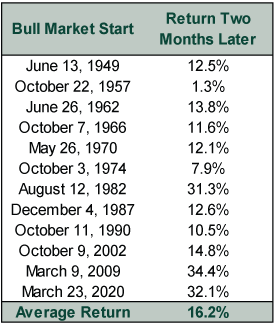

We agree looking to history is a useful practice. Past rebounds can provide a sense of what is probable and help investors set expectations. From June 16 to August 16, the S&P 500 rose 17.4% in price returns—in line with the postwar average two months into past new bull markets.[iv] (Exhibit 1)

Exhibit 1: Returns Two Months Into New S&P 500 Bull Markets

Source: Global Financial Data, as of 7/28/2022 and FactSet, as of 8/22/2022. S&P 500 Price Index, 5/29/1946 – 8/19/2022. Price returns used due to data availability.

But historical averages and models simply tell you what happened. That is just the starting place, and if you are going to employ historical analysis, we think it is vital to explore the why behind the what. Namely, what were the general conditions during those rallies? What did they have in common in terms of sentiment and economic drivers? We also think it is important to review false dawns, as some bear market rallies also top the 16% milestone. What did conditions look like then? What were people saying about the rally? Were there still strong signs the economy had much further to drop than expected?

Generally, recoveries start when dour sentiment dominates and a phenomenon Fisher Investments founder and Executive Chairman Ken Fisher calls the “Pessimism of Disbelief” is prevalent. When the Pessimism of Disbelief is widespread, investors see all news as negative. They ignore positive developments or couch them as potential sources of trouble. In this environment, economic fundamentals don’t have to be stellar. According to our research, many bull markets have begun amid weak growth or even contraction. But these tepid fundamentals are still better than what most anticipate—providing upside surprise and fuel for a recovery. When everyone projects disaster, and reality is only mildly bad, that can be enough to foment a genuine rebound.

Bear market rallies, by contrast, look like the inverse, as investor sentiment generally isn’t as dour. Moreover, during most bear markets, stocks usually decline gradually at first, lulling investors into complacency. In this environment, few notice deteriorating fundamentals. Instead of debating reasons to avoid stocks, investors treat any decline as an opportunity to buy—and a bear market rally can fool them into thinking the rebound is real and the bull market still has life.

Now, employing this method today won’t give you surefire answers. Yes, the Pessimism of Disbelief seems to be in place and economic data are mixed but generally better than projections for a deep recession—ingredients consistent with recovery. But we are also cognizant this bear market was mostly sentiment-driven, and feelings can flip on a dime. It is possible the recent rally fizzles out as ghost stories from this year gain renewed strength and weigh on investors’ moods—or if the recent weakening in economic data turns much deeper and broader than expected. It is also possible new fears arise, knocking sentiment—and stocks—further. However, the silver lining here is that you don’t need to nail inflection points. We understand the appeal of trying, but focusing on inflection points is myopic—and timing them is impossible, in our view, as stocks’ short-term moves are sentiment-driven, subject to wild, unpredictable swings.

Moreover, zeroing in on the super short term can tempt investors to try timing the market. That mindset encourages attempts to find the “perfect” moment to jump in—or to look for excuses to jump out. It can also cause investors to see daily market volatility as the start of a longer-term updraft or downturn—a mistake, in our view. Treating negative volatility as indicative of the future is a big risk since it may cause investors to miss out on a recovery.

Instead of trying to call a bottom, look to the foreseeable future. Identifying whether this is a temporary rally or not won’t make or break your portfolio, but not participating in bull markets can be a big setback since early gains compound throughout the generally rising period for stocks. We acknowledge more negative volatility is always possible, and the recovery won’t be smooth or easy. But nothing about long-term investing is.

[i] “Whether It’s a New Bull Market or a Bear Market Rally, There Is a Way to Make Money,” Tom Stevenson, The Telegraph, 8/18/2022.

[ii] “Wall St Week Ahead Summer Rebound in US Stocks Gains Fans Among Chart-Watching Investors,” Lewis Krauskopf, Reuters, 8/21/2022.

[iii] “How to Tell a New Bull From a Bear Market Fakeout: Toss a Coin,” Lu Wang, Bloomberg, 8/17/2022.

[iv] Source: FactSet, as of 8/22/2022. S&P 500 price returns, 6/16/2022 – 8/16/2022. Note, we use price returns throughout this article due to availability for historical data comparisons.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets — July 27 - July 312026-08-03

-

Expert Commentary 3 Things You Need to Know This Week | US Jobs, Trade Balance, Earnings Reports

2026-08-03

2026-08-03 -

Market Analysis Digging Into Last Week’s Fed ‘Credibility’ Concerns2026-08-03

-

Expert Commentary This Week in Review | Fed Meeting, US GDP, Eurozone GDP

2026-07-31

2026-07-31

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today