Personal Wealth Management / Market Analysis

Doom Loop Doesn’t Loom for Italian Banks

Italian banks aren’t the house of cards they are portrayed as.

As Italy’s new budget preoccupied investors in recent days, debt fears took a turn, with Italian banks entering the spotlight. Many believe Italy’s banks—holding Italian debt—are at risk. If the government’s finances get shaky, many fear, it could doom banks downstream. In our view, fears about Italy’s debt are clouding investors’ views of Italian banks and seem off the mark to us. As we showed here recently, Italy’s public finances are stronger than most give them credit for, and a “Quitaly” of Italy leaving the euro looks highly unlikely. Moreover, strip away debt fears and Italian bank fundamentals look fine—setting up bullish upside.

Italian bonds and banks aren’t inextricably linked. During Europe’s debt crisis, governments were on the hook for bailing out their banks, while banks held home-country sovereign bonds exposed to government credit risks—the dreaded “doom loop.” Some governments had to borrow heavily to bail out the banks, risking their own solvency—like Ireland. But spiraling banking and government failures depended on insolvent financial institutions and a depleted Treasury unable to borrow on the open market without sending debt costs to unsustainable levels. In Italy (and the rest of the eurozone outside maybe Greece), neither is the case today.

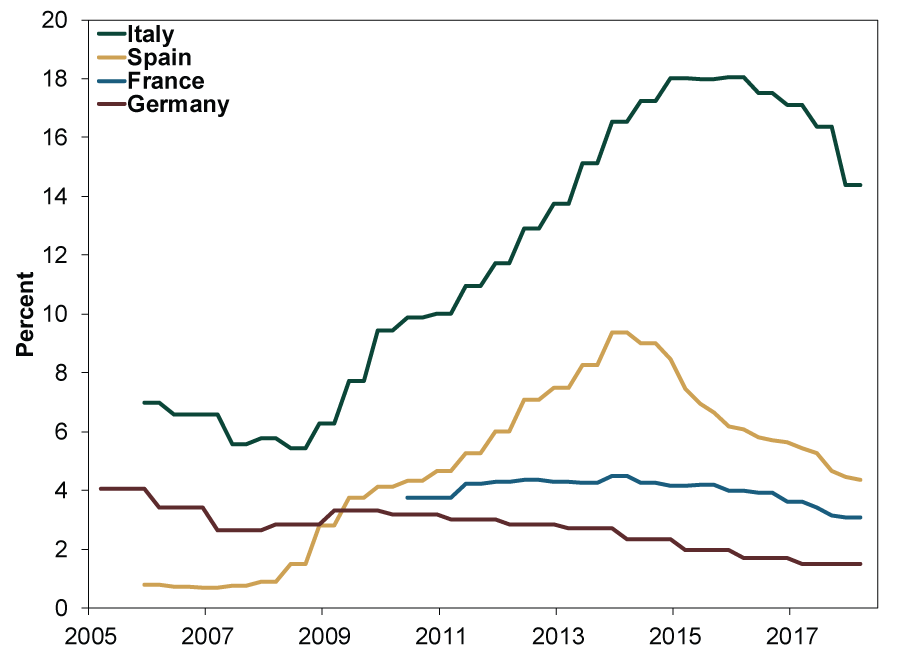

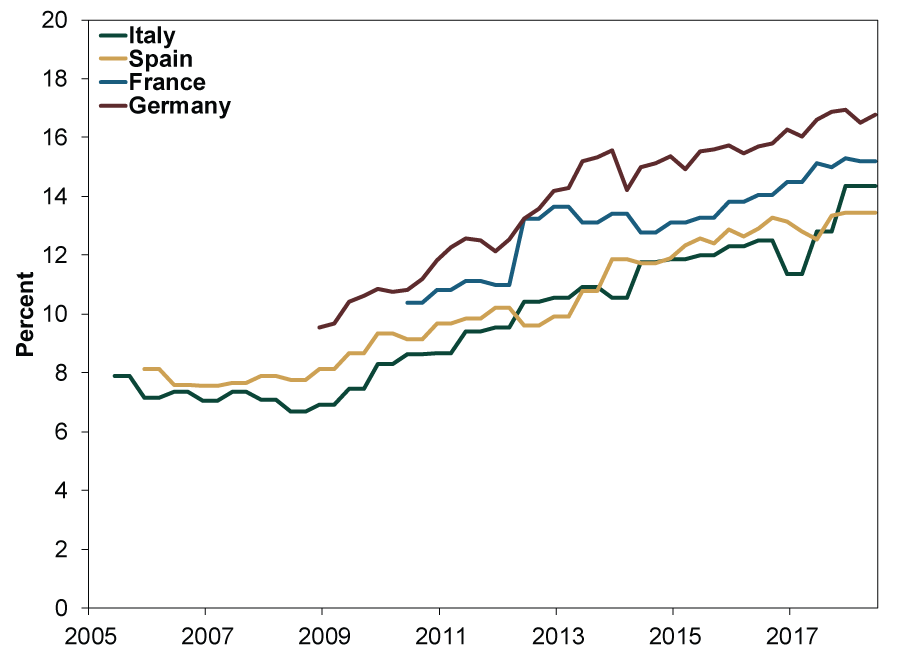

Italian banks don’t need bailouts anymore—they are cleaning up their books. As Exhibit 1 shows, while Italian banks’ non-performing loans (NPLs) are still above pre-crisis levels and higher than some other major eurozone members’, they have made big strides in reducing problem loans over the past couple years. Moreover, Italy’s biggest banks are in better shape than Exhibit 1 implies. Most bad assets are concentrated in smaller banks. Megabanks’ bad asset disposals are much further along. Italian banks’ capital ratios are also high and rising. (Exhibit 2) This means they can likely absorb substantial losses before being subject to ECB bail-in rules. There is more to do, but Italy’s banks are far along the road to recovery, and the biggest are on sound financial footing.

Exhibit 1: Italian NPLs High, but Falling

Source: FactSet, as of 10/5/2018. Non-performing loan ratio for Italian, Spanish, French and German banks, Q1 2005 – Q1 2018.

Exhibit 2: European Bank Capital High and Rising

Source: FactSet, as of 10/5/2018. Tier 1 capital ratio for Italian, Spanish, French and German banks, Q1 2005 – Q2 2018.

The big fear now is that Italian government debt constitutes about 11% of Italy’s bank assets.[i] This might be a problem if Italy’s Treasury was close to defaulting, but fiscally, Italy is coping far better than most mainstream coverage suggests. Interest payments are near generational lows, and yields are much lower than they were in recent history. Because most rates are fixed, rising rates impact Italy’s public finances only when new debt is issued. So it may be useful to compare recent bond issues that, in part, refinance this old debt. What you find is Italy’s long-term debt is getting cheaper.

In October 2003, Italy issued 15-year bonds at a 4.8% yield.[ii] 10-year notes auctioned in October 2008 cost 5.3%,[iii] while 5-year notes auctioned October 2013 yielded 2.9%.[iv] Italy sold 10- and 5-year debt September 28. Rates were 2.9% and 2.0%,[v] respectively, below the maturing bonds’ rates. October 12, Italy sold 15-year debt. The yield? 3.7%.[vi] Yes, they are rolling over some short-term debt at higher rates, but the average maturity of Italy’s debt stock is just under seven years,[vii] making elevated short-term debt costs less of a factor than some of the more hyperbolic commentary implies. Besides, yields on bonds up to 1 year in maturity are still sub-1%—very low.

Some people also fear Italy will leave the euro and eventually repay this debt in devalued lira, hurting creditors—including banks. But this remains highly unlikely. The populist parties, when forming Italy’s government, dropped all references to leaving the eurozone. Even if they called a referendum, a solid majority of Italians favor keeping the euro.[viii] But given Quitaly isn’t even part of their governing platform, this mostly seems like a sentiment freakout.

The reason to dump Italian banks would be if Italy’s (and the eurozone’s) economy was about to tank and their profits plummet, but nothing on the horizon suggests this is imminent. Italian GDP chugged along through Q2, and September’s services purchasing managers index (PMI) indicates expansion continued in Q3, while its forward-looking new orders suggest further growth ahead. The manufacturing PMI was 50[ix]—on the dividing line between expansion and contraction—but manufacturing is less than a fifth of Italy’s GDP; services is over 70%.[x]

Italy’s positively sloped yield curve—near-zero short-term interest rates and higher long-term rates—also implies ongoing growth. For banks, the yield curve is a good profitability proxy since banks borrow short, lend long and pocket the difference—a positive spread provides incentive to lend. The latest data from Banca d’Italia—Italy’s central bank—show private sector bank lending up 2.6% y/y in August, accelerating from July’s 2.5%.[xi] Household loans rose 2.7% y/y and business loans 1.2%.[xii] Loan growth has hovered in the mid-2% year-over-year range this year after steadily accelerating since 2013, but it remains at its highest rate in seven years. Banks may be reluctant to ramp up risk during a period of elevated political uncertainty, but as uncertainty falls, they should be able to resume taking risk.

In recent weeks, the yield curve has steepened, supporting wider net interest margins—and more lending. Gradual ECB monetary policy normalization—purchasing fewer bonds and potentially ending its negative short-term interest policy—may be helping, but regardless, a steeper curve bolsters profits. In other words, what people are freaking out about is actually an incremental positive. That says a lot about the divergence between sentiment and reality.

As abounding scare stories attest, sentiment toward Italian banks remains depressed—ghosts from sovereign debt crises past still linger. But the reality is far less shocking, and as fears fade—and Italy resolves its budget one way or another—investors should enjoy a positive surprise.

[i] “Bank Investors Fear Return of European Doom Loop,” Paul J. Davies, The Wall Street Journal, 5/29/2018.

[ii] Source: Dipartimento del Tesoro, as of 10/12/2018. 15-year Buoni del Tesoro Poliannuali (BTP) Auction Results’ Gross Yield, 10/14/2003.

[iii] Ibid. 10-year Buoni del Tesoro Poliannuali (BTP) Auction Results’ Gross Yield, 10/31/2008.

[iv] Ibid. 5-year Buoni del Tesoro Poliannuali (BTP) Auction Results’ Gross Yield, 10/31/2013.

[v] Ibid. 10-year and 5-year Buoni del Tesoro Poliannuali (BTP) Auction Results’ Gross Yields, 9/28/2018.

[vi] Ibid. 15-year Buoni del Tesoro Poliannuali (BTP) Auction Results’ Gross Yield, 10/12/2018.

[vii] Ibid, as of 5/23/2018. Weighted average maturity of government debt, March 2018.

[viii] “Polls Show Most Italians Want to Stay in Euro,” Giselda Vagnoni, Reuters, 5/30/2018.

[ix] Source: IHS Markit, as of 10/1/2018. Italy Manufacturing Purchasing Managers’ Index (PMI), September 2018.

[x] Source: OECD, as of 10/17/2018. Manufacturing and services, % of value added, 2017.

[xi] Source: Banca d’Italia, as of 10/10/2018.

[xii] Ibid.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Corporate Information How You Benefit from Fisher Investments' Transparent Fee Structure

2026-08-04

2026-08-04 -

Corporate Information How Fisher Investments' High-Touch Service Helps You2026-08-04

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets — July 27 - July 312026-08-03

-

Expert Commentary 3 Things You Need to Know This Week | US Jobs, Trade Balance, Earnings Reports

2026-08-03

2026-08-03

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today