Personal Wealth Management / Economics

Early March Data Echo Stocks' Downturn

Preliminary March PMIs start showing what stocks already saw.

For the past five weeks, stocks have been quickly pricing in the escalating likelihood of a global recession stemming from the world’s efforts to contain the spread of COVID-19. Now, courtesy of IHS Markit’s Flash March Purchasing Managers’ Indexes (PMIs) for major developed nations, we have the first economic data read on the situation. In a word, it is awful, making this a crucial time to remember stocks typically lead economic data, not the other way around.

PMIs are surveys, conducted monthly, of thousands of private businesses. Each business reports whether activity rose, fell or held steady versus the prior month in a handful of categories—including output, new business, new export business, employment and supplier delivery times. They also report on squishier indicators including expectations for future business and prices. IHS Markit then compiles all the responses into headline indicators for manufacturing, services and a composite of all businesses. Readings correspond to the percentage of businesses reporting expansion, with results over 50 generally signaling economic growth and under 50 implying contraction. These aren’t perfect indicators, as they don’t measure the magnitude of that growth or contraction. But they are timely, and the flash readings—early tallies containing about 85% of responses for the month—are especially so. Hence, we find them quite useful.

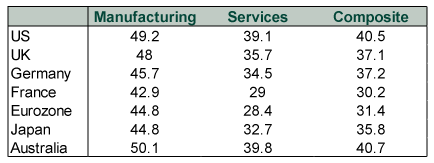

With that explainer out of the way, Exhibit 1 displays this month’s flash PMIs. Please take a deep breath before looking.

Exhibit 1: March Flash PMIs

Source: IHS Markit, as of 3/24/2020.

If we were to put these numbers into recent and historical context, there would be a lot of “all-time low” and “biggest single-month drop ever.” But at this juncture, we doubt an extended discussion of this would do anyone any favors.

Instead, we offer some caveats about those manufacturing numbers, which look surprisingly resilient. Unfortunately, they are actually worse than they appear, as they received a boost from skyrocketing supplier delivery times. This category counts as a positive because in a healthy expansion, supply chain backlogs indicate demand is robust and factories will have to kick it up a notch to keep up. In this case, however, they indicate the extent to which COVID-19 containment efforts have disrupted global supply chains. It is a false positive. Manufacturing output indexes, which eliminate that skew, were far worse across the board. In their accompanying commentary, IHS Markit also noted worldwide plunges in new orders, which is the main forward-looking component of a PMI. At the very least, that points to disappointing output in April even if containment efforts begin letting up.

One other caveat: Even if April’s figures jump back up to 50, it doesn’t necessarily imply a recovery. Rather, it would simply mean businesses held steady at a very low level of activity. Even in the best case scenario of quarantines outside the worst COVID-19 hot spots easing in a week, it may take time for businesses to pick up the pieces and find some semblance of normalcy. In other words, while we do think COVID-19 containment is causing a lot of pent-up demand, it probably won’t unleash all at once. If containment efforts last several more weeks—or even months—then these numbers could get a lot worse. Particularly since the most extreme containment measures didn’t take effect until later in March.

We say all of this not to be a downer, but to help you set realistic expectations, lest a few more rounds of bad data make you question your long-term investment strategy. Bull markets always follow bear markets, and recoveries follow recessions. Typically, the bull begins before the economic recovery, as stocks start pricing in the likelihood of a turnaround well before it becomes apparent in the data. In March 2009, people were talking about another Great Depression, much as they are now. Economic indicators were still hemorrhaging. So were corporate earnings. But stocks began recovering, because they didn’t need good news. All they needed was a reality that wasn’t quite as bad as the world feared.

What was true then should be true now, in our view. Yet there is no timing any bear market’s ultimate end. So this is a time to exercise the greatest, most difficult virtues in long-term investing: patience, endurance and faith that capital markets will work as they always have, ultimately overcoming even history’s greatest challenges.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary Why Ken Fisher Is Optimistic About European Stocks

2026-07-23

2026-07-23 -

Economics A Summertime Check-in on US Consumers2026-07-23

-

Market Analysis Why the SOX “Bear Market” Isn’t Foreboding2026-07-21

-

Politics Blunting Burnham?2026-07-21

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today