Personal Wealth Management / Economics

Earnings Demise Greatly Exaggerated

The earnings recession is over, but excluding Energy, there was never one to begin with.

Reports of earnings' downturn in 2015 - 2016 were an exaggeration, as Mark Twain might say. Now, with S&P 500 profits rebounding sharply, pundits seem to celebrate this as though it's a rebirth. But earnings' underlying trend overall rose at a fine clip pretty much the whole time. Investors' sunnier reaction to recent data says a lot more about sentiment than Corporate America's health.

After posting declines through 2015 and 2016's first half, S&P 500 earnings flipped positive and eked out an annual 0.7% gain last year.[i] During this period of weak profit growth pundits dubbed an "earnings recession," many investors wondered: Why be bullish? After all, for stocks, fundamentals are an important input into market direction, and you can't get much more fundamental than profits! Now, mere months later, profits are jumping and folks are relieved. Yet the reality is the recent rise isn't a renaissance. It's all about math and one sector-Energy's profit-growth math.

2015 and 2016's earnings decline was almost entirely due to Energy's sagging profits. After a roughly 20-month oil price plunge from $110 per barrel in June 2014 to $26 in January 2016, Energy sector profits imploded.[ii] Oil prices' -77% drop had a sufficiently powerful influence on Energy firms' profits-which are very oil-price sensitive-to flip headline profits negative. (Exhibit 1) Investors who correctly saw this was a single-sector phenomenon and rejected the "earnings recession" narrative were rewarded by stocks, which rose 14.7% while Energy skewed profits downward.[iii] (18.1% excluding Energy.[iv])

Now, earnings are jumping, boosted by oil and Energy's rebound, and beating expectations. Analysts are raising their earnings targets as a result. If nothing else, this should dispel lingering fears over US corporate profitability, boost sentiment and lead investors to bid stocks higher. However, cheering a supposed resurgence is as much an error of overrating Energy math as fearing the earlier decline. Energy's earnings, previously a drag, are now a tailwind, inflated by the low comparison base. During Q1 2017, oil traded around $50 per barrel, give or take. This is much higher than Q1 2016's average $34.55 Brent crude price. The 288% profit boost is the result.

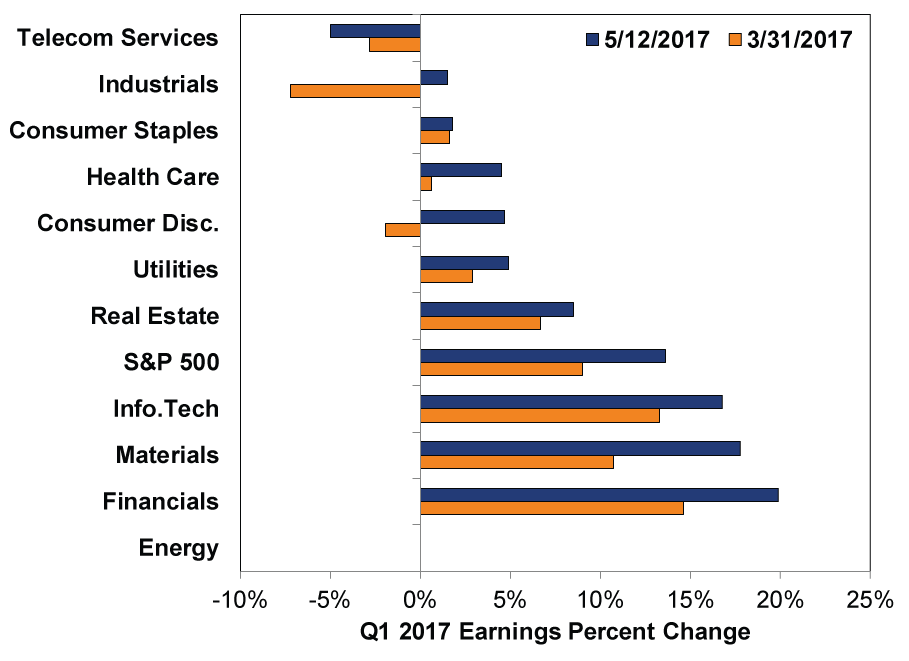

That upward boost is just as much a skew as the downside was earlier. But either way, earnings-with or without Energy-are growing and thumping expectations. Investors are only now appreciating this more as the "earnings recession" narrative has been proven false. In early April-before any releases-analysts estimated around 9% earnings growth. As results beat, they steadily ratcheted up forecasts. With 91% of S&P 500 companies now reporting, earnings rose 13.6% y/y, the fastest rate since Q3 2011 (if the pace holds) and up from Q4's 5.0%. (Exhibit 1) Excluding Energy, Q1 earnings rose 9.5%, well ahead of 5.4% expectations at April's start and accelerating from Q4's 5.2%. What's more, 75% of companies reporting beat analyst expectations. While beating is normal (managements often lowball estimates to "surprise" higher), we're well over the five-year 68% average. The 75% "beat rate" is the highest in 13 years. And the extent of earnings beats is above normal. In dollar amounts, actual earnings are coming in 6.0% higher than expected earnings, above the 4.1% average beat over the last five years. Exhibit 2 shows how Q1 earnings (blue bars) are topping analysts' estimates at Q1's end (orange bars).

Exhibit 1: Broad-based Q1 Earnings Growth

Source: FactSet Earnings Insight, as of 5/12/2017. Q1 2017 year-over-year earnings growth estimates for the S&P 500 and its sectors on 5/12/2017 and 3/31/2017. Because Q1 Energy earnings were negative last year, a year-over-year percentage calculation is mathematically impossible.

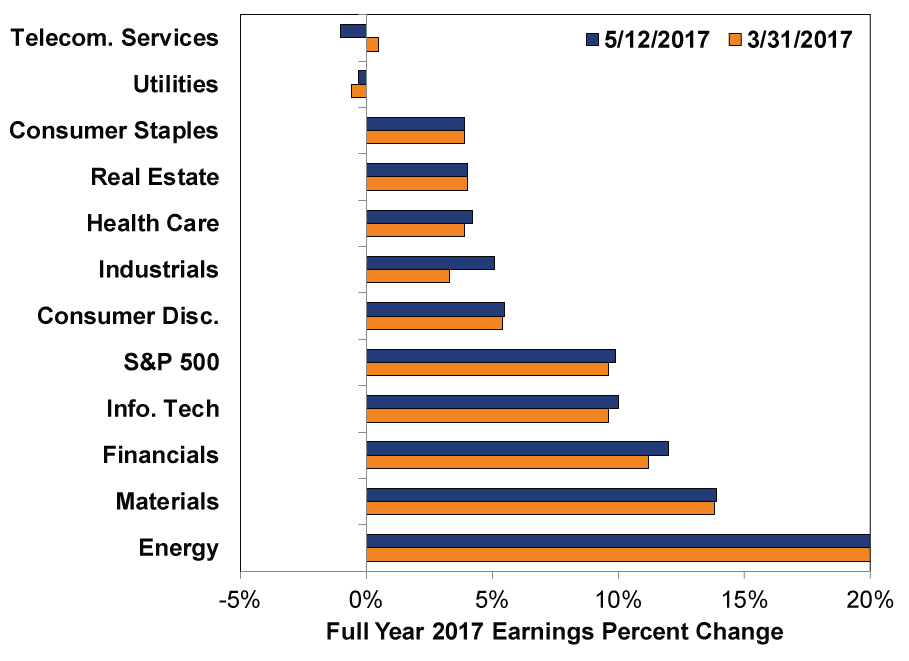

All that is rapidly moving into the rear view mirror as we're halfway through Q2, but the outlook continues improving for full-year 2017. When Q2 began, analysts expected earnings to grow almost 10% this year (7.1% ex Energy). Solid growth! And, as Exhibit 2 shows, they've actually slightly raised estimates as Q1 data have arrived. But even if earnings growth slows-possible, given Energy will move to a higher year-over-year base soon-bull markets don't need gangbusters earnings to kick off big returns. As bull markets proceed, investors tend to gain confidence. They extend their view of future profits further and further into the future. They become more willing to pay up for profits. Hence, price-to-earnings (P/E) ratios typically rise during a bull market's later stages.

Exhibit 2: Full Year Earnings Expectations Look Solid, Too

Source: FactSet, as of 5/12/2017. 2017 year-over-year earnings growth estimates for the S&P 500 and its sectors on 5/12/2017 and 3/31/2017. Energy cutoff at 20%; earnings growth estimated at 287.5% on 5/12/2017 and 297.2% on 3/31/2017.

Ultimately, to those who have correctly seen Energy's influence, the latest skew isn't a surprise. It's the reversal of the same factor that erroneously made folks downcast a year or so ago. But outside this skewed sector, profits have been fine throughout the last couple years-and likely continue to be moving forward.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary This Week in Review | Global PMIs, SpaceX, RMD Planning

2026-07-10

2026-07-10 -

Market Analysis Trim Your Angst on Economic Measurement Tweaks2026-07-09

-

Politics Long-Term Forecasts and Court Verdicts: The Latest in British and French Politics2026-07-09

-

Corporate Information How You Benefit from Fisher Investments' Transparent Fee Structure

2026-07-08

2026-07-08

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today