Personal Wealth Management / Economics

Earnings Slip on Oil, and Other Obvious Puns

Strip out the Energy sector, and S&P 500 earnings look just fine.

Earnings season is winding down, and with four firms left to go, the S&P 500 is on track for its 19th straight quarter of earnings growth. But headlines aren't celebrating-they're eulogizing. Profits are expected to drop the next two quarters, and pundits warn "profit recessions" have preceded the last two economic recessions (and accompanied bear markets). Some point to broader US corporate profits-down three straight quarters through Q3-as another indicator of trouble ahead. However, dig into the numbers a bit, and it's clear most companies' profits aren't plunging, and stock prices are not becoming wildly detached from earnings. Everything is just skewed by falling oil prices.

Yes, aggregate S&P 500 earnings and revenue growth both slowed in Q4. Revenues eased from 4% y/y in Q3 to 2.1%, and earnings drifted from 8% y/y in Q3 to 3.7%. Both are expected to fall in Q1 and Q2, and analysts expect total 2015 revenues to be in the red. That all sounds very dreary, particularly with stocks clocking new highs and price-to-earnings ratios above-average. However, aggregates and averages have a problem: They obscure things. Sometimes they gloss over problems. Other times they make problems look bigger than they are. This time, they are spreading the sea of red ink in the Energy sector to the rest of the market. Strip Energy from all these earnings calculations, and it's clear the rest of the market is in fine shape. Without energy, earnings and revenues grew faster in Q4-and are projected to grow looking ahead.

Exhibit 1: S&P 500 Earnings and Revenue Growth

Source: FactSet and Math, as of 3/9/2015. Q4 figures include 496 of 500 S&P 500 companies. All growth figures are year-over-year.

It takes huge negative surprises to kill bull markets prematurely, and falling Energy earnings and revenues are neither huge nor surprising. Both started falling several quarters ago, even before oil prices' 2014 swan dive-oil prices weren't tanking before June, but they were still under pressure from booming output at US shale fields. They are also not huge. S&P 500 Energy revenues are projected to fall by about $500 billion this year, and the sector's earnings are projected to drop by $64 billion-big numbers, but not big enough to derail a bull market. That usually takes a few trillion worth of negatives. Energy's woes lack scale and breadth. For most other sectors, low energy prices are good! Consumer firms benefit from people having more discretionary cash. Industrials and service firms benefit from lower operating costs, which boost margins. Lower energy prices create enough growth elsewhere to offset the bloodbath in Energy. This is simply a winners and losers game.

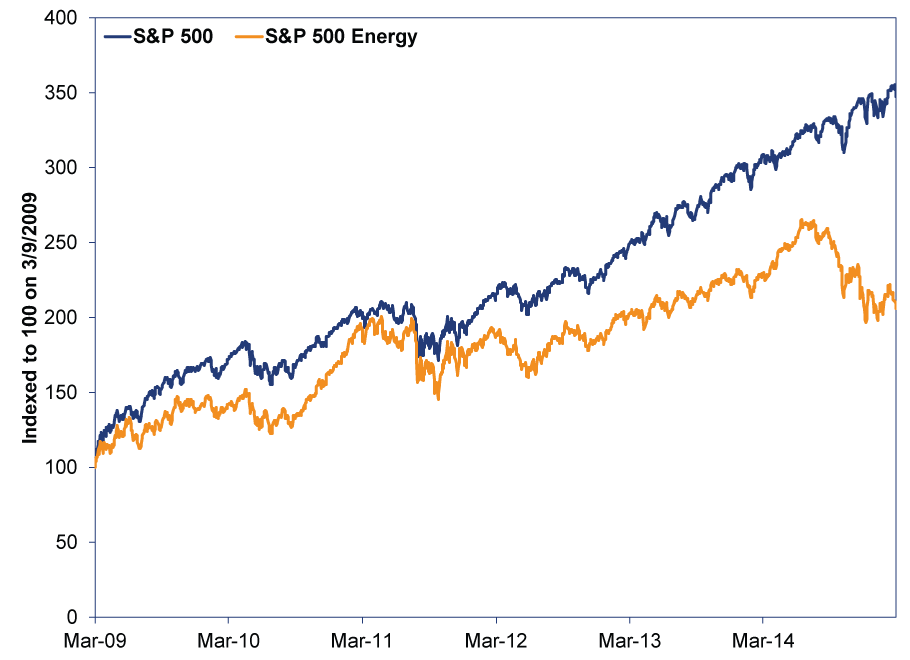

Markets know all of this and have been pricing it in. Broad markets aren't down, but Energy stocks sure are. They've underperformed the S&P 500 since mid-2011 and have taken a beating since June. Stocks are very well aware of how oil prices impact Corporate America's profitability, and they are behaving accordingly. Energy stocks are down. Most other sectors are up.[i] Weak oil prices are a reason, in our view, to underweight Energy stocks and overweight sectors poised to benefit. Not to get out of stocks.

Exhibit 2: S&P 500 Vs. Energy

Source: FactSet, as of 3/9/2015. S&P 500 and S&P 500 Energy Sector Total Return Indexes, 3/9/2009 - 3/6/2015.

As for broader corporate profits, the US Commerce Department doesn't give a timely industry breakdown of after-tax profits, so we can't perform the same analysis-but we have no reason to believe the story there is wildly different. We also know, from history, that falling total profits-like falling S&P 500 earnings-are normal in maturing bull markets and expansions. It often doesn't mean the private sector is weakening. Usually, the year-over-year comparisons just get more difficult to beat. Treating falling profits as a leading indicator could lead to some very bad market timing. Like selling in March 1998, two years before the bull ended. Or December 1985, over a year and a half before stocks peaked. Or sitting out the entirety of the late-1960s bull market. And the first half of the early-1950s bull. It's important to watch corporate profits-and monitor whether investors are overlooking bad news-but they are not a market-timing tool.

As far as we're concerned, today's earnings brouhaha is just another instance of sentiment broadly missing the forest for the trees-a sign we aren't at that euphoric bull market peak yet. When pundits pooh-pooh actually poor earnings, that will be a sign investors are out over their skis. We aren't there yet.

Stock Market Outlook

Like what you read? Interested in market analysis for your portfolio? Why not download our in-depth analysis of current investing conditions and our forecast for the period ahead. Our latest report looks at key stock market drivers including market, political, and economic factors. Click Here for More!

[i] Materials are mostly losing, because most commodity prices-particularly metals-are way down. Materials firms, like Energy, are price-sensitive, not volume-sensitive.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis The New Tariffs in Town Are Still Old News2026-07-24

-

Expert Commentary This Week in Review | Market Volatility, Tariffs, SpaceX

2026-07-24

2026-07-24 -

Economics A Summertime Check-in on US Consumers2026-07-23

-

Expert Commentary Why Ken Fisher Is Optimistic About European Stocks

2026-07-23

2026-07-23

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today