Personal Wealth Management / Economics

Earnings—Still High, Still Rising

Earnings are still at all-time highs and rising, with less economically sensitive sectors leading the charge.

Earnings season is winding down, and with 384 of S&P 500 companies reporting through August 2, US stocks are on pace for share-weighted earnings growth of 4.3%—the 14th straight quarter of growth.i On their own, all-time-high-and-rising earnings are bullish for stocks—but even more bullish, most folks don’t see the strength underlying the headline results.

Instead, they see a figure skewed by Financials earnings, which grew 28.5% y/y thanks to one-off losses some firms took in Q2 2012, distorting the yearly comps. To many, excluding Financials better reflects corporate health, and since earnings ex-Financials are up only 0.6%, corporate America must be losing steam.

In our view though, this hardly means the expansion is petering out. With or without Financials, earnings are behaving normally for a maturing bull market. For one, earnings growth rates regularly slow as year-over-year comparisons become more difficult to beat. Cyclical factors are also at work. Early in an expansion, earnings grow quickly thanks to recessionary cost-cutting—even modest sales growth means big margins. Later on, firms reach the limits of their efficiency gains, and they have to raise costs in order to boost output and keep up with demand. As costs and revenues play leap frog, fat margins are tough to maintain.

To see how firms really did in Q2—and to see which broad market trends are in force—start by breaking down revenue growth by sector (Exhibit 1).

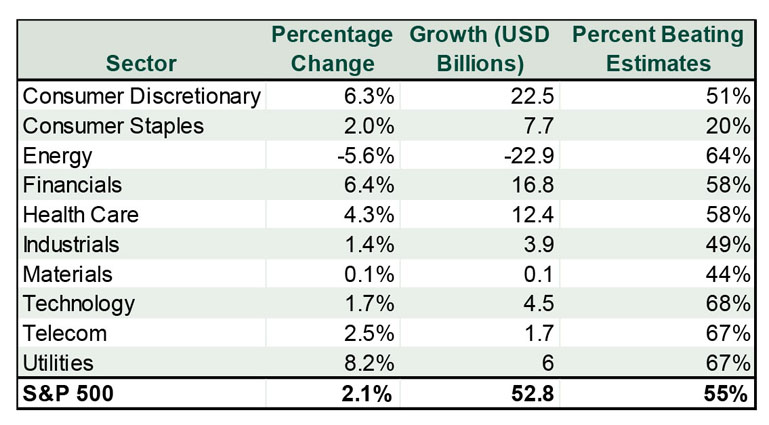

Exhibit 1: S&P 500 Q2 2013 Y/Y Revenue Growth By Sector

Source: Thomson Reuters, as of 8/2/2013.

Financials are far less of an outlier here. More eye-catching, in our view, is continued weakness in Energy, Industrials and Materials—three economically sensitive, commodity-driven sectors. Together, their revenues fell -2.4%. This is typical later in an expansion—and with commodity prices struggling lately, it’s even less surprising. Also unsurprising, less cyclical sectors with more diverse revenue streams are holding up fine. Excluding Energy, Industrials and Materials, revenues are up 4.2%. Not gangbusters, but not shabby nearly four and a half years into a bull.

The sector breakdown of earnings growth tells a similar story (Exhibit 2).

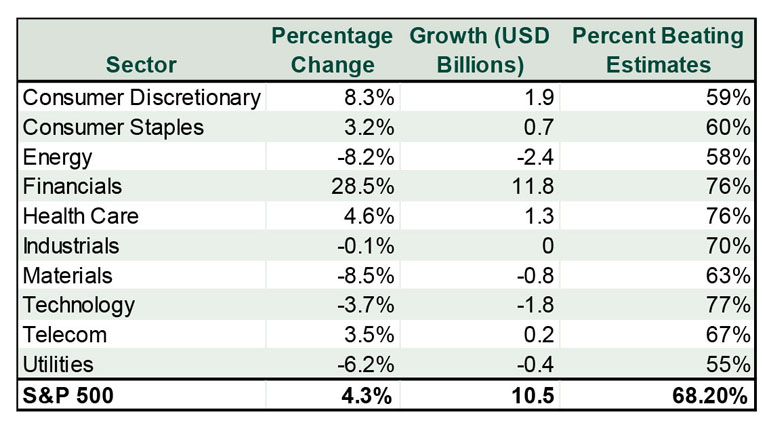

Exhibit 2: S&P 500 Q2 Y/Y Earnings Growth by Sector

Source: Thomson Reuters, as of 8/2/2013.

Together, share-weighted earnings for Energy, Materials and Industrials are down -6.2%—just as we’d expect given their high fixed costs and falling sales. Toss these sectors, and aggregate share-weighted earnings grew 7.8%. Toss Financials, too, and it’s a weaker 1.5%, but still growth and better than those stripping out Financials only would have you believe.

Valuations are similarly misinterpreted. P/Es have risen lately, leading some to say stocks are rising too high too fast. However, the S&P 500’s 12-month forward P/E of 14.4% is still below the long-term average—not necessarily predictive, but telling about the gap between perception and reality (Exhibit 3).

Exhibit 3: S&P 500 12-Month Forward P/E

Source: Thomson Reuters, as of 8/2/2013.

Fact is, stocks have lagged corporate profits for most of the bull, and they’re only just starting to catch up. S&P 500 earnings hit all-time highs in Q2 2011, but the index itself only got there in March. And lest you think this signals an inflection point, we still haven’t seen the multiple expansion typical of bull markets’ latter stages. Maybe it’s starting to happen now—and if that’s the case, multiples can likely expand for some time as investors place ever-higher premiums on companies with the most stable earnings growth. And with fundamentals broadly better than most appreciate, this bull can keep marching higher.

i Source: “This Week in Earnings,” Thomson Reuters, 8/2/2013.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Corporate Information How You Benefit from Fisher Investments' Transparent Fee Structure

2026-08-04

2026-08-04 -

Corporate Information How Fisher Investments' High-Touch Service Helps You2026-08-04

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets — July 27 - July 312026-08-03

-

Expert Commentary 3 Things You Need to Know This Week | US Jobs, Trade Balance, Earnings Reports

2026-08-03

2026-08-03

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today