Personal Wealth Management / Market Analysis

Easing’s Quantitative Analytics

A quick analysis of QE’s impact on the economy throws into question the quantity of its benefits.

Fed-head Ben Bernanke has started walking back from his June suggestion quantitative easing (QE) might end soon, and investors seem pleased with the U-turn. In our view though, that cheer is rather misplaced. Data show current Fed policy is contractionary for the economy, and in our view, its eventual end should be bullish for stocks.

QE aims to stimulate economic activity—and, per the Fed’s mandate, employment—by increasing the amount of money in the economy and reducing long-term interest rates. With money abundant and cheap, the theory goes, businesses can get easier financing for growth-oriented investment and, eventually, hiring. But in practice, monetary policy doesn’t always have the economic impact expected in theory, and QE is no different.

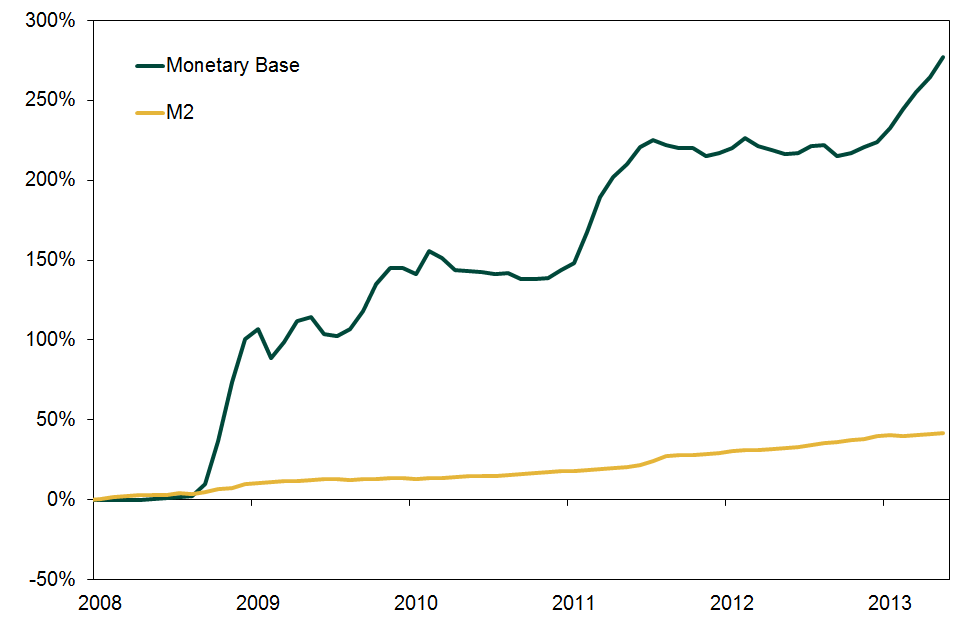

Long rates have indeed fallen, and the monetary base (M0) is up. Yet increasing the monetary base (M0) alone won’t increase economic activity. The money has to circulate—money sitting on the sidelines does nothing. If you look a little closer, you’ll see the amount of money in circulation (M2) remains subdued even as the monetary base has nearly tripled. (Exhibit 1)

Exhibit 1: Cumulative Monetary Base Versus Money Supply Growth

Source: Thomson Reuters, US Federal Reserve as of 7/2/2013. Money Supply and Monetary Base from 12/15/2007-5/15/2013.

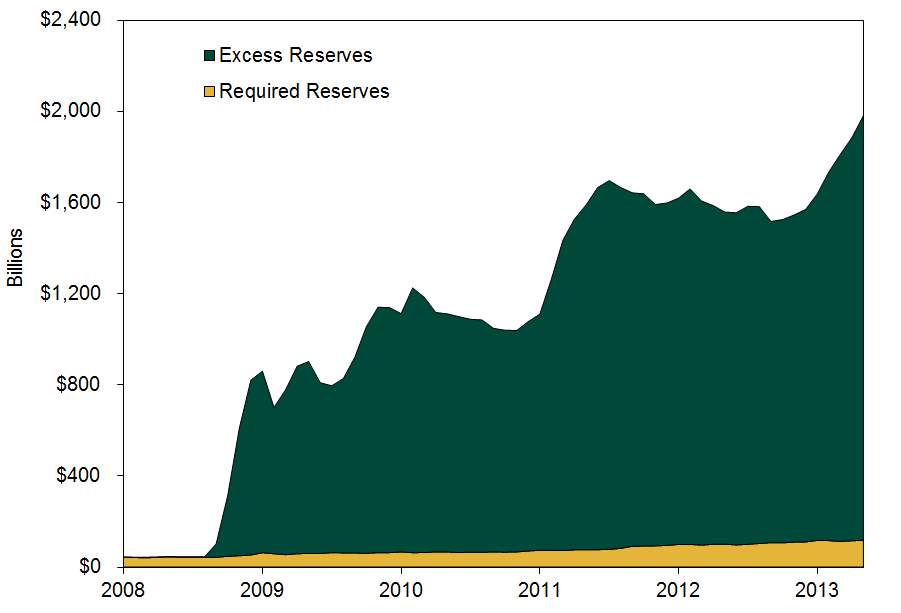

This discrepancy is a direct result of QE. Ultimately, QE discourages higher M2 by flattening the yield curve, which disincentivizes bank lending. Banks borrow short—through customer deposits and wholesale funding markets—and lend long, and their potential operating profit is the spread between long and short rates. But as the Fed continues purchasing long-term assets (Treasurys and agency mortgage-backed securities), it pushes long-term interest rates lower, reducing banks’ potential margins on the next loan made. Meanwhile, regulatory capital requirements are set to rise, requiring banks to hold more reserves against loans made today, adding risk to every lending decision. For many banks, the risk/return tradeoff of all but the highest-quality loans isn’t worth it. As a result, they largely haven’t tapped excess reserves created through QE—they’ve kept them at the Fed for no risk and a little return. (Exhibit 2)

Exhibit 2: Excess Reserves Versus Required Reserves

Source: Thomson Reuters, US Federal Reserve as of 7/2/2013 Excess Reserves of Depository Institutions, Required Reserves of Depository Institutions from 1/15/2007-5/15/2013.

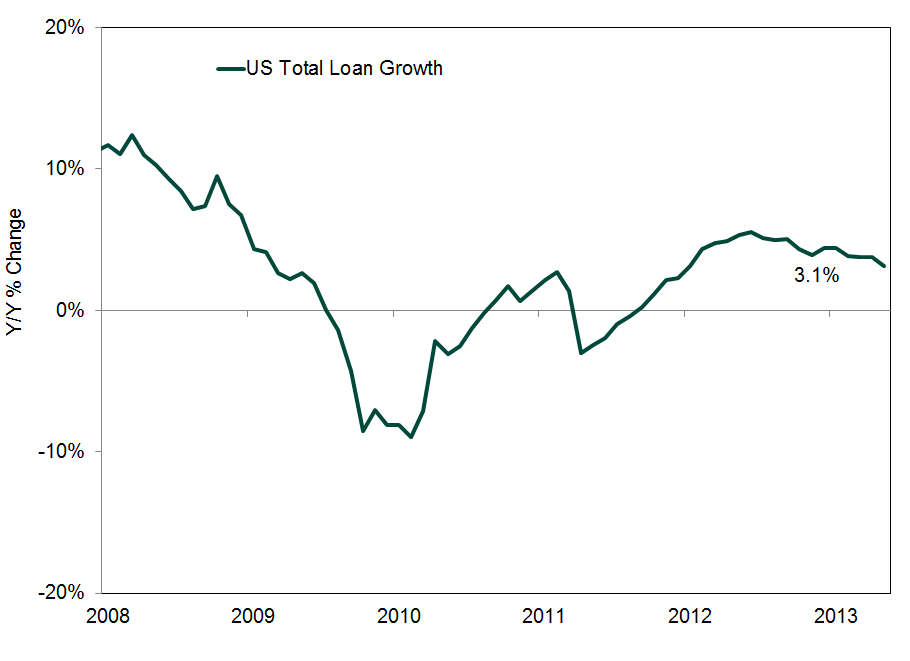

Loan growth, as a result, has been lackluster (Exhibit 3). Large, well-capitalized businesses can access credit, but many small and mid-sized businesses have a tougher time, robbing the economy of a key source of growth. That the US economy is still growing anyway is a testament to the US economy’s fundamental strength—we’re growing despite QE, not because of it.

Exhibit 3: US Loan Growth

Source: Thomson Reuters, US Federal Reserve as of 7/2/2013. Total Loan Growth, Industrials and Commercials Loan Growth from 1/15/2006-5/15/2013.

So, in our view, QE’s end would be an economic positive. Perversely, ending it would likely help the Fed hit its targets of 6.5% unemployment or 2.5% inflation sooner, as the velocity of money and overall growth would likely accelerate.

QE’s end is likely good for stocks, too. Investors see this nearly perfectly backward. Fear of a false factor is almost always bullish—and the bigger the misperception, the bigger its potential positive surprise power. Plus, QE hasn’t been a big driver of returns during this bull, despite what some headlines say. It might have provided a small sentiment lift, but the notion of “hot money” alone propping up stocks is flawed. This bull has ample fundamental support. Some say low yields have driven investors from stocks to bonds, and rising yields will drive them back out, but this overlooks why investors would own stocks or bonds in the first place. Folks generally own stocks for long-term growth and bonds to mitigate short-term volatility or help provide cash flows. A bond investor looking for a higher yield is thus more likely to move into high-grade corporate bonds and other similar assets—and considering how far corporate yields have fallen, this is likely what has happened since QE began. Similarly, rising interest rates don’t give investors fundamental reasons to leave stocks. Stocks can do (and have done) just fine during periods of rising rates. As long as companies are profitable, investors have every reason to continue bidding share prices up.

Still, we may see further volatility as investors chew over Fed plans and QE’s end. But after QE ends and investors see reality is much better than they anticipated, stocks should ultimately get a nice lift overall.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets — July 27 - July 312026-08-03

-

Market Analysis Digging Into Last Week’s Fed ‘Credibility’ Concerns2026-08-03

-

Expert Commentary 3 Things You Need to Know This Week | US Jobs, Trade Balance, Earnings Reports

2026-08-03

2026-08-03 -

Expert Commentary This Week in Review | Fed Meeting, US GDP, Eurozone GDP

2026-07-31

2026-07-31

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today