Personal Wealth Management / Market Analysis

Elastic Health Care Demand?

In the past few years, it seems many patients deferred procedures as a result of economic hardship. Improving macroeconomic conditions should drive patient utilization rates higher.

Few folks willingly cease cancer treatment when macroeconomic conditions deteriorate. Nor is it likely many increase medication intake during a robust economic expansion. This relatively inelastic demand keeps Pharmaceuticals firms’ sales and earnings relatively stable—and typically contributes to outperformance during periods of economic uncertainty. For this reason, Health Care is often thought of as a defensive sector. But this common perception isn’t a universal truism.

Not all Health Care industries are as defensive as Pharmaceuticals—particularly true for many Health Care Equipment firms. For example, orthopedics firms manufacture devices associated with the skeletal system, such as joint replacements, hand reconstruction and spinal fusion products. And demand for these products is more elastic than pharmaceuticals. How so?

Imagine a patient—a 54-year old female and primary breadwinner for her household. Partly due to daily joint stress and partly due to an old ski injury, she has chronic knee pain and deteriorating mobility. Surely a major discomfort—but thankfully, not a life-threatening condition.

She is a candidate for total knee replacement—which is covered under her employer-sponsored medical insurance. She will undergo surgery—the only question is when. Most total knee replacement patients don’t resume normal daily activity for several weeks following surgery. This lengthy recuperation and the financial implications can weigh on the surgery decision. As such, patients often delay medically necessary yet deferrable procedures based on their current financial condition or even their perception of economic conditions—waiting until their outlooks improve.

That’s just one example—numerous other factors drive procedure deferral. A growing prevalence of high-deductible insurance plans places more of the financial burden on the individual, while a lack of insurance coverage from job loss shifts costs entirely to the patient.

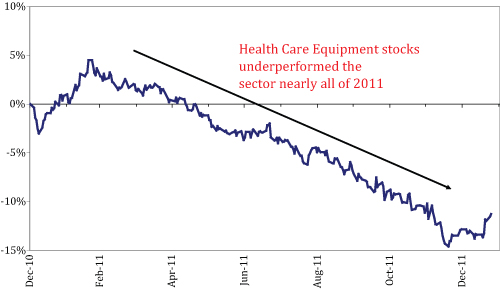

Patient utilization (procedure demand) rates were anemic over the last few years, likely primarily due to 2007-2009’s recession and its aftermath. Naturally, lower utilization rates caused lower sales and earnings growth for many Equipment firms, contributing to industry underperformance versus the broader Health Care sector (Exhibit 1).

Exhibit 1: Relative Performance of Health Care Equipment Industry Versus Health Care Sector

Source: Thomson Reuters, S&P 1500 Health Care Equipment Index versus S&P 1500 Health Care Index, 12/31/2010-12/31/2011.

It seems unlikely to me the recession suddenly cured chronic joint issues like our hypothetical patient’s. Instead, it’s likely there’s a backlog of delayed procedures. Ongoing US economic growth should provide a much-needed assist.

GDP grew at accelerating rates in Q2, Q3 and Q4 2011—and it seems quite likely growth continues ahead. Employment has been improving in recent months and disposable incomes overall rising. Economic and wage growth seem likely to goad an uptick in utilization rates as pent up demand is released—benefiting Health Care Equipment firms and helping Health Care Equipment valuations expand from currently low levels. Not all Health Care firms are created equal—Equipment firms seem poised to benefit in 2012 along with other economically sensitive categories.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Politics Blunting Burnham?2026-07-21

-

Expert Commentary 3 Things You Need to Know This Week | Q2 Earnings, ECB Meeting, Trump Accounts

2026-07-20

2026-07-20 -

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—July 13 - July 172026-07-20

-

Market Analysis Pumping Up the Yen?2026-07-17

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today