Personal Wealth Management / Economics

Energy Inflation, Gas Taxes and Markets’ View

Seeing energy costs’ impacts from a market perspective.

Editors’ note: While inflation is a politically charged subject, our commentary addresses its economic, market and personal finance impact only.

Driven by gas, the US consumer price index (CPI) accelerated to 7.9% y/y in February.[i] Moreover, that read preceded March’s energy spike tied to Russia’s escalating war in Ukraine, which temporarily sent oil as high as $139 per barrel—and US national average gas prices to a record-high $4.33 per gallon.[ii] Many Americans, especially those who drive a lot for work and other responsibilities, may be feeling a pinch. It is also fueling fears of further inflation ahead, prompting some to call for action—like temporarily waiving gas taxes. But for investors, we think it is important not to overrate the effect—or staying power—of these higher prices.

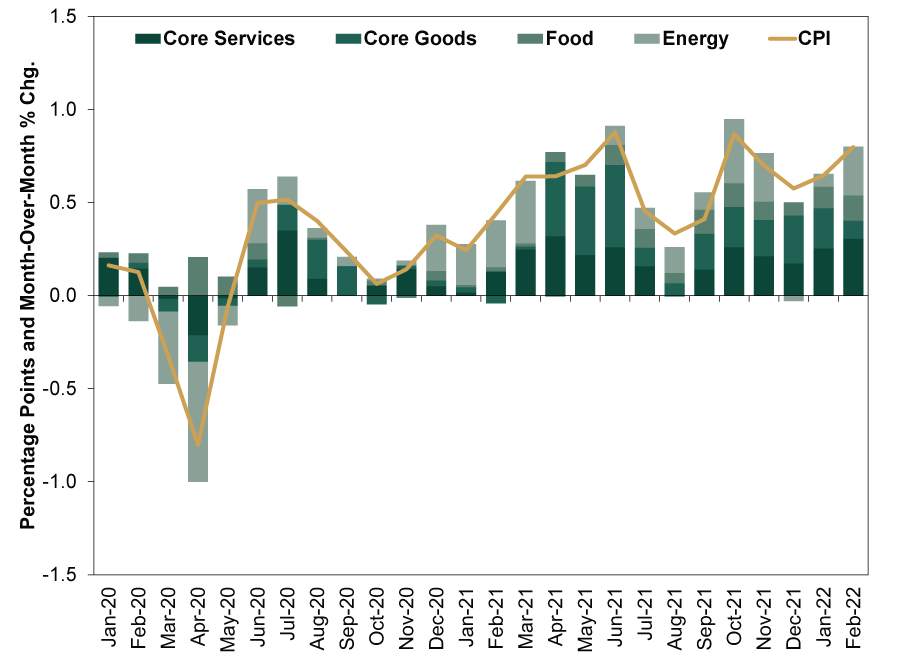

Month-over-month, February’s CPI rose 0.8%, with gas’s 6.6% monthly gain responsible for a whopping one-third of the headline figure.[iii] That is a huge contribution, considering gasoline’s share of the CPI basket is just 3.7%.[iv] With gas now up 18.2% in March, expect a much larger contribution—and further bump in CPI—if pump prices stay elevated.[v] Exhibit 1 shows how much energy has contributed to monthly inflation.

Exhibit 1: Contributions to Month-Over-Month CPI by Major Category

Source: US Bureau of Labor Statistics (BLS), as of 3/10/2022. Seasonally adjusted categories’ effect on CPI, January 2020 – February 2022. Note: The sum of the categories’ percentage point contributions may not always match headline CPI growth rates exactly due to the BLS’s statistical margins of error.

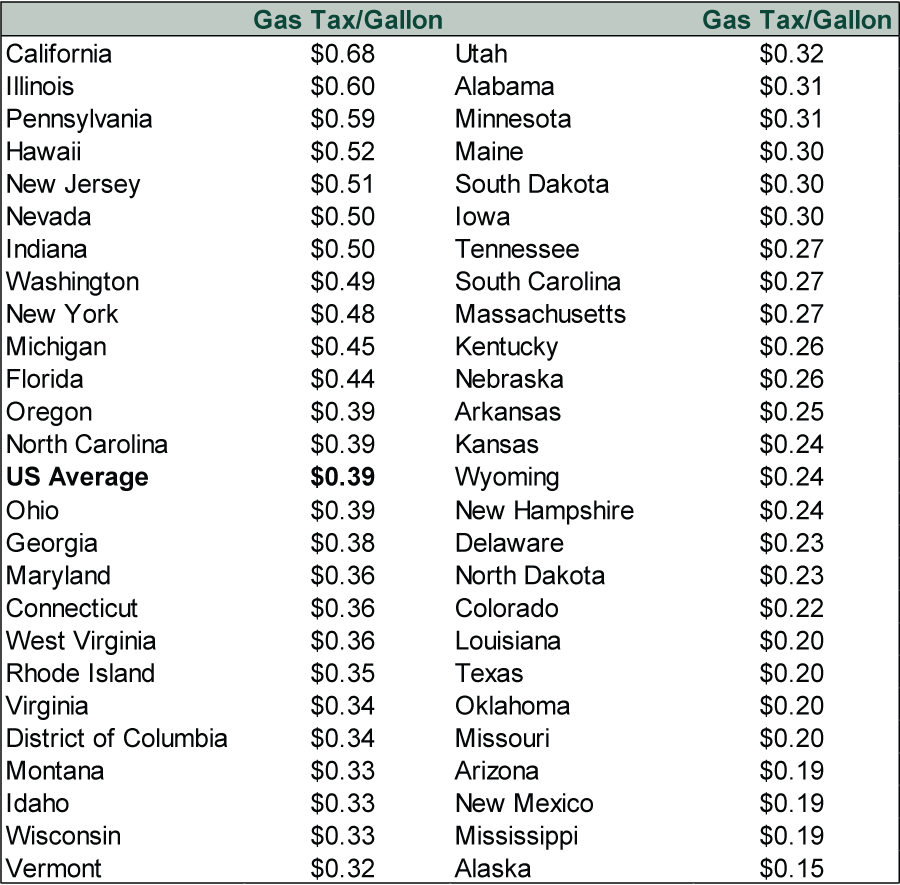

There is discussion underway to suspend the federal gas tax, but we doubt it will have a huge impact. While the federal gas tax is 18¢ per gallon, states’ levies are bigger, averaging 39¢. (Exhibit 2) Will all 50 states act in concert with the feds? Moreover, gasoline’s CPI weight is, again, just 3.7%.[vi] We don’t dismiss the potential help for those with fuel costs that are big parts of their budgets, but any gas tax waiver(s) will likely have only a tiny impact on overall inflation.

Exhibit 2: Gas Taxes by State

Source: American Petroleum Institute, as of 1/1/2022.

For the broad economy and markets, what effects—if any—are energy price spikes likely to have? They likely add to production costs for manufactured goods and their distribution—on top of all the supply chain snags over the last year. But energy aside, those snags have started to ease. Shipping bottlenecks and supplier delivery times have fallen noticeably in recent months. San Pedro Bay container ship backlogs for LA area ports—the nation’s busiest—have been cut in half to 50 vessels waiting to unload from over 100 in January.[vii] More generally, as IHS Markit noted about US manufacturing supply chains, “Delivery delays were the least severe since last May.”[viii] Now, perhaps flight re-routing and shipping issues stemming from the war in Ukraine will impact shipping anew, but given Russia’s small global economic footprint, we doubt they would be very big.

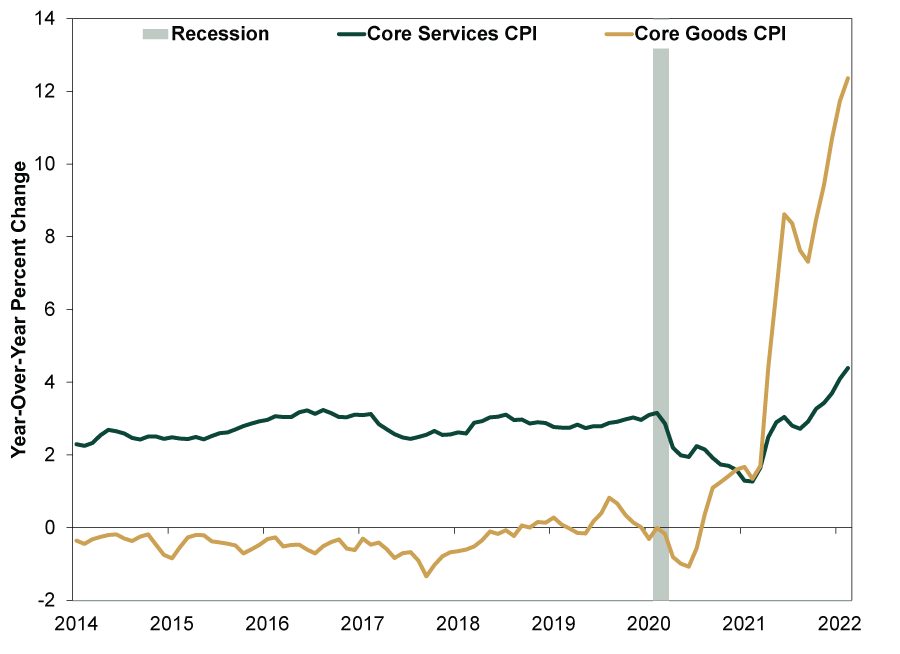

Those prior disruptions—now fading (if in fits and starts)—are primarily why inflation has surged. There was a big COVID-related shift to goods spending from services. Discretionary in-person services collapsed in favor of deliverable things—e.g., at-home gym equipment replaced gym memberships. Meanwhile, as 2020 lockdowns shuttered a lot of production globally, reopening-related demand surged. But restarting factories and supply lines—coordinating across borders facing different restrictions—has proved more difficult than turning them off. Through 2021, this caused mainly goods prices to soar, whereas pre-pandemic they were mostly deflationary. (Exhibit 3) Add energy disruptions starting last fall to today, and you have headline CPI hitting four-decade highs.

Exhibit 3: Inflation Is Mainly Goods-Driven

Source: Federal Reserve Bank of St. Louis, as of 3/10/2022. Services CPI less energy services and goods CPI less food and energy, January 2014 – January 2022.

But we think forward-looking markets care more about inflation’s path over the next 3 – 30 months. As COVID wanes, lingering restrictions end and supply-chain disruptions fade (including from war), price pressures should subside sooner rather than later. We expect consumption patterns to veer back toward pre-pandemic behavior, with more services-based economic activity. That may not lead to outright price declines in goods, but in our view, they are likely to level off along with inflation generally.

This may already be occurring. Although we hesitate to read too much into short-term moves, spot oil prices are back under $100 as we write.[ix] Of course, they may spike again, and sentiment-driven moves are unpredictable—especially given geopolitical tensions among oil-producing (and consuming) powerhouses and China’s latest lockdowns, which many see hampering oil demand. Yet oil futures also hint at cheaper oil several months from today’s levels, implying traders don’t see the spike persisting.[x] Futures prices a year out are trading at $83.[xi] Although they don’t forecast oil prices,[xii] they do reflect a market outlook where tight supply-demand conditions now aren’t expected to last.

This is why we think the 10-year Treasury yield, highly sensitive to inflation and inflation expectations, isn’t signaling much longer-term concern. Yes, it has risen in recent months, but at just 2.1% now, it remains below nearly all pre-pandemic levels.[xiii]

[i] Source: BLS, as of 3/10/2022. CPI, February 2022.

[ii] “Gas Prices Are Probably Still Headed Much Higher,” Brian Sozzi, Yahoo!, 3/14/2022.

[iii] Source: BLS, as of 3/10/2022. CPI and gasoline, February 2022.

[iv] Ibid. Gasoline’s relative importance in CPI, January 2022.

[v] Source: FactSet, as of 3/16/2022. Reformulated blendstock for oxygenate blending gasoline price per gallon, 2/28/2022 – 3/15/2022.

[vi] See note iv.

[vii] “Port of Long Beach Records Busiest February Ever,” Brandon Richardson, Long Beach Business Journal, 3/11/2022.

[viii] “Output Growth Picks up Amid Stronger Demand and Easing Supply Disruption,” Chris Williamson, IHS Markit, 3/1/2022.

[ix] Source: FactSet, as of 3/16/2022. WTI crude oil price per barrel, 3/15/2022.

[x] “Hedge Funds Slash Oil Positions Amid Extreme Volatility,” John Kemp, Reuters, 3/14/2022.

[xi] Source: FactSet, as of 3/16/2022. WTI crude oil price per barrel, March 2023 futures contract, 3/15/2022.

[xii] As futures prices also reflect storage or “carrying” costs.

[xiii] Source: FactSet, as of 3/16/2022. 10-year Treasury yield, 3/15/2022.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis The New Tariffs in Town Are Still Old News2026-07-24

-

Expert Commentary This Week in Review | Market Volatility, Tariffs, SpaceX

2026-07-24

2026-07-24 -

Economics A Summertime Check-in on US Consumers2026-07-23

-

Expert Commentary Why Ken Fisher Is Optimistic About European Stocks

2026-07-23

2026-07-23

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today