Personal Wealth Management / Economics

Fast Inflation Still Looks Fleeting to Us

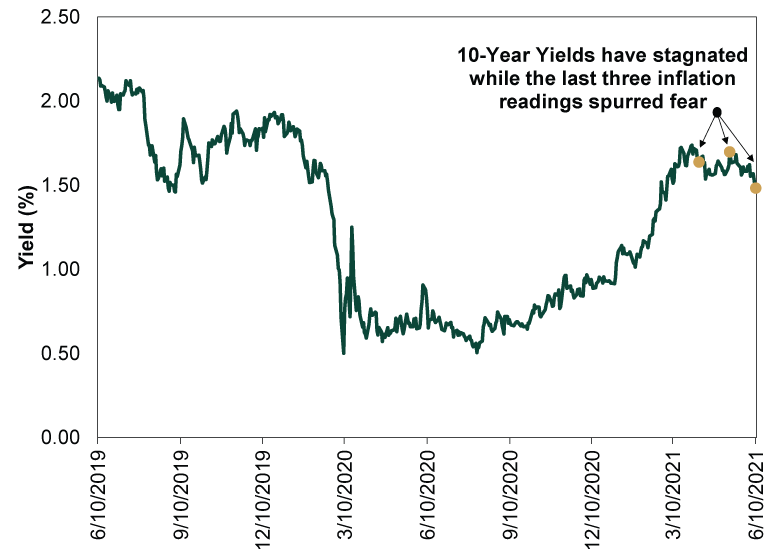

Markets (including Treasury yields) appear to agree.

Headlines are once again in a tizzy over inflation after May’s faster-than-expected US consumer price index (CPI) reading. But, just like April, we think there is little sign of lasting faster inflation in these data, which markets seemingly see. In our view, investors should follow their lead.

Headline CPI rose 5.0% y/y in May, accelerating from April’s 4.2% and logging the biggest uptick in 13 years, a fact the Bureau of Labor Statistics (BLS)—and seemingly everyone else—pointed out.[i] But like last month, that big year-over-year gain from deflationary lockdown levels is largely a garbage stat. Month-over-month data are somewhat more informative. In May, CPI rose 0.6% m/m, decelerating from April’s 0.8%. Even on this basis, though, we see plenty of signs the uptick is temporary—the effect of reopening and related supply chain issues.

Hence, in our view, the Treasury market’s telling “meh” reaction. Inflation and inflation expectations heavily influence longer-term Treasury yields. Why? While yields fluctuate in the open market, every given Treasury bond pays a fixed rate over time. The more inflation you get, the less buying power those fixed rates are delivering you. Hence, investors expecting hotter inflation typically demand higher yields.

But after climbing rather swiftly to start 2021, 10-year Treasury yields have been drifting lower in recent months—while the higher CPI reports have been emerging. (Exhibit 1) After today’s release, the 10-year yield dropped to a three-month low. Now that is admittedly short term. Perhaps rates reverse course. But it is safe to say this sideways-and-downward trend isn’t what you would expect markets to do if hot inflation were a material, lasting threat.

Exhibit 1: 10-Year Treasury Yield Shrugs at Inflation’s Jump

Source: FactSet, as of 6/10/2021. 10-year Treasury yield, 6/10/2019 – 6/10/2021.

Digging into the details supports the markets’ seemingly indifferent reaction, in our view: Temporary one-offs again led CPI’s month-over-month surge. Like April’s report, used car prices drove[ii] May’s big jump. Of CPI’s 0.6% m/m overall gain, one-third came from pre-owned vehicles’ 7.3% monthly pop.[iii] Note: That is down from April’s 10% monthly rise that added mightily to last month’s climb. More generally, reopening categories still underpin most of prices’ rise: auto rentals, airfares, apparel, new vehicles and household furnishings—the latter two tied to shortages from well-publicized supply-chain bottlenecks.

While the reopening effect boosting inflation could linger to an extent, the base effect on year-over-year rates is set to fade. Because of last summer’s reopening rebound, CPI troughed in May 2020. While June 2020 was still a pretty low base, the rising denominator from here means big year-over-year inflation rates will be harder to sustain in the coming months.

All in all, we find little in this report to suggest that the uptick in inflation is more than a temporary, lockdown-and-reopening-related phenomenon—one markets seem increasingly aware of. In our view, they are likely to look past it.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary Why Ken Fisher Is Optimistic About European Stocks

2026-07-23

2026-07-23 -

Economics A Summertime Check-in on US Consumers2026-07-23

-

Politics Blunting Burnham?2026-07-21

-

Market Analysis Why the SOX “Bear Market” Isn’t Foreboding2026-07-21

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today