Personal Wealth Management / Market Analysis

Fed People Write Words, Draw Dots

Once again, headlines read way too much into Fed communications.

Don't let the smile fool you-Janet Yellen is no longer feeling patient. Photo by Bloomberg/Getty Images.

Welp, the Fed is officially impatient, stocks are over the moon, and everyone is reading way too much into 157 words and two charts. Sorry folks, but we don't know the Fed's next move any more than we did yesterday.

For those who have miraculously avoided the media circus over the Fed's use of the word "patient" in its forward guidance, I (a) envy you and (b) am happy to summarize. Most of last year, Fed statements said overnight rates would stay low for a "considerable time" after the Fed's long-term bond buying ended, which Fed head Janet Yellen said amounted to six months or so. In December, the FOMC swapped "considerable time" for a pledge to be "patient" in raising rates. During that post-meeting press conference, Yellen said "patient" meant the Fed likely wouldn't hike rates for "a couple of meetings," helpfully adding that a couple means "two." Thus began Patient Watch 2015, with pundits parsing Yellen's February Congressional testimony for clues on when "patient" might go and start that two-meeting clock. Except when she testified, Yellen threw the two-meeting countdown out the window, saying a rate rise "could be warranted at any meeting."

Perhaps that is why today's Fed statement included some dizzying verbal gymnastics and one bizarre attempt at transparency:

To support continued progress toward maximum employment and price stability, the Committee today reaffirmed its view that the current 0 to 1/4 percent target range for the federal funds rate remains appropriate. In determining how long to maintain this target range, the Committee will assess progress--both realized and expected--toward its objectives of maximum employment and 2 percent inflation. This assessment will take into account a wide range of information, including measures of labor market conditions, indicators of inflation pressures and inflation expectations, and readings on financial and international developments. Consistent with its previous statement, the Committee judges that an increase in the target range for the federal funds rate remains unlikely at the April FOMC meeting. The Committee anticipates that it will be appropriate to raise the target range for the federal funds rate when it has seen further improvement in the labor market and is reasonably confident that inflation will move back to its 2 percent objective over the medium term. This change in the forward guidance does not indicate that the Committee has decided on the timing of the initial increase in the target range.

Not fluent in Fedspeak? Allow me to translate: They're holding the fed-funds target rate at 0-0.25%. As they plot their next move, they'll weigh how inflation, jobs, global growth and financial markets stack up with their long-term inflation and employment targets. They probably won't hike in April, but don't rule it out. Again, they gotta think about their targets, and who knows how any of that will go, so they really don't know what they'll do or when they'll do it.

But most coverage overlooked the hedging, seized on the "not in April" bit, coupled it with the "couple meetings" thing, and presto, everyone's penciling in a rate hike on June 17. One might think this would make markets freak, because everyone thinks rate hikes are bad![i] So why the jump? Well, there is usually no easy, singular explanation for what stocks do. But headlines say stocks jumped because, even though the statement was kinda rate-hikey, Fed members' interest rate projections were surprisingly, well, patient.

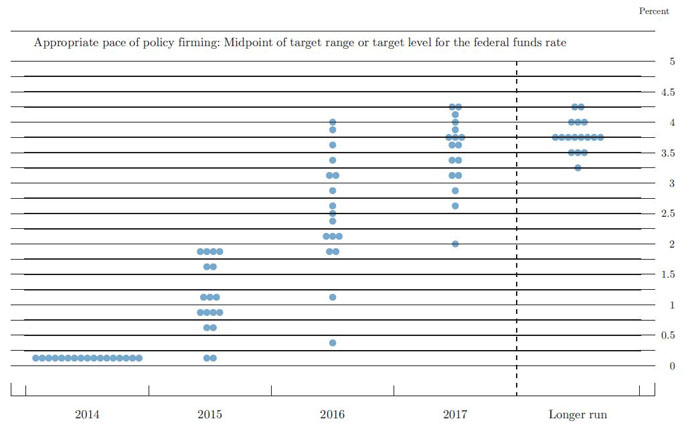

By projections, they're referring to what is colloquially known as the "dot plot"-charts showing where each Fed person believes rates will or should be in each of the next three years ... and beyond. For each year, each Fed person puts a dot at their chosen rate level-17 dots per year. Last December, the dots looked like this:

Exhibit 1: December 2014 Dot Plot

Source: Federal Reserve, as of 3/18/2015. Economic Projections of Federal Reserve Board Members and Federal Reserve Bank Presidents, December 2014.

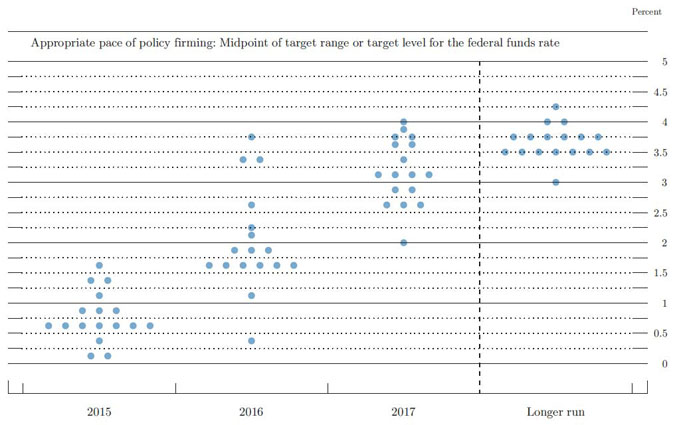

So Fed people presumed rates would spend 2015 somewhere between 0 and 2%, 2016 between 0.25% and 4%, and 2017 between 2% and 4.25%-with no strong consensus at any given level in any year. But now, the dots look like this:

Exhibit 2: March 2015 Dot Plot

Source: Federal Reserve, as of 3/18/2015. Economic Projections of Federal Reserve Board Members and Federal Reserve Bank Presidents, March 2015.

Now, not only do projected rates top out below 1.75% for 2015, but there is a cluster near 0.75%. In 2016, the max drops to 3.75%, with a cluster around 1.75%. 2017 has the same max projection but a clump in around 3%. So pundits are clumpy happy, assuming this means the FOMC plans to keep rates lower for longer.[ii]

The trouble here is twofold. One, the dot plot is a Rorschach test. Nothing more. Where pundits see four years of dovish monetary policy, I see an airplane[iii], a ballerina, a gingerbread lady and a flying saucer.[iv] These charts are entirely what you want to make of them, because they are nothing more than people's opinions at one moment. We do not know the meaning, conviction or logic behind them. Two, even if we knew all that, these projections aren't promises. Again, they are opinions, and opinions shift. That March's dot plot changed so radically from December's should be Exhibit A of why you shouldn't rely on anything the Fed writes or draws.

The Fed didn't etch its plans in stone Wednesday. It published a summary of 17 people's opinions based on their interpretations of recent economic data, which has all the permanence of an Etch-a-Sketch drawing. What they publish after April's meeting will depend on their opinions of whatever data come out in the interim, and those opinions could be different than today's opinions. June's opinions could be different still. Basing financial decisions on something this unreliable is folly.

Of all the Fed words excerpted above, you can probably toss all but these: "This ... does not indicate that the Committee has decided on the timing of the initial increase in the target range." Ok? They don't know what they're going to do! And that's just fine, because the minute they put policy on a preset course is the minute they open themselves to greater risk of error. Whether interest rates rise or not, in a vacuum, isn't important. What matter is whether they're right for the conditions at hand, and those conditions are unknowable today.

Beat the Crowd, by Ken Fisher with Elisabeth Dellinger, is available for pre-order now. Order your copy today!

[i] They are not. See this messy chart, for example.

[ii] I imagine some of the cheer is connected to a certain hedge fund manager's apocalyptic warning that today parallels 1937, when the Fed tightened aggressively and knocked the recovery off course. That's a ridiculous comparison. Rate hikes weren't the problem in 1937. Trouble came after the Fed jacked up reserve requirements, which have a far more powerful influence on money supply growth than the discount or fed-funds rates. That is simply not an issue today, when banks hold trillions in excess reserves.

[iii] My esteemed colleague Todd Bliman sees the bad guys from Space Invaders, the classic Atari videogame.

[iv] Not, alas, a dog, a cat and a horse with a hat on it.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Quick Hit: The July Jobs Nothingburger2026-08-07

-

Expert Commentary This Week in Review | Record Highs, US Jobs, Yen Intervention

2026-08-07

2026-08-07 -

Market Analysis Western Oil and Gas Producers Are Ramping Up2026-08-06

-

Politics The Tenth Question Facing Alberta2026-08-06

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today