Personal Wealth Management / Market Analysis

Four (of Many) Reasons to Be Bullish

A few signs the market probably isn’t peaking.

After a long, frustrating stretch with a lot of volatility and not much to show for it, this bull market is once again clocking new highs. Accordingly, investors are suffering a relapse of a time-honored malaise: fear of heights. But bull markets routinely hit new highs—even hundreds of them—and you can never tell which one is the peak until long after the fact. Index levels don’t predict bear markets. Nor does any one indicator. But there are some metrics we watch to assess whether a bear market might be lurking. Here is a sample of what we are monitoring today and why we believe they support our bullish stance.

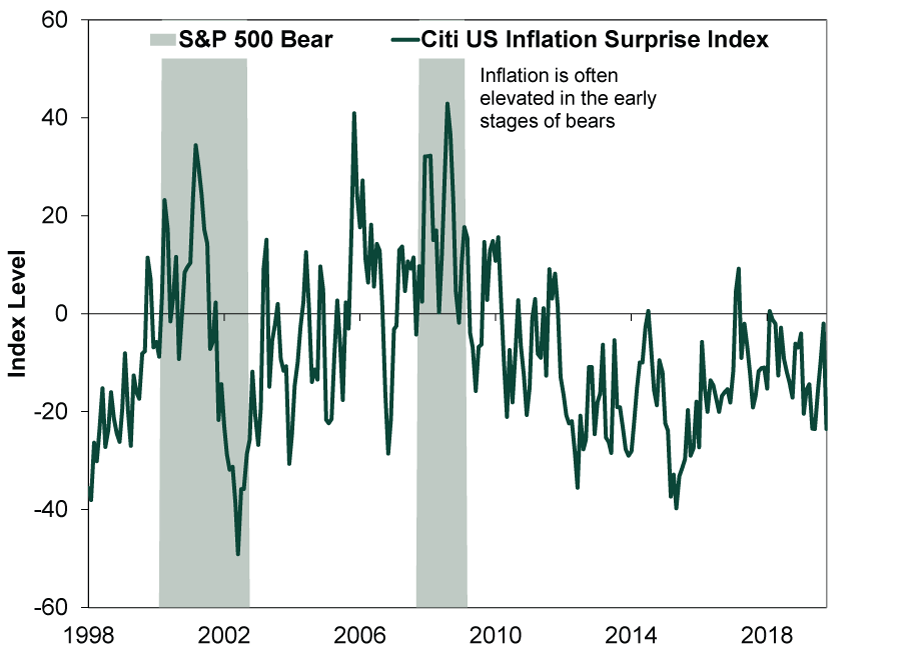

Muted Inflation: One common symptom of a late-cycle economy is an unexpected jump in inflation, which is evidence supply constraints are developing and not widely appreciated. Exhibit 1 shows the US inflation surprise index, which tracks how much inflation exceeds (or trails) expectations. It has been strong in the early stages of recent bear markets. In contrast, inflationary pressure today remains muted.

Exhibit 1: Citi US Inflation Surprise Index

Source: FactSet, as of 11/19/2019. Citi Inflation Surprise Index – United States, January 1998 – October 2019.

Credit Not Tightening: Tightening credit conditions are another common symptom of a late-stage economic expansion. The inverted US Treasury yield curve (when short-term exceed long-term rates) received considerable attention earlier this year, as yield curve inversion has preceded most modern US recessions. The yield curve matters because it is a rough proxy for bank profitability. However, it hasn’t historically been useful for short-term timing, and it doesn’t always signal a looming credit crunch. So, we also look for other symptoms of bank stress such as tightening credit conditions. Exhibit 2 shows the net percentage of banks reporting tighter credit conditions for commercial and industrial loans. Banks are often tight early in bear markets, but that isn’t the case today.

Exhibit 2: US Senior Loan Officer Opinion Survey: Net Percentage of Respondents Reporting Tighter Lending Standards for Commercial and Industrial Loans

Source: FactSet, as of 11/19/2019. Senior Loan Officer Opinion Survey, Net % of Domestic Respondents Tightening Standards for C&I Loans, Large & Medium Firms. Senior Loan Officer Opinion Survey, Net % of Domestic Respondents Tightening Standards for C&I Loans, Small Firms, Q1 1990 – Q4 2019.

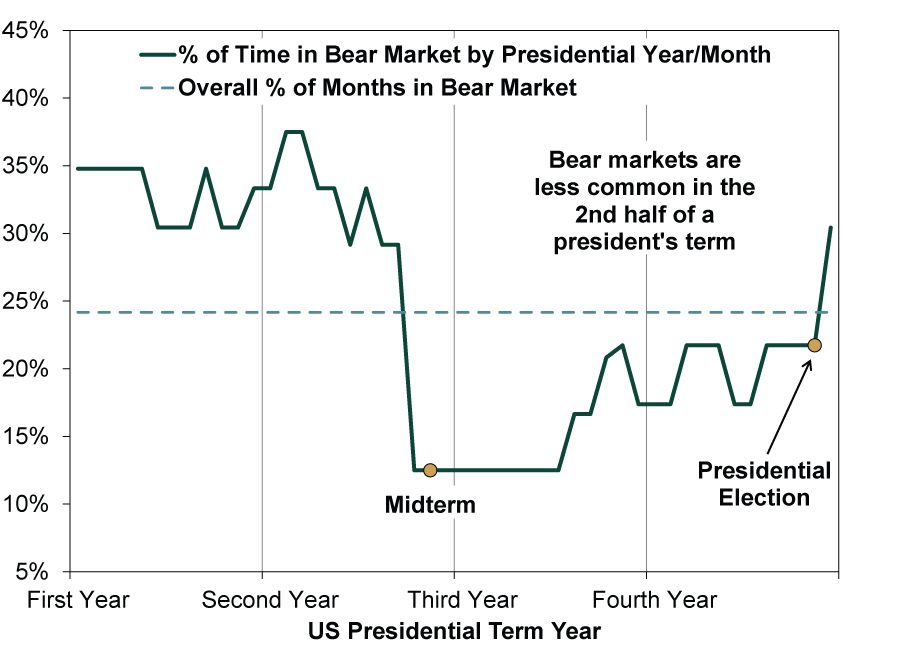

Political Gridlock: We also believe politics has a heavy influence on markets—in particular, the presidential election cycle. As Exhibit 3 illustrates, bear markets historically occur more frequently in the first two years of a new presidency. We believe this is because new presidents’ ability to pass major legislation is strongest in their first two years, thus heightening legislative risk in the first half of their term. Stocks generally dislike it when Congress is capable of passing radical legislation, as it increases the risk of policies interfering with property rights and creates uncertainty. However, after the midterm election, the President’s party almost always loses seats, frequently resulting in a do-nothing gridlocked Congress. The result is less change and more clarity for business. While a presidential election is approaching, it is still a year away, which we think bodes well for stocks in the intermediate term.

Note, Exhibit 3 doesn’t mean a bear market is the most likely outcome for 2021 or 2022. Even though the historical frequency of bear markets is higher in years one and two, it is still below 50%. Returns in a president’s first half aren’t uniformly bad—just more variable. How 2020’s election will affect legislative risk depends not only on who wins the election and what investors’ expectations are, but how much clout they have in Congress and the likelihood that actual legislation is worse or better than investors anticipate. This is all unknowable today.

Exhibit 3: Percentage of Time US Stocks Are in a Bear Market

Source: FactSet, as of 11/19/2019. Historical percentage of months the S&P 500 has been in a bear market by year of the US president’s term, December 1925 – October 2019.

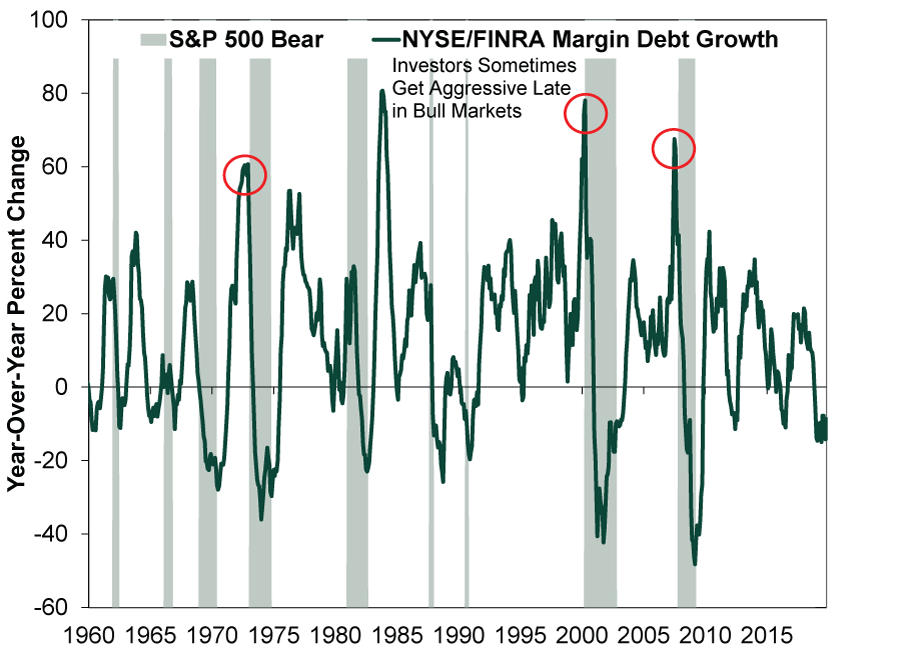

Investor Sentiment: Lastly, beyond economics and politics, we believe sentiment is a powerful market driver. Euphoric investor sentiment often accompanies stock market peaks since it may reflect over-optimistic expectations, where even moderately good news can disappoint investors. One way to measure investor sentiment is the use of margin debt. Exhibit 4 shows the growth rate for US margin debt, reported by FINRA. In our view, the level of margin debt outstanding doesn’t mean much, but a rapid rise can be a sign of fast-changing sentiment. While margin debt spikes are not a guarantee of a coming bear market, we have seen extensive margin use near some previous market peaks. Today, margin debt is shrinking, which doesn’t mean a bear market can’t happen, but it does help illustrate that expectations are probably not too exuberant.

Exhibit 4: NYSE/FINRA Margin Debt Growth

Sources: Global Financial Data, Inc., and FINRA, as of 11/19/2019. NYSE Margin Debt year-over-year percentage change, January 1960 – January 2010. FINRA Debit Balances in Customers’ Securities Margin Accounts year-over-year percentage change, February 2010 – October 2019.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary 3 Things You Need to Know This Week | Q2 Earnings, ECB Meeting, Trump Accounts

2026-07-20

2026-07-20 -

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—July 13 - July 172026-07-20

-

Expert Commentary This Week in Review | US-Iran Conflict, US Inflation, New UK Prime Minister

2026-07-17

2026-07-17 -

Market Analysis Pumping Up the Yen?2026-07-17

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today