Personal Wealth Management / Market Analysis

Geopolitics and Markets - Israel and Iran

Putting concerns over Middle Eastern geopolitical tensions in context.

Heightened tensions between Israel and Iran are again dominating headlines. In our view, while a surprise Israeli attack is possible, assigning a probability isn’t truly possible—attempts to do so strike us as highly speculative. (We might add there are a number of aspects of the media reporting of this story that are equally, if not even more, speculative.) That said, it seems apparent given the relative strength and degree of economic and military advantages Israel and its allies have over Iran, the risk of sustained military action after such an event is quite low. Further, the timing of such an attack would be near impossible to predict. As for the capital markets impact (our primary point of interest in geopolitics) history shows even large-scale geopolitical events tend to have a fleeting, and not necessarily negative, impact on market direction.

Part of the concern surrounds the potential that Iran may attempt to blockade the Strait of Hormuz, which could spike oil prices. The Strait of Hormuz is the most important crude oil bottleneck in the world—approximately 17 million barrels of oil (just under 20% of global consumption) travels through it each day. Again, a blockade is a possibility, but, in our view, the probability of a sustained blockade is low. First, the US has an overwhelming military advantage over Iran. Further, Iran is not the only oil-producing nation that uses the Strait of Hormuz—other OPEC members, some of them friendlier to Iran (relatively), don’t want the Strait blocked. What’s more, Iran is economically dependent on its oil trade. The nation hurt most by an Iranian blockade—even a short-lived one—is Iran.

Overall though, flaring Middle East tensions are neither new nor unusual. And while some claim Iran has never been so near the military ability to “eliminate Israel,” as its threatened for years, fears of a pre-emptive Israeli strike aren’t new either. (Moreover, we’d note the discussion of Iran being close to possessing a nuclear weapon is also highly speculative—there’s been no successful nuclear test and nearly every report indicates they’re some distance away.) Most frequently, the tensions amount to nothing more than saber rattling. Investors avoiding stocks during periods of heightened Middle East tension would find themselves invested very rarely. And yet stocks rise approximately 72% of all years.

What’s more, stocks tend to have a brief reaction to short-lived military action—particularly military action that’s long been anticipated. Consider 1981’s Israeli bombing of an Iraqi nuclear facility—stocks barely wiggled. Terror strikes similarly have had fleeting market impact. Even following the September 11 terror strikes, arguably the most significant in recent memory, stocks fell sharply but reversed course just as fast and were trading above September 10 levels a month later—and remained above those levels for months.

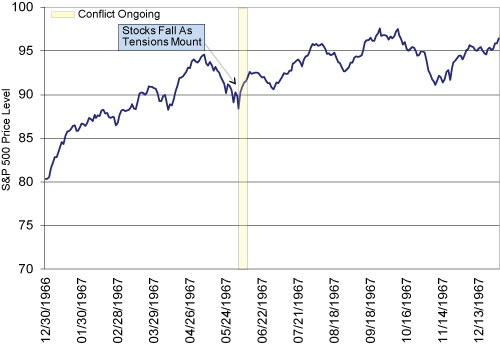

In terms of larger scale geopolitical events, the uncertainty leading up to the outbreak of war tends to depress stocks, but when bullets are exchanged, alleviated uncertainty can be a bullish factor. Consider 1967’s Six-Day War, in which Israel was invaded by neighboring Egypt, Jordan and Syria. Stocks fell slightly in the run-up to conflict—but then rose every session after the outbreak of conflict. (See Exhibit 1.) More importantly, an ongoing global bull market wasn’t knocked off course.

Exhibit 1: The Six-Day War and S&P 500 Returns (Price Level)

Source: Global Financial Data, Inc., as of 02/14/2012.

The same effect occurred in the run-up to and start of the first and second Gulf Wars. In both instances, stocks were depressed in the period before, and new bull markets started close to the start of hot conflict. Saddam Hussein invaded Kuwait on August 2, 1990, and the already-ongoing bear market bottomed October 11, 1990. Operation Desert Storm began January 17, 1991—but that bull market ran until March 2000.

The second Gulf War began when the US invaded Iraq on March 20, 2003—mere days after the US and global bear market double bottomed and a five-year bull market kicked off in earnest.

The Afghanistan War began on October 7, 2001, amid a counter-trend rally in an ongoing bear market. That bear market, which started in March 2000 and doubled-bottomed in March 2003, had little to do with Middle East tensions and nearly everything to do with a major Tech-sector implosion.

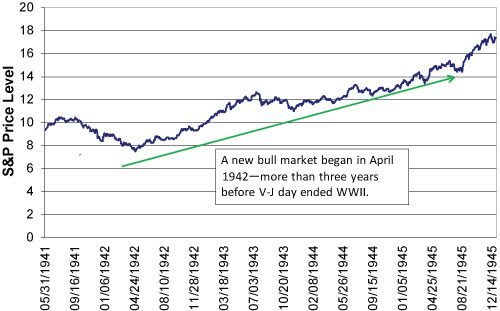

History shows armed conflict rarely has a lasting impact on market direction. The onset of World War II in Europe is the only modern example in which war had a lasting impact on market direction. A nascent bull market kicked off in 1938 but was truncated soon after the Nazis invaded the Sudetenland. Stocks didn’t bottom until 1942, kicking off a new bull market three full years before the end of World War II. Stocks can and do rise during periods of even major armed conflict. (See Exhibit 2.)

Exhibit 2: S&P 500 Price Level During US Involvement in World War II

Source: Global Financial Data, Inc., as of 02/14/2012.

But WWII was massive and bears little, if any, resemblance to Iranian tensions. In virtually all other wars and periods of tension, the start of armed conflict hasn’t been a material, lasting bearish factor. More often, the removal of uncertainty has been a positive factor.

It’s near-impossible for us to predict whether a single nation may act unilaterally in striking another nation. However, we believe the outbreak of major, protracted war is a low probability, and there’s little if any evidence such an event would be a lasting, bearish factor for stocks.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis The New Tariffs in Town Are Still Old News2026-07-24

-

Expert Commentary This Week in Review | Market Volatility, Tariffs, SpaceX

2026-07-24

2026-07-24 -

Expert Commentary Why Ken Fisher Is Optimistic About European Stocks

2026-07-23

2026-07-23 -

Economics A Summertime Check-in on US Consumers2026-07-23

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today