Personal Wealth Management / Economics

Global Economy: Look Beyond Manufacturing

There is more to an economy than just building stuff.

Is manufacturing sending a warning signal? Several indicators slowed or fell in September, fueling a "Manufacturing Stalls!" narrative worldwide and compounding fear of a faltering global economy. As ever, though, the headlines don't tell the full story. If you take a broader look and consider some of the data's nuances, the world appears to be in better shape than the gloomy narrative implies. Growth may not be gangbusters these days, but reality should exceed investors' expectations, providing fundamental support for stocks.

The fear largely stems from Purchasing Managers' Indexes (PMI), surveys that loosely measure the percentage of firms growing in a given country. If the reading tops 50, the majority of firms surveyed reported growth, and PMI calls it an expansion. Below 50 is supposedly contraction. If the PMI falls from one month to the next but stays above 50, growth supposedly slowed.

Using the official interpretation of PMIs, September was rough. Both of China's PMIs fell below 50. The US's slipped to 50.2, the UK's to 51.5 and the eurozone's to 52.0. PMI would characterize China as contracting and the West slowing to a crawl, but that isn't quite how it works. PMIs estimate the breadth of growth nationally, not the magnitude. If the number is below 50, and the firms reporting growth grew by a larger amount than the other firms contracted, then a "contractionary" PMI could obscure actual growth. Same goes for a supposedly slower PMI-a downtick in the breadth of growth may actually obscure acceleration. As evidence, French manufacturing PMIs have spent much of the past two years below 50, yet France keeps growing. PMI wobbles often aren't all that telling.

China's PMIs come with even more caveats. The Caixin/Markit gauge, which includes smaller, private firms, slipped to 47.2 in September-a six-year low. That stole headlines, but it actually isn't a new development. Caixin's Manufacturing PMI has spent most of the last four years in contraction-and China kept growing at a fast clip, as private manufacturers don't really reflect the broader economy. For one, they have borne the brunt of the country's overcapacity issues. Private steelmakers dealt with headwinds like the forced destruction of blast furnaces last year. Small firms also have trouble securing financing since the big state-owned banks prefer lending to big state-owned firms. The big players have thus held up much better, and the official PMI has long reflected that. Until now, that is, with readings of 49.7 and 49.8 for August and September, respectively, renewing long-running hard-landing fears. But given PMIs' limitations, that doesn't mean China is actually contracting. We'd cast it in a different light: a symptom of China's slow shift from industry-led growth to consumption and services Chinese manufacturing's slowdown is consistent with the trend of the last few years, which have seen China's service sector gain prominence and become the primary growth engine.

Which brings up another point: For all the eyeballs on factories, services-health care, transportation and accommodations, finance, retail, entertainment, etc.-account for the lion's share of output in most developed countries and a growing share in many Emerging Markets.

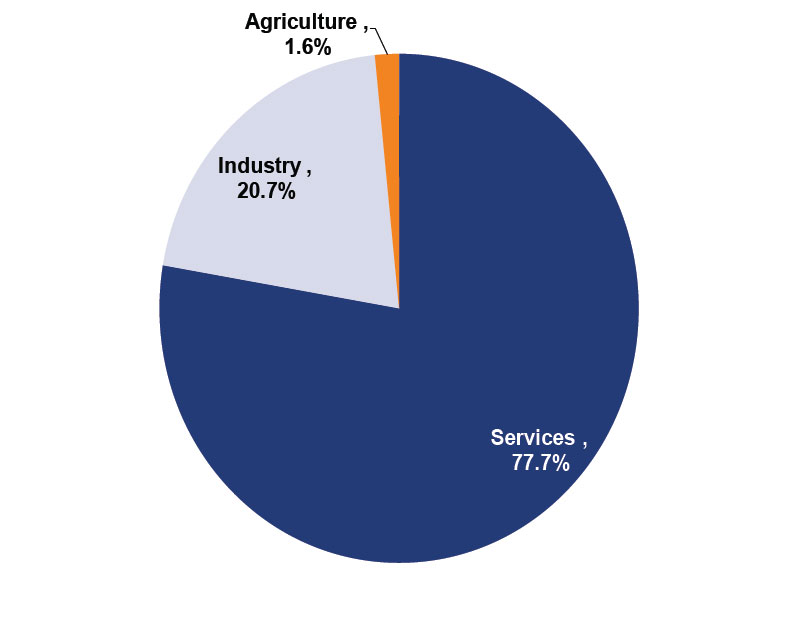

Services accounts for 77.7% of US output, 68.4% of German output, 74.3% for Japan, and an even bigger 78.9% for France and 78.8% for the UK. China's services sector comprises 48.2% of GDP-less than half, but still the biggest share of China's economy.

Exhibit 1: US GDP - By Sector of Composition

Source: CIA World Factbook, as of 10/5/2015.

Exhibit 2: China GDP - By Sector of Composition

Source: CIA World Factbook, as of 10/5/2015.

Service-sector numbers are overall stronger than manufacturing numbers globally and have been for a while. China retail sales grew 10.4% y/y in August. Though this is just one subset of overall consumer spending, it shows that even as manufacturing slows, the bigger portion of China's economy is likely growing at a strong pace. The UK's service sector output grew 2.8% y/y in July, the sixth straight rise, with all four main components up. Eurozone August retail sales climbed 2.3% y/y, and US consumer spending-which, unlike retail sales, includes spending on services-climbed 3.2% y/y. Incomplete views of the service sector, granted, but encouraging all the same.

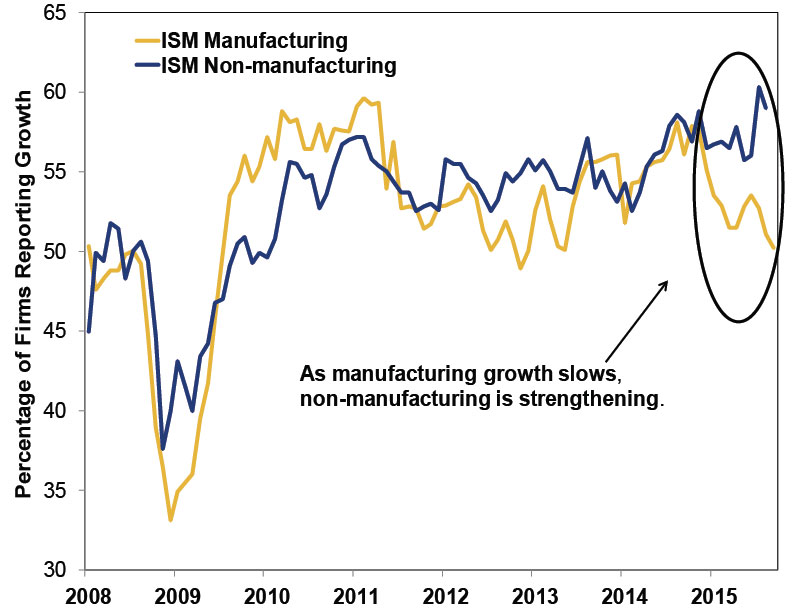

Service PMIs top Manufacturing PMIs across the board, too-53.7 in the eurozone, 53.3 in the UK and 56.9 in the US[i] in September. Yes, service PMIs are also squishy, with all the same caveats, but big gaps between services and manufacturing are a good sign the biggest part of the economy is in fine shape (despite the fact all these service gauges slipped a tad from August-again, wobbles aren't all that meaningful much of the time).

Exhibit 3: US ISM Manufacturing and Non-Manufacturing PMIs

Source: Factset, as of 10/5/2015.

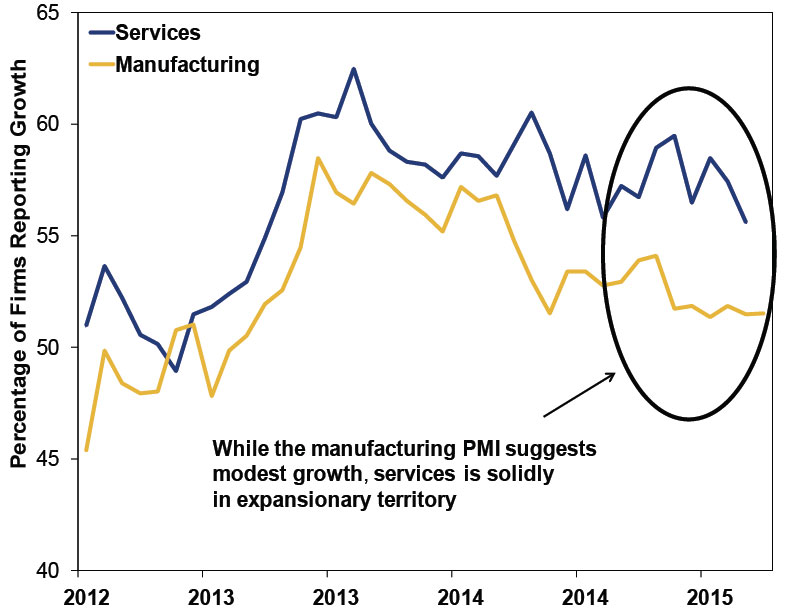

Exhibit 4: UK Manufacturing and Services PMIs

Source: Factset, as of 10/5/2015.

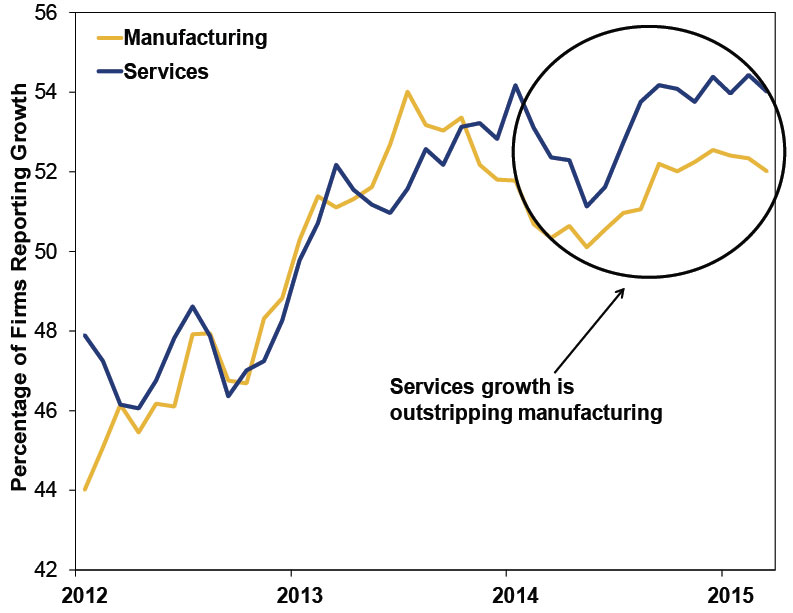

Exhibit 5: Eurozone Manufacturing and Services PMIs

Source: Factset, as of 10/5/2015.

Some fear manufacturing's slowdown is a harbinger for the broader economy, but that often isn't the case. Long ago, when our economy was factory-intensive, a slip in output or demand could reliably signal widespread trouble. But it is an antiquated view in a service-driven age. It lingers, we presume, because most of our economic data center on manufacturing-industrial production, factory orders, durable goods, man-hours, you name it. Output per unit of labor, the traditional definition of productivity, is rooted in a heavy-industry mentality. Service-sector growth is much harder to quantify in a timely fashion, and of major countries, only the UK has a monthly output index. We can get close with retail sales and consumer spending, but these are seen as softer figures. Manufacturing is more tangible-stuff we make.

But manufacturing has no magical predictive powers. Its surges don't necessarily precipitate booming growth, and its dips don't always foretell broader declines. It is one segment of our economy, with its own drivers. The service sector has its own drivers, only some of which overlap. Troubles in one sector aren't always contagious. Often they stay isolated, as we've seen in Energy this year. Troubles in manufacturing may be visible earlier than troubles elsewhere, but that is a data-collection issue only. It speaks to the need for statisticians to get better at measuring demand and output in the service sector. PMIs try to do this, with their service new orders indexes, but it is still a work in progress. The same goes for trade. Trade in goods is easy to tabulate-just add up the customs bills. Trade in services is harder.

So regardless of whether manufacturing wobbles further, investors should take a more holistic view of the global economy. That will give you a more accurate view than those who over-focus on manufacturing, and today, that broader view will reveal a world on much firmer footing than many believe.

[i] The US number covers all non-manufacturing segments of the economy, including mining and construction as well as several service industries.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary This Week in Review | Global PMIs, SpaceX, RMD Planning

2026-07-10

2026-07-10 -

Market Analysis Trim Your Angst on Economic Measurement Tweaks2026-07-09

-

Politics Long-Term Forecasts and Court Verdicts: The Latest in British and French Politics2026-07-09

-

Corporate Information How You Benefit from Fisher Investments' Transparent Fee Structure

2026-07-08

2026-07-08

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today