Personal Wealth Management /

Gold Climbs, Still Isn’t a Good Long-Term Investment

Despite nearing record highs set nine years ago, gold still isn’t a good choice for the huge majority of investors, in our view.

Gold is having a moment right now. Prices, up 19.3% this year, sit near all-time highs set in 2011.[i] Inflows into gold-linked funds in the year’s first half surpassed the prior annual record. Why all this interest? Among the many narratives that are likely contributing, gold allegedly hedges against equity market declines. With many fearing a second shoe is about to drop and send stocks back towards March 23’s bear market low, a haven may seem alluring. In our view, though, gold is a fatally flawed long-term investment—and one that would require remarkable timing to do well with near term. Hence, we think it is tough to make the case for a material allocation to gold in the vast majority of investors’ portfolios.

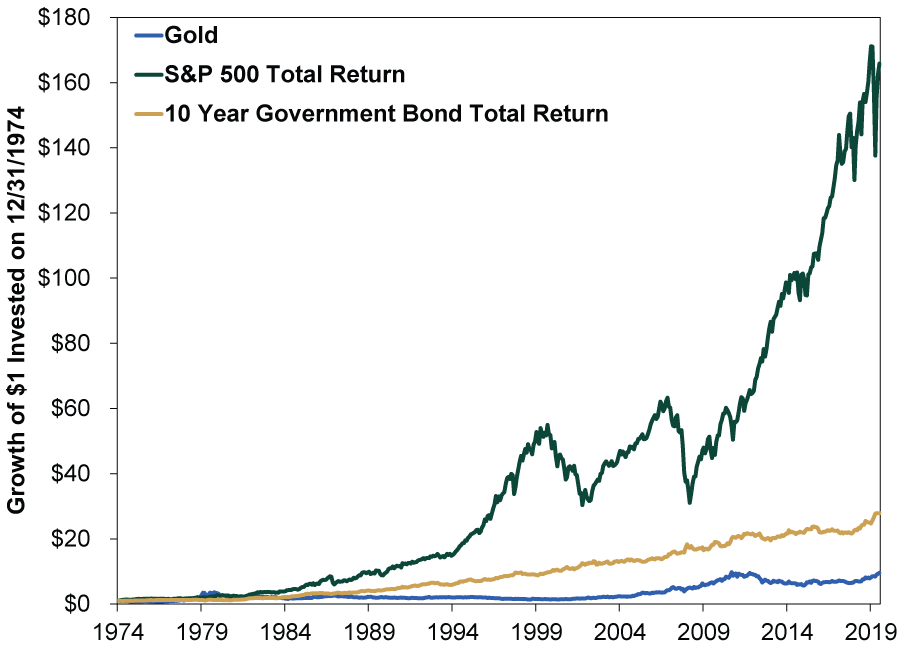

Gold’s recent jump higher—and its year-to-date outperformance versus stocks—is, well, historically atypical. Since US investors could legally own investment gold in the mid-1970s, it has posted a cumulative 868% gain.[ii] Sound shiny? Consider Exhibit 1, which shows stocks have crushed gold over this span. Even government bonds’ total returns are far, far ahead of gold.

Exhibit 1: Gold Returns Lags Stocks’ and Bonds’

Source: Global Financial Data, Inc. as of 7/9/2020. Growth of $1 invested in the US 10-Year Government Bond Index, S&P 500 Total Return Index and gold prices, 12/31/1974 - 6/30/2020.

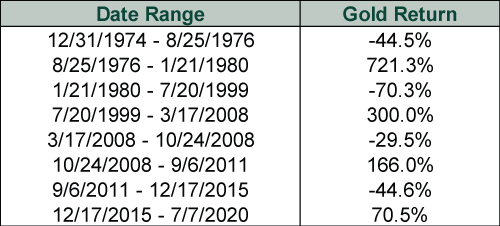

What’s more, it isn’t like gold’s performance has been a smooth or steady climb to those relatively low returns. We could excuse the vast long-term underperformance if that were the case. Yet the bulk of gold’s gains have come in just four stretches—bursts of upside bracketed by long flat-to-down periods. Missing any of these booms would severely affect returns. Exhibit 2 shows several long stretches of flattish or negative gold returns—like the one running from January 1980 through July 1999. This period contained multiple stock market cycles and epic equity bull markets, including 1982 – 1987 and most of the 1990s’ huge bull market.

Exhibit 2: Gold’s Boom/Bust Cycles

Source: FactSet, as of 7/9/2020. Gold price percentage change, 12/31/1974 – 7/7/2020.

This burst-and-bust history hints at another reality. Lower returns than stocks might be fine if gold offered substantially less volatility. After all, bond returns don’t match stock returns over the long run. But bonds compensate for their lower returns with less volatility, making them a potentially valuable part of portfolios for investors whose goals are consistent with less volatility. However, gold is more volatile than either stocks or bonds. Exhibit 3 shows this by comparing the historical one-year standard deviation of stocks, gold and bonds. Standard deviation (yellow columns) measures the degree to which historical returns fluctuate around their average—a higher number means it varies more, implying bigger volatility.

Exhibit 3: Gold’s Higher Volatility Over 1-Year Rolling Periods

Source: Global Financial Data, Inc. as of 7/9/2020. Average annualized rate of return for the S&P 500 Total Return Index, USA 10-year Government Bond Index and gold price.

Even if one chooses to view volatility differently—just the magnitude of swings versus one another—gold is still bouncier. From December 31, 1974 through June 30, 2020, gold’s average and median monthly movements (up or down) were 3.87% and 2.81%, respectively.[iii] The S&P 500’s were 3.42% and 2.58%—lower than gold’s, although stocks’ more frequent positivity generated the far higher returns shown in Exhibit 1.[iv] As for bonds, Global Financial Data’s 10-year US Treasury Index posted average and median monthly returns of 1.85% and 1.41%, illustrating their lower volatility.[v] Volatility isn’t inherently bad—higher volatility often accompanies higher returns. Not so with gold, though.

In our view, the explanation for gold’s high volatility and subpar returns lies in its supply and demand drivers. Gold supply tends to rise at a fairly slow and consistent rate over time, considering every ounce of gold mined is still in existence. Gold demand, meanwhile, tends to be highly volatile. Since gold has few industrial uses, demand typically fluctuates with investor sentiment. When folks fear big market declines (usually just as or after one has occurred), inflation, a falling dollar or one of the many other things gold purports to hedge against, they often bid it up rapidly for a time. The upshot: Gold moves in psychologically driven, often massive short-term price swings—exceedingly difficult to time, in our view.

As for gold’s inferior returns, we think this stems from the fact it is a commodity, not a company. Firms can innovate, evolve, respond to market incentives and grow over time. As humans flourish, so, overall and on average, do publicly traded companies. Gold—like other commodities—has no such connection to economic growth and progress. It just, well … sits there.

In turbulent times, gold’s shine seemingly attracts more investors. Headlines touting all-time high gold prices and doom-and-gloom stock market forecasts lure many. In our view, though, investors shouldn’t overlook gold’s high-volatility, low-return history.

[i] Source: FactSet, as of 7/16/2020. Gold price, 12/30/2019 – 7/15/2020.

[ii] Ibid. Gold price, 12/31/1974 – 7/15/2020.

[iii] Ibid, as of 7/10/2020.

[iv] Ibid.

[v] Ibid.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Politics Blunting Burnham?2026-07-21

-

Market Analysis Why the SOX “Bear Market” Isn’t Foreboding2026-07-21

-

Expert Commentary 3 Things You Need to Know This Week | Q2 Earnings, ECB Meeting, Trump Accounts

2026-07-20

2026-07-20 -

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—July 13 - July 172026-07-20

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today