Personal Wealth Management / Market Analysis

Greek Contagion Risk Is Minimal

Seven charts show Greece's problems are contained.

Flags fly in front of the Parthenon in Athens. Photo by Bloomberg/Getty Images.

After five years of Greek crisis, two defaults and going-on three bailouts, many still fear a contagion across the eurozone. While default and "Grexit" risk persist, the risk of a contagion has fallen significantly over the last few years. The eurozone economy is improving, foreign banks hold less Greek debt, bank deposits aren't fleeing other peripheral nations, and euroskeptic parties poll well behind traditional parties across the eurozone. Greece's problems are contained and shouldn't put the broader eurozone at risk.

Improved Economic Environment: Peripheral Economies Are Growing Again

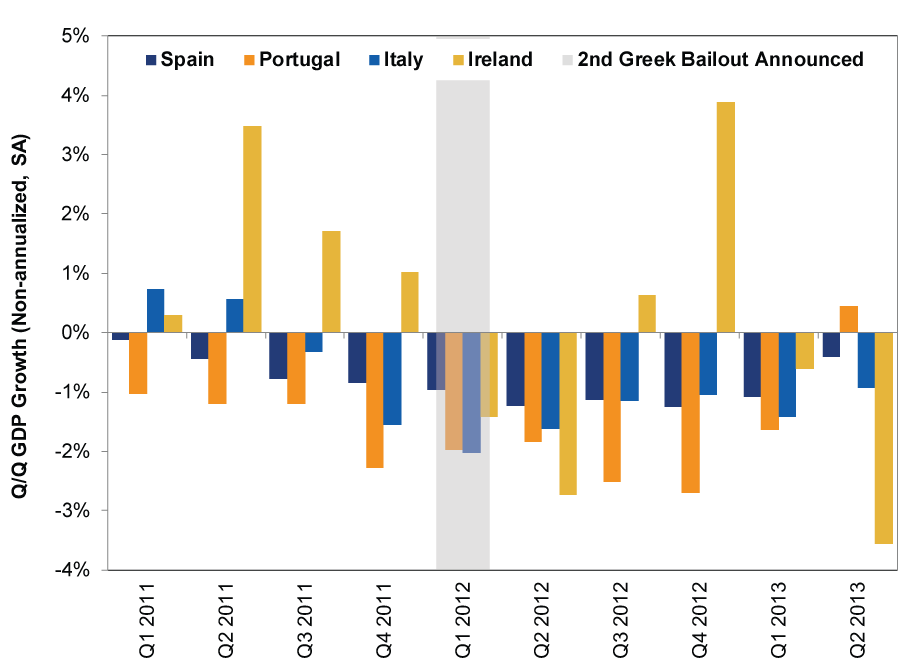

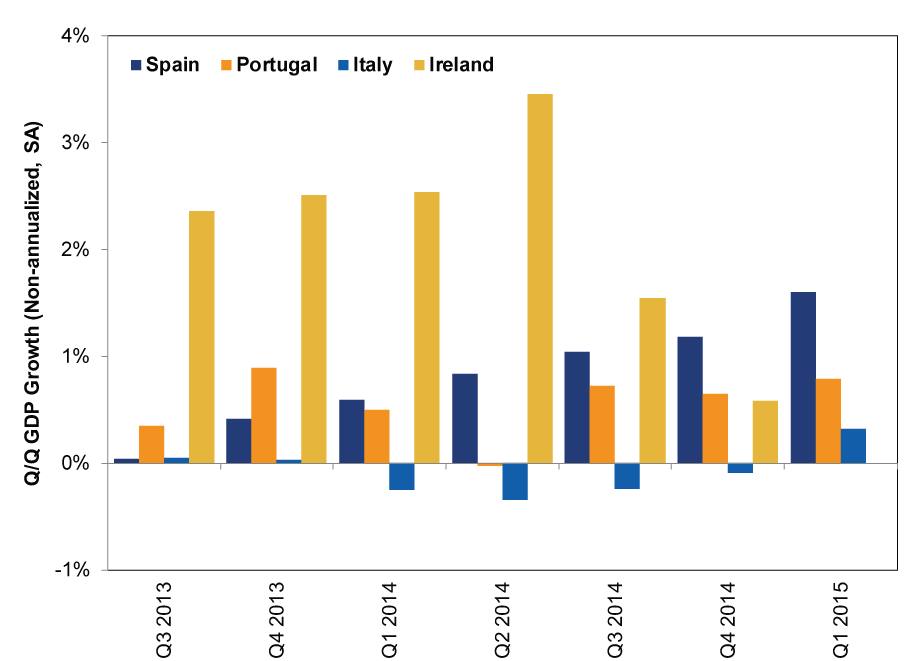

Since the sovereign debt crisis began, concerns about a "Grexit" hurting the eurozone economy have persisted. While a Greek default and exit from the eurozone could create a headwind, the bloc's economy is much stronger today than it was at the peak of the crisis (Exhibit 1). Spain, Italy, Portugal and Ireland have all resumed growing (Exhibit 2). Greece's economic backslide this year didn't drag them down.

Exhibit 1: Peripheral Eurozone GDP Growth During Greece's Second Bailout

Source: FactSet, as of 7/27/2015.

Exhibit 2: The Periphery Has Resumed Growing

Source: FactSet, as of 7/27/2015.

Greek Debt Ownership: International Banks Hold Significantly Less

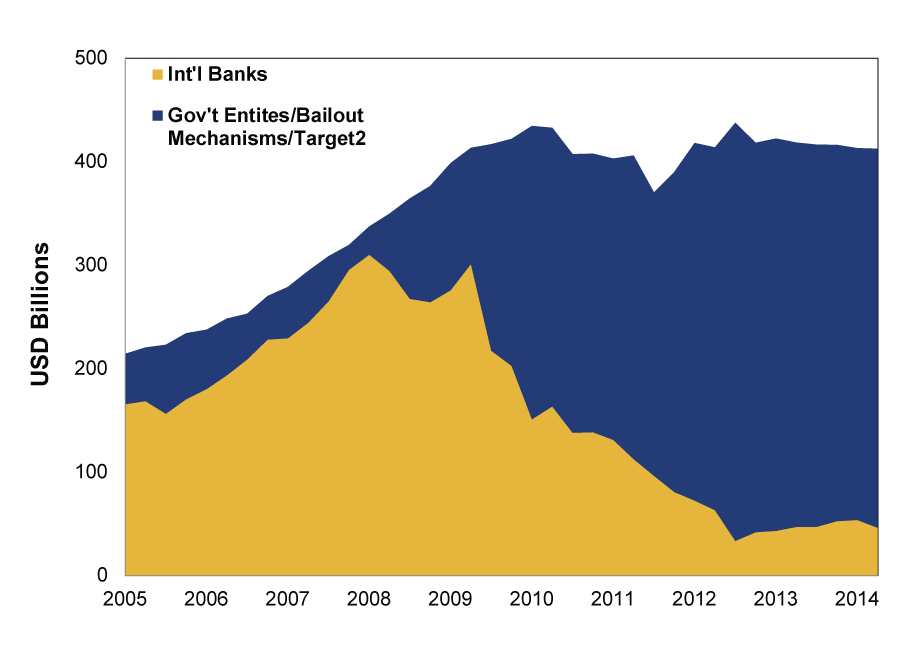

When the crisis began, many cited foreign banks' large holdings of Greek debt as a conduit for contagion, fearing a Greek default would trigger significant write-downs at foreign banks, forcing governments to recapitalize them-a high-cost endeavor that could in turn push those nations into default, leading to the European banking system's collapse. Since then, however, foreign banks have significantly reduced their exposure to Greek debt, offloading their holdings to various bailout mechanisms and the ECB. Their collective exposure is down to just €46 billion, significantly reducing the risk of a banking crisis. When Greece wrote down about €100 billion in debt owed to private sector creditors in 2012, banks and markets barely blinked.

Exhibit 3: Who Holds External Greek Debt

Source: Bank for International Settlements, as of 7/27/2015.

Greek Default Risk Has Limited Impact on Other Periphery Yields

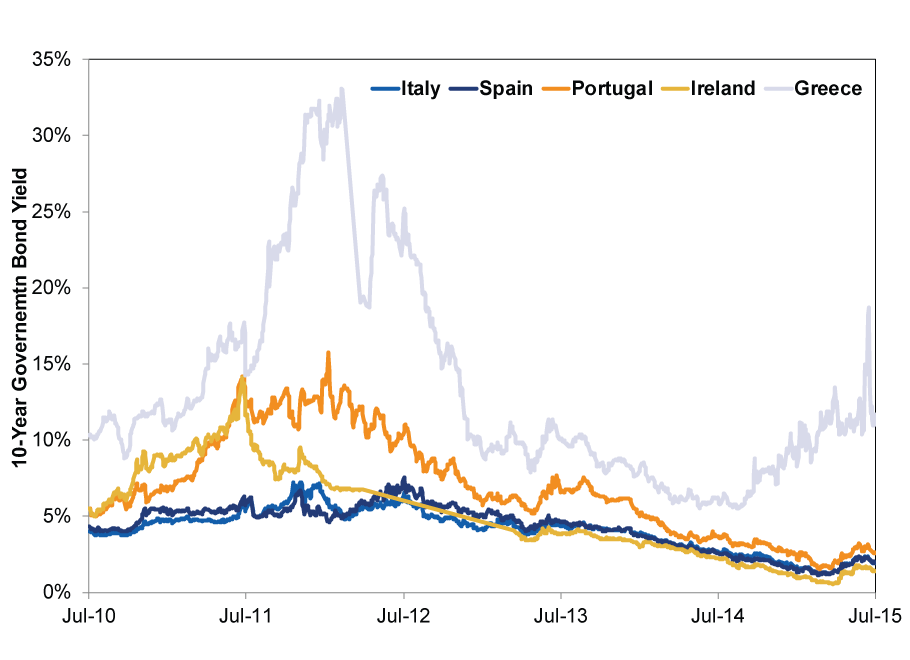

Because foreign bank hold far less Greek debt and the eurozone economy is improving, rising Greek default risk has a muted impact on other peripheral nations' bond yields. Interest rates have fallen significantly since Mario Draghi's famous "whatever it takes to save the euro" speech in 2012. While yields did start climbing in late April, that likely had less to do with Greece and more to do with global yields climbing. The US 10-year bond yield, for example, climbed 25bps from April 28th to July 31st.[i] The ECB is currently in the middle of a €1 trillion asset purchase program and has indicated they will increase purchases if necessary. Notably, when Greece's latest round of brinksmanship caused Greek yields to spike in late June and early July, other peripheral yields rose just a bit. Spain, Italy, Ireland and Portugal now trade much more like the eurozone core than Greece.

Exhibit 4: Greek Yields Are an Outlier

Source: FactSet, as of 7/27/2015.

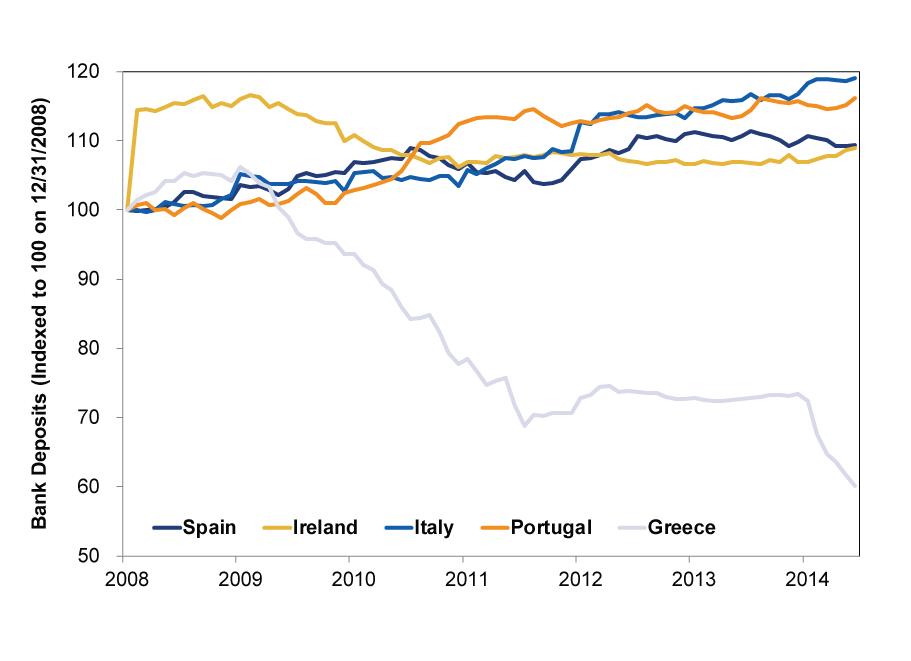

Deposits at Periphery Banks: Deposit Flight Is Isolated to Greece

Compounding Greece's problems, deposits have fled from Greek banks, falling by 40% since December 2008. Deposit flight has forced Greek banks to rely on ECB emergency liquidity, and recapitalizing them will add to the government's debt. Banks elsewhere in the periphery are in much better shape. Deposits at Spanish, Italian, Irish, and Portuguese banks have all risen since that date and remain stable or rising, depending on the country. If there were significant concern of additional exits from the eurozone, deposits would likely have been more turbulent in other periphery nations as savers and businesses sought to protect their cash reserves from currency conversion and likely devaluation.

Exhibit 5: Deposits at Eurozone Periphery Banks

Source: FactSet, as of 7/27/2015.

Political Contagion: Euroskeptic Parties Remain Well Behind Traditional Parties

The final aspect to Greek contagion fears is political contagion-the risk the anti-austerity Syriza party's electoral success in Greece would trigger a wave of support for euroskeptic anti-austerity parties in the rest of the periphery, most notably in Spain and Portugal, which hold elections this year. After Syriza won the election in January, support for parties like Spain's Podemos did rise, but Syriza's acceptance of draconian bailout terms in July seems to have sapped some of the enthusiasm for other protest parties. Recent polls in the rest of the periphery show traditional parties remain well ahead of euroskeptic parties. The trend is relatively steady across the board with only modest gains by euroskeptic parties in Portugal and Italy.

Exhibit 6: Greek Election Results

Source: Greek Interior Ministry, as of 1/26/2015.

Exhibit 7: Greek Election Results

Source: Celeste-Tel, Eurosondagem, SWG, The Sunday Times, as of 7/27/2015.

[i] FactSet, as of 8/7/2015.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Politics Blunting Burnham?2026-07-21

-

Market Analysis Why the SOX “Bear Market” Isn’t Foreboding2026-07-21

-

Expert Commentary 3 Things You Need to Know This Week | Q2 Earnings, ECB Meeting, Trump Accounts

2026-07-20

2026-07-20 -

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—July 13 - July 172026-07-20

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today