Personal Wealth Management / Market Analysis

Growth Versus Guidance

The UK LEI’s 1.5% rise in September is just the latest evidence the end of quantitative easing is good for growth—likely to the surprise of most investors.

Does BoE Governor Mark Carney see more economic growth ahead for the UK? Source: Pool/Getty Images.

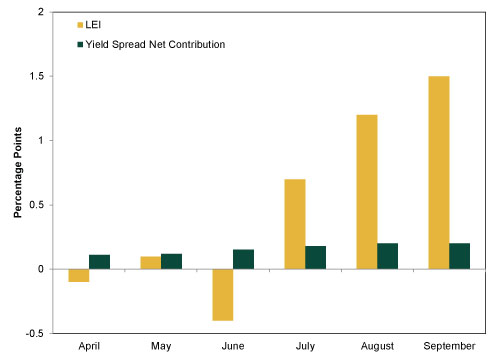

How can you tell if an economic indicator is worthwhile? Here’s an easy acid test: Does the media use it? If they don’t, chances are it’s worth exploring—one time-honored trick for investors seeking a leg up is to look where most people don’t. These days, few look at The Conference Board’s Leading Economic Index (LEI) series—the US LEI occasionally gets some play, but barely anyone seems to notice the Conference Board publishes similar series for the UK, 10 other major countries and the eurozone. Though LEI doesn’t perfectly predict economic inflection points, economies have tended to follow its longer-term trends more often than not. UK LEI, for example, started an upswing before the country’s economic recovery took off this year and has accelerated in recent months—and sped up again in September, rising 1.5% m/m. Along with high and rising LEI throughout much of the world, it’s just one more piece of evidence pointing to a faster-growing global economy—something many investors don’t appreciate.

Like its US and global counterparts, the UK LEI aggregates a handful of largely forward-looking economic indicators. None are perfectly predictive on their own (or even in aggregate), but the composite tends to be a fairly accurate snapshot of an economy’s forward-looking trends. September’s was the third consecutive increase, following July’s 0.7% rise and August’s 1.2%, with six of the seven components contributing positively. The largest contributor was one of the most forward-looking: Order Book Volume—how much new business firms logged. Over the next few months, these orders turn into production, shipments, sales and exports—all of which adds to growth. Orders foretell this, and orders are rising. As is the volume of expected output—another prime contributor and evidence sales and shipments should rise in the very near term. And, as it has for months, the widening yield spread helped keep things in motion.

Exhibit 1: UK LEI Growth and Yield Spread Contribution

Source: The Conference Board, as of 11/12/2013.

The rate spread’s influence on LEI is no coincidence or, in our view, surprise. The yield spread has widened significantly (though irregularly) since markets started discounting the end of quantitative easing (QE) in the UK last year. QE depressed long-term bond rates while short rates were held at 0.5%, shrinking the gap between the two—banks’ potential operating profit (banks borrow short, lend long and live off the spread). Banks aren’t charities—they won’t take on the risk associated with a loan if the potential reward isn’t worth it. With margins narrow, they had incentive to lend only to the most creditworthy borrowers—riskier businesses and individuals were shut out. Now spreads are wider, giving banks more incentive to begin lending again.

And lending has ... stabilized—it isn’t falling, contrary to the trend during QE. But it’s still negative y/y as the BoE’s regulatory clampdown kept banks from taking advantage of the wider spread. Force banks to adopt international capital standards six years early, and they won’t lend (especially when the reward, profits, is meager). Mortgage issuance has risen nicely, but small business lending—what would most benefit the UK—remains wobbly. Now, however, regulatory clouds are clearing, and banks have more flexibility.

Even without a broad recovery in lending, M4 money supply has accelerated along with the UK economy. GDP grew—and accelerated—in three straight quarters, hitting a three-year-high 0.8% q/q in Q3. More enthusiastic mortgage issuance has spurred UK housing, where a supply shortage is prompting new construction. UK businesses are starting to invest for the first time in over a year, and retail sales are well ahead of 2012. The LEI tells us there is plenty more to come.

Even dour BoE Governor Mark Carney is starting to notice. Since taking over in July, he has made a herculean effort to talk down the recovery. Thursday, however, he announced the economy has “traction” and appears on course for even faster growth. He was even willing to cop to a potential rate hike before 2016—the target he tried (and failed) to convince investors of for months. Originally, the BoE said it would only consider raising its key interest rate after unemployment reached 7% (currently unemployment is 7.6%), which wasn’t projected to happen until mid-2016. Now, it’s projected for late 2014, about in line with what markets have suspected for months. Perhaps the BoE has finally grasped what markets already saw: The UK economy is in better shape than most headlines would lead you to believe. Few (if any) expected a broad reacceleration this time last year.

As in the UK, fundamentals say much of the world is on the verge of growing faster. So do most LEIs—nearly all are on an upswing. Forecasters largely disagree though—the IMF, World Bank, OECD and others have spent the past several months ratcheting down their global growth forecasts. But they do so based on backward-looking assessments. Forward-looking gauges like LEI tell a much different story—one we’d suggest investors pay more heed.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Corporate Information How You Benefit from Fisher Investments' Transparent Fee Structure

2026-08-04

2026-08-04 -

Corporate Information How Fisher Investments' High-Touch Service Helps You2026-08-04

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets — July 27 - July 312026-08-03

-

Expert Commentary 3 Things You Need to Know This Week | US Jobs, Trade Balance, Earnings Reports

2026-08-03

2026-08-03

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today