Personal Wealth Management / Market Analysis

How Closed Is the Reopening Trade?

A chart collection of sectors and industries most pundits assume are very reliant on reopening the economy raises the question: How much reopening isn’t baked into stock prices now?

During value’s bursts of outperformance since vaccine news broke last November, talk of the so-called reopening trade—a market rotation from industries that benefited from the lockdowns to those that suffered—has frequented headlines. So it is presently, as value categories enjoy another moment in the sun. Many, many investors see this as lasting. But markets tend to anticipate widely watched factors like this. Today, fairly few seem to acknowledge just how much reopening is already reflected in stock prices. In our view, a tour of charts of the most reopening-related categories should give proponents pause and raise the question: Exactly how much reopening is left for markets to weigh?

The reopening trade essentially presumes increasingly widespread vaccinations will drive investors to dial up expectations for profit growth among the industries hardest hit by lockdown. Those are generally economically sensitive value stocks. But, more specifically, we refer to the Airline industry, Hotels, Restaurants and Leisure firms and the Energy sector. The lockdowns designed to quell COVID’s spread devastated all of these. All would likely benefit from reopening in a major, major way relative to growth-oriented firms—some of which were COVID winners.

But here is the thing: Pretty much everyone knows that. In investing, anything widely expected is likely already reflected in stock prices to a very large degree. So, with that, consider Exhibits 1 – 4, which plot the cumulative percentage change in global value stocks and each of the three categories noted above since 2020’s pre-pandemic market peak.

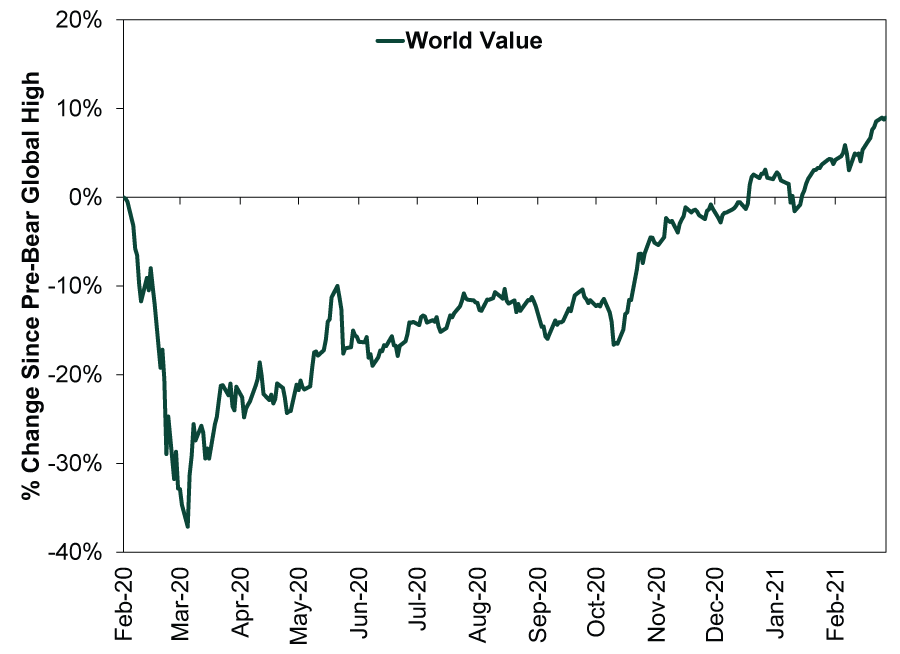

Exhibit 1: Global Value Stocks Since 2/19/2020

Source: FactSet, as of 3/18/2021. MSCI World Value Index, 2/19/2020 – 3/17/2021.

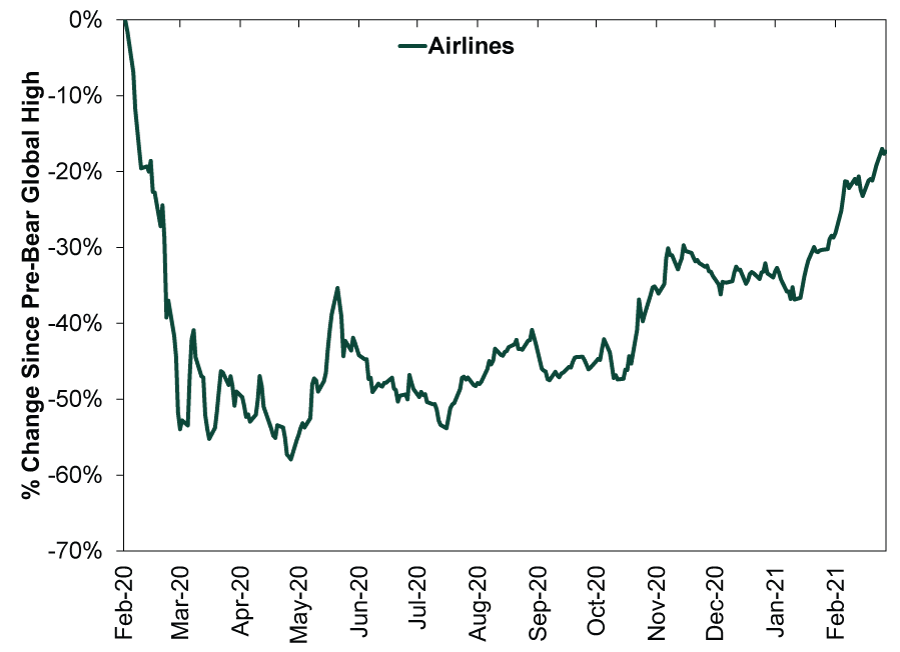

Exhibit 2: MSCI World Airline Industry Since 2/19/2020

Source: FactSet, as of 3/18/2021. MSCI World Airline Industry, 2/19/2020 – 3/17/2021.

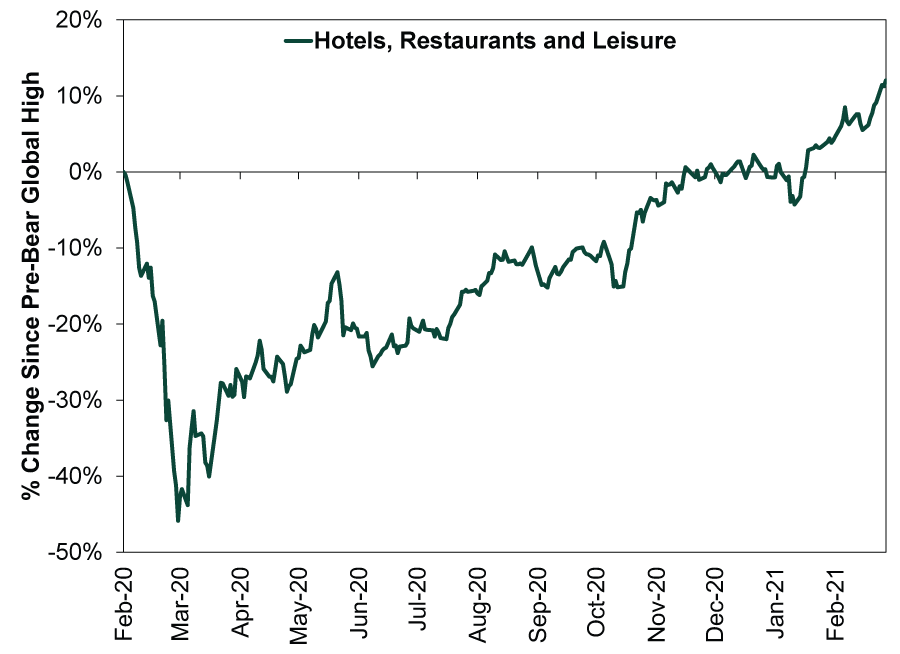

Exhibit 3: MSCI World Hotels, Restaurants and Leisure Industry Group Since 2/19/2020

Source: FactSet, as of 3/18/2021. MSCI World Hotel, Restaurant and Leisure Industry Group, 2/19/2020 – 3/17/2021.

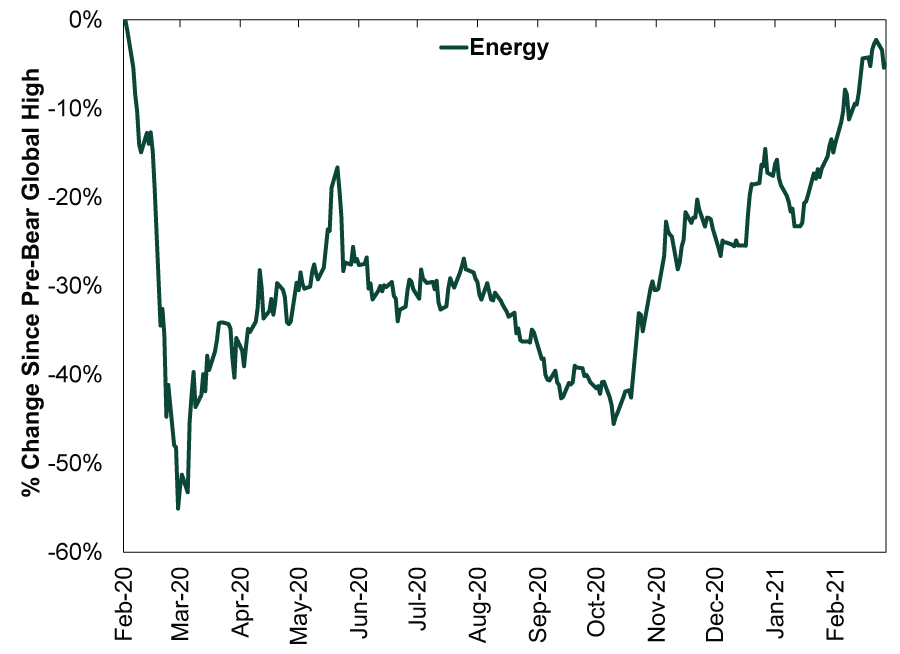

Exhibit 4: MSCI World Energy Sector Since 2/19/2020

Source: FactSet, as of 3/18/2021. MSCI World Energy Sector, 2/19/2020 – 3/17/2021.

Now, of course, this is all past performance, and past performance never predicts.[i] But reviewing this does raise an important consideration for investors buying into the reopening trade. None of the industries indicated here have recovered at an economic level. Many still confront a variety of lockdowns, demand issues and virus-related headwinds. Yet despite this, markets have seemingly anticipated a recovery, starting initially last summer and really accelerating in the fall. They are, in our view, moving on expectations and opinions of what lies ahead. They are anticipating the future for these value categories based on a plethora of theories, headlines, opinions and forecasts. Perhaps March’s Bank of America Merrill Lynch Global Fund Manager Survey captures these best. It showed a record margin of respondents in the series’ 14-year history expect value to outperform growth over the next 12 months. Add that to a plethora of headlines championing reopening as a key market inflection point and others touting value for its typical early bull market leadership and it seems clear the reopening trade isn’t sneaking up on anyone.

Unless one tries arguing markets are completely inefficient and the charts above reflect an upturn based on some other factor, it seems inarguable to us that reopening isn’t already significantly priced into these stocks. So the question now for value bulls is, to what extent do they reflect the future? Fully, partially or excessively? Additionally, and crucially, what lies beyond the reopening trade?

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis The New Tariffs in Town Are Still Old News2026-07-24

-

Expert Commentary This Week in Review | Market Volatility, Tariffs, SpaceX

2026-07-24

2026-07-24 -

Economics A Summertime Check-in on US Consumers2026-07-23

-

Expert Commentary Why Ken Fisher Is Optimistic About European Stocks

2026-07-23

2026-07-23

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today