Personal Wealth Management / Financial Planning

How to Think About Your Emergency Cash in a Low-Rate World

Low interest rates may reduce the appeal of savings accounts, but a right-sized emergency fund is still important.

For most of the past decade, interest rates have hovered near historical lows. To some, namely people who took out loans during this stretch, that has likely been a pretty positive development. But to others, it amounts to “financial repression”—a fancy way to say low rates punish savings by slashing yields well below inflation rates. Today, options to stash your cash are returning less than ever—which we think has many behaving rather oddly. Here is a broad look at various cash options—and some behaviors we think you ought to avoid.

First, to be clear, we think it is a fallacy to argue that people fit into neat and tidy categories like borrowers, savers, investors, consumers, etc. Most people are all those things at once. One trait of good investors, in our view, is that they are disciplined savers, too. They have a cash reserve to tap in case of emergencies—so that they aren’t forced to liquidate any time an unexpected expense arises. Now, this should be within reason—holding too much cash lowers your overall expected return and is a mistake that complicates many folks’ efforts to reach their financial goals. It is also not cash “on the sidelines” that you may look to deploy at some point. But having a right-sized emergency fund is important. Usually between 3 and 12 months’ (in extreme cases) cash flow needs seems sufficient, in our view. There are reasons to hold more cash than that, though. For example, if you are saving for some near-term expected expense—a down payment on a property, perhaps. But we generally think large holdings of cash warrant scrutiny.

Here is why: With interest rates as low as they are now, cash holdings—no matter where they are parked—are likely losing purchasing power to inflation, even at today’s low inflation rates. The US Consumer Price Index (CPI) rose 1.3% y/y in August—1.7% excluding food and fuel. Good luck finding that in a stable-value option like a certificate of deposit (CD), savings account or money market fund.

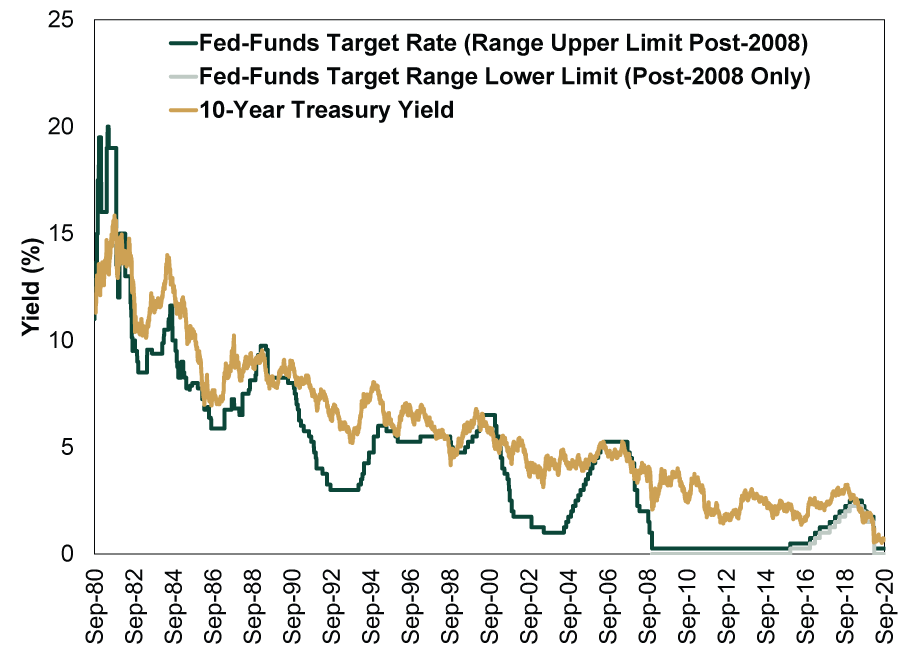

Most of these deposit accounts base their interest rate on the short-term interest rates set by the Fed. The Fed’s target range is presently 0% – 0.25% which, to state the obvious, is low. Even the 10-year US Treasury yields just 0.68%, far below CPI. (Exhibit 1) The upshot: Carrying too much cash erodes your purchasing power. This is even more true when you consider that many cash-like options pay even less than 10-year yields.

Exhibit 1: As You Know, Interest Rates Are Low

Source: FactSet, as of 9/23/2020. 10-Year US Treasury constant maturity yield, fed-funds target rates, 9/22/1980 – 9/22/2020. Note: The Fed shifted from targeting an explicit rate to a 25 basis point range on 12/16/2008.

Now, that doesn’t mean you should hold no cash. But it leads many to wonder: What should they do with their reserves? Here are some suggested dos—and don’ts.

Standard savings accounts at many banks pay very, very little. The average rate today is something like a 0.1% annual percentage yield (APY), which we hesitate to call an interest rate. Many banks are awash in excess reserves and don’t need to pay you a higher yield to attract your deposit. Yet there are options to consider. Look at high-yield, online savings accounts from one of the many purveyors. You can choose from a large array ranging from big banks to midsized and smaller firms. Rates on these still aren’t phenomenal. But in our review of eight today, we found rates ranging from 0.6% to 0.9% APY.[i] Again, these aren’t great. But no option will be hugely higher with fed-funds rates so low. The drawbacks to an online bank? In many cases, you can’t walk into a branch (to the extent you would these days anyway). Moreover, if you run into a really time-sensitive cash pinch, it can take a couple of days to move money via electronic funds transfer to your checking account. Otherwise, most of these are FDIC insured in exactly the same manner as your neighborhood bank—up to $250,000 per depositor, $500,000 for joint accounts—and subject to the same regulatory cap at six monthly withdrawals.

Some money market mutual funds can offer similar yields with a good deal of stability. But it is worth remembering that, after post-financial crisis reforms, some of these are subject to price volatility. The exception: Treasury funds, which aren’t likely to match the above yields. Furthermore, they aren’t FDIC insured, if that is important to you.

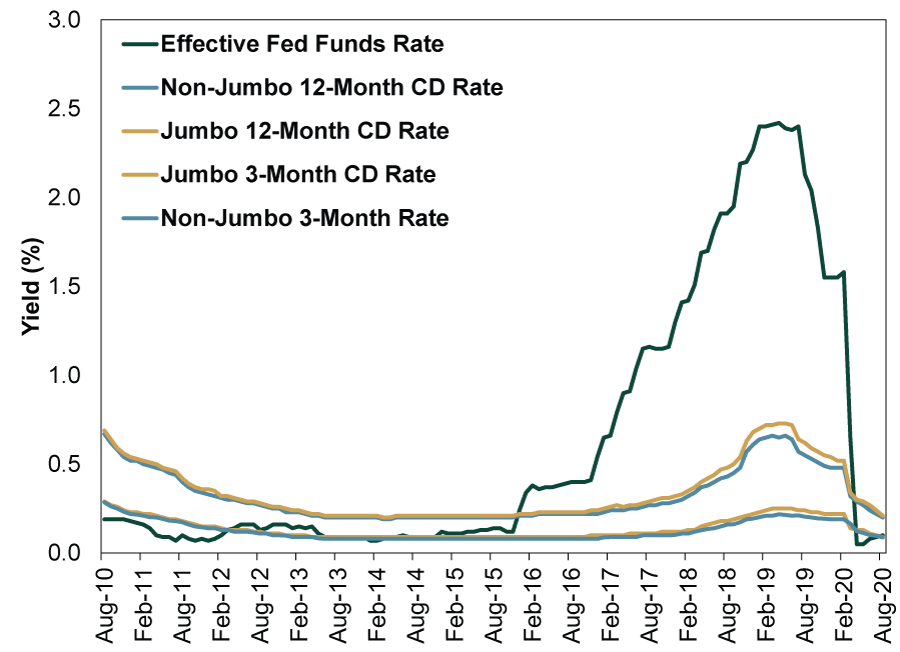

Another possible option: Certificates of Deposit (CDs). But these rates are little different—in some cases lower—than high-yield savings accounts. The difference is they lock the rate in for a specified period, so if you expect rates to go lower, this may be an option. That said, don’t expect much here, either. Exhibit 2 plots CD rates and the effective fed-funds rate (the rate banks actually are lending to one another at). CDs also may be tougher to get your money out of in a pinch—many ding you for early redemption.

Exhibit 2: CD Rates Aren’t Much Better

Source: Federal Reserve Bank of St. Louis, as of 9/23/2020. Effective fed-funds rate and national average CD rates, 3- and 12-month jumbo and non-jumbo CDs. Jumbo is defined as above $100,000.

If you start looking beyond this—at bonds or other assets—you immediately start taking on more volatility risk than may be desirable for an emergency fund or nest egg. Any bond will fluctuate in the secondary market based on interest rate moves. If they rise, prices fall, and your holdings may decline in value. Some outlandish ideas we have seen include moving into gold or Bitcoin. This is, in our view, a horrific idea for holdings that would otherwise be in cash. Both are more volatile than stocks! As another strike against Bitcoin, we frequently see reports of scams in cryptocurrencies. So, if you want our advice, don’t follow the CEO who recently moved his firm’s cash reserves into crypto on the notion real returns on cash were somehow double-digit negative.[ii] They aren’t good, but it is a stretch to think they are that bad.

We realize the returns you would get on cash are paltry now. That is the world we live in. But a right-sized, well-managed cash reserve should never have been about making money in the first place. That is where your investments come in. Savings, in our view, are a safety blanket for emergencies or money you can’t subject to volatility.

[i] We reviewed rates from Goldman Sachs’ Marcus unit, Vio Bank, Ally Financial, CapitalOne 360, Citi’s Accelerate, and American Express. As of 9/22/2020.

[ii] “CEO Says Bitcoin Is Safer After Moving Firm’s Cash to Crypto,” Olga Kharif, Bloomberg, September 22, 2020.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis The New Tariffs in Town Are Still Old News2026-07-24

-

Expert Commentary This Week in Review | Market Volatility, Tariffs, SpaceX

2026-07-24

2026-07-24 -

Economics A Summertime Check-in on US Consumers2026-07-23

-

Expert Commentary Why Ken Fisher Is Optimistic About European Stocks

2026-07-23

2026-07-23

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today