Personal Wealth Management / Market Analysis

If Europe Faces Recession, Can the US Economy Still Continue to Grow?

Troubles in Europe have raised the question, “If Europe faces a recession, can the US economy still continue to grow?” Recent data suggest it can.

The eurozone’s current economic challenges are now well known. As policymakers move to grapple with fiscal and economic weakness in the PIIGS, the region faces cuts to government spending and deleveraging across the banking system—potential headwinds to growth. As a result, estimates broadly are for slower growth in the eurozone in 2012, and it is possible individual nations or even the eurozone as a whole could fall into recession. For an American or globally oriented investor, then, a pertinent question is: If Europe faces a recession, can the US and global economies still continue to grow?” In my view, recent data suggests the answer is likely “yes.”

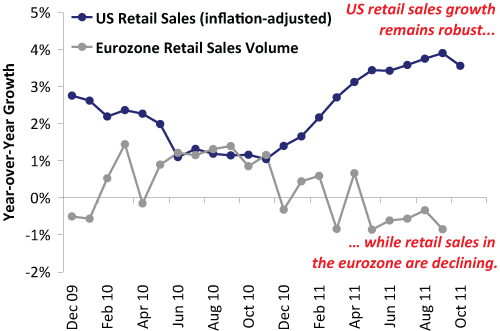

While eurozone retail sales volumes fell more than 1% year-over-year in the latest reading (the fifth consecutive decline), US sales growth (adjusted for inflation) has continually trended up over the last 12 months and was nearly 4% in the latest reading. And while Black Friday doesn’t necessarily tell the whole story for holiday shopping, initial readings from Thanksgiving weekend suggest the season is off to quite a good start—all evidence the US consumer remains resilient in the face of Europe’s problems. Exhibit 1 compares US and eurozone retail trends.

Exhibit 1: US and Eurozone Retail Sales Growth

Source: Thomson Reuters.

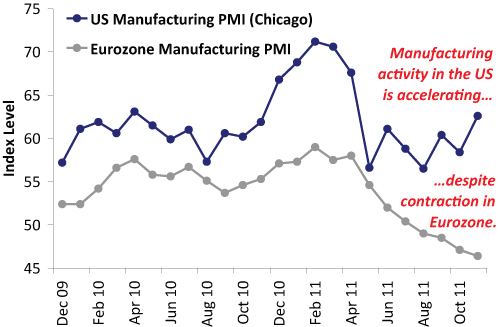

Perhaps more importantly, the US manufacturing sector appears to have shaken off last summer’s malaise. While growth rates have shown fairly typical variability, the bellwether Chicago Manufacturing Purchasing Managers Index (PMI) has been above the 50-level—indicating growth—in every month in 2011. And in November, PMI sharply accelerated to 62.6—the strongest reading since April. In contrast, November eurozone manufacturing PMI fell to 46.4—the fourth consecutive month of contraction. Exhibit 2 compares US and eurozone PMI data.

Exhibit 2: US and Eurozone PMI

Source: Thomson Reuters.

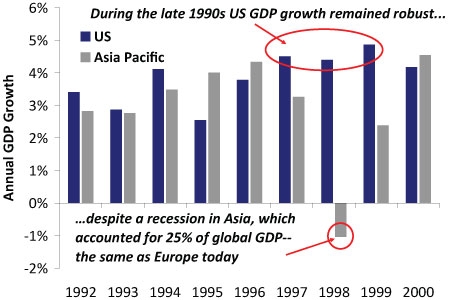

Even in an increasingly globalized world, history shows recession in one region does not necessarily spell recession worldwide. For example, 1998’s Asian Financial Crisis caused the regional economy—which was roughly 25% of global GDP at the time (nearly identical to Europe ex-UK today)—to contract by more than 1.0%. But despite widespread concerns to the contrary—and a large, nearly 20% US equity market correction largely associated with those concerns—the US economy was largely unaffected, expanding by 4.4% that year and faster the next. Now, history isn’t an exact playbook illustrating precisely how future events unfold. But it does illustrate that a regional recession, even one affecting roughly a quarter of the globe, doesn’t automatically mean global or US recession.

Exhibit 3: US and Asia/Pacific Region GDP Growth During 1998’s Asian Financial Crisis

Source: World Bank.

Moreover, because the world is increasingly interconnected, Europe just isn’t as important to the US economy as it once was. As illustrated in Exhibit 4, the share of US exports sent to the European continent are at historic lows—while US exports in total have surged over the last few years to record highs. (In Exhibit 4, we use Europe plus UK because of the longer dataset and the nations included remain constant throughout the period. A graph on the eurozone would show a shorter period and reflect increasing membership, distorting the graph.)

Exhibit 4: Europe’s Share of US Exports at a Record Low

Source: Thomson Reuters.

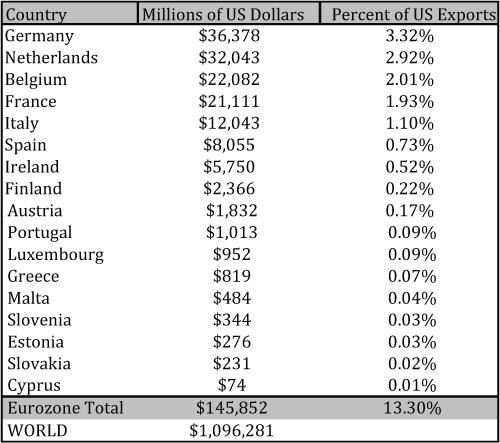

Europe as a whole now accounts for just about 18% and the eurozone about 13% of US exports in 2011 through September. Exhibit 5 shows trade to individual eurozone nations.

Exhibit 5: US Exports to the Eurozone by Country, YTD Through September 2011

Source: US Census Bureau. All figures nominal in millions of US dollars for the period 1/1/2011 - 9/30/2011. Not seasonally adjusted.

Clearly, other regions—like Emerging Markets—are now more material to US economic growth than the European Union or eurozone. And importantly, while it’s a nice shortcut to use the blanket term “eurozone” to refer to the region, it’s important to note the 17 countries do have significant differences economically. So while our demonstration is mostly discussing the area as a whole, the degree of economic problems are different country by country. That differentiation would likely exist if the eurozone overall fell into recession.

Thus, even in the event Europe does slip into recession in 2012, recent experience and data show that doesn’t necessarily imply the US or world must follow.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Economics Don’t Doubt the Old World2026-07-16

-

Market Analysis Business Friendly Bureaucracy or No, Britain is Growing2026-07-16

-

Market Analysis On the June Inflation Cooldown2026-07-14

-

Expert Commentary 3 Things You Need to Know This Week | US Inflation, China GDP, US Retail Sales

2026-07-13

2026-07-13

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today