Personal Wealth Management / Economics

Inside the Payroll Tax Hike

While many presume the payroll tax hike will weigh on household spending, January’s strong retail sales suggest consumers are rather resilient.

Higher taxes didn’t keep shoppers away from the mall in January. Photo: Spencer Platt/Getty Images.

When Congress extended several tax cuts in its fiscal cliff compromise, it let a key one expire: The two-year payroll tax holiday. Beginning January 1, every American worker’s taxes rose two percentage points, and most folks assumed lower take-home pay would weigh on economic growth in 2013. Yet thus far, data suggest the impact isn’t as bad as feared.

Recall, Congress reduced the payroll tax from 6.2% to 4.2% for 2011 to help consumers during what they viewed as a shaky economic recovery, and they extended the holiday to 2012 when economic growth remained slower than they wanted (and when their poll numbers were at all-time lows—not good for politicians facing re-election in 11 months). During the fiscal cliff negotiations, it was largely a foregone conclusion the holiday would sunset—lame-duck politicians had little incentive to extend it, and talks never got off the ground as the 2001/2003 tax cuts monopolized the debate.

Thus, most Americans entered 2013 resigned to earning less—$1,000 less per year for workers earning $50,000—with higher tax withholdings starting in January. And when polled for consumer confidence surveys, most said they planned to cut spending as a result. As usual though, what people said didn’t match what they did: Despite the higher tax, January retail sales rose 4.5% year over year. Could spending have risen more without the tax increase? Sure—very possible. But the increase argues against the tax being a major shopping deterrent.

Now, this is just one data point, and the long-term impact remains to be seen—and some outlets suggested other temporary variables overshadowed the tax hike’s drag on growth. For example, the retail industry’s fiscal calendar added an extra week to January 2013—January 2013 included the five weeks ending February 2, while January 2012 included only the four weeks ending January 28. Many observers claimed the extra week distorted the year-over-year comparisons, obscuring somewhat weaker results. However, some retailers that reported four-week and five-week sales showed strong results in both, suggesting the statistical quirk wasn’t terribly impactful.

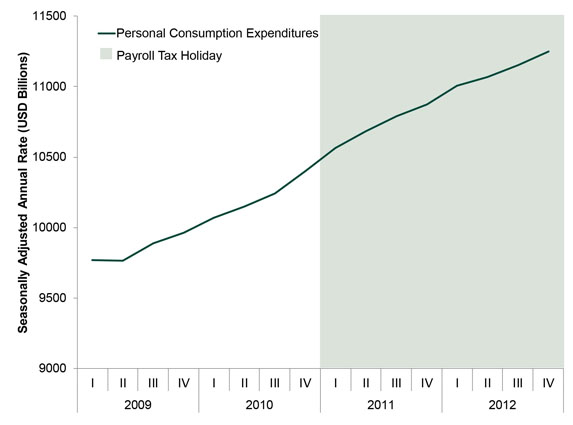

Others suggested consumers only shopped more because of huge clearance sales. And steep discounts likely did draw folks to the mall. But once there, they still spent more—not quite what you’d expect if they were in full cost-cutting mode. We suppose one could argue folks merely stocked up on cheaper goods in January in anticipation of leaner times ahead, but for that to be true, we’d need evidence consumers spent most of their payroll tax savings in 2011 and 2012. Only, they didn’t. According to Fed data, households only spent 36% of their payroll tax savings in 2011—the rest went to savings or paying down debt. Hence why consumer spending growth didn’t much change during the payroll tax holiday (Exhibit 1)—small, temporary tax adjustments in either direction typically don’t significantly change folks’ behavior.

Exhibit 1: Household Spending

Source: Bureau of Economic Analysis.

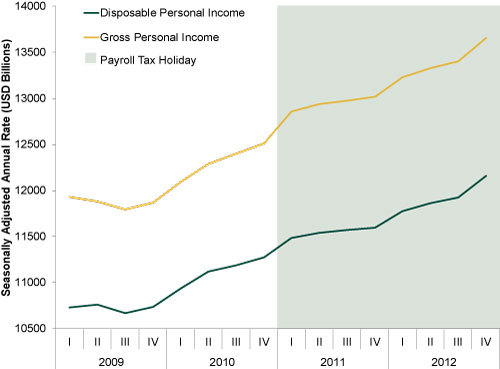

In fact, much as we love tax cuts and believe them a marginal good for the economy, it’s difficult to argue this one had much impact on economic growth. GDP, consumer spending and disposable incomes were already growing nicely before it took effect, and disposable income—the biggest determinant of spending—didn’t accelerate during the holiday. Gross personal income followed a similar trend—higher earning power, not the lower tax rate, drove disposable income gains. (Exhibit 2).

Exhibit 2: Gross and Disposable Income

Source: Bureau of Economic Analysis.

Since the holiday didn’t have a big positive impact, we wouldn’t expect its expiration to be a huge negative—with incomes trending up, over time, folks likely keep earning more despite the higher tax rate, and consumer spending should continue rising in kind (though, as always, growth rates could fluctuate).

That said, we’d much prefer a lower payroll tax. The payroll tax may be small in the grand scheme of things, but it’s regressive, and like all taxes it transfers money from efficient spenders (people) to inefficient (the government). We’d much rather have the extra cash in consumers’ (and our) pockets. But even with the small hike, overall income tax rates remain near historic lows—and that should be good enough for continued economic growth.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Quick Hit: The July Jobs Nothingburger2026-08-07

-

Expert Commentary This Week in Review | Record Highs, US Jobs, Yen Intervention

2026-08-07

2026-08-07 -

Market Analysis Western Oil and Gas Producers Are Ramping Up2026-08-06

-

Politics The Tenth Question Facing Alberta2026-08-06

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today