Personal Wealth Management / Market Analysis

Into Perspective: America and Russian Oil

Proposed legislation that would restrict US imports of Russian oil aren’t material enough to US supplies to change much.

Editors’ Note: This article addresses some political developments, so please note that MarketMinder is intentionally nonpartisan, favoring no party or any politician. We assess such matters solely for their potential economic, market and/or personal finance impacts.

While the West’s response to Russia’s war in Ukraine so far lets the world continue buying Russian energy, a bipartisan coalition led by Senators Joe Manchin and Lisa Murkowski is attempting to change this. New legislation, if passed, would ban US imports of Russian fossil fuels, including crude oil, refined petroleum products, natural gas and coal. Beltway observers think the legislation has a decent shot of passing and—while the vast majority of the country is probably behind this from a humanitarian and geopolitical standpoint—there has long been concern that the US, like Europe, now relies on Russian energy. If that is indeed true, then banning Russian oil would potentially cause a severe shortage, driving prices even higher. Yet a quick look at some US oil production data should quash this fear.

Now, much of this fear stems from politics, tied to some outlets’ over-simplified portrayals of the Biden administration’s energy policy. As the story allegedly goes, the US was energy independent[i] until January 2021, when Executive Orders canceling the Keystone XL pipeline and halting leases and permits to drill on Federal lands quashed US oil production, leading to high imports from Russia to fill the shortfall. That is the background, which we present so that all of you, dear readers, are on the same page.

We see a couple of key points countering this narrative. First, regarding Keystone XL, the Executive Order simply canceled a construction permit. The pipeline wasn’t built or operational. Additionally, its primary purpose would have been to transport Canadian crude oil to gulf refiners. It wouldn’t have done much to address the supply bottlenecks that slowed shipments of crude oil from Texas’s Permian Basin to the coastal refineries. Canceling construction did create winners and losers, but it was largely irrelevant to US drillers in the here and now, as they were already using existing pipelines and rail lines to get oil to refiners. Said differently, the absence of a future incremental addition to supply isn’t a detraction in the here and now.

Second, about those oil leases and permits. We aren’t passing any judgment at all on the merits (or lack thereof) in that decision. But the original halt was temporary and existed primarily on paper. As we wrote at the time, it didn’t prevent oil producers from utilizing land that had already been leased and permitted. It also applied to Federal land only, home to about 25% of US oil production. That is significant, but halting new leases and permitting isn’t a shutdown.

Note that the aforementioned Permian Basin, which is the US’s most productive oil field presently, isn’t on Federal or tribal land. It is private, and private lands have generated most of the growth in US oil output during the shale boom—a happy consequence of our country’s robust mineral rights. Lastly, the moratorium was only temporary, lasting until the administration could develop climate change cost criteria for evaluating whether a lease would fit with its environmental goals. That process didn’t take long, and the administration resumed awarding leases in March 2021. Over the next 11 months, the Biden administration proceeded to issue permits at a faster rate than its predecessor, with an average of about 322 per month—roughly 10% more than the Trump administration’s average.[ii]

Last week, the administration again halted lease issuance, but not by choice. Rather, a Louisiana district court issued an injunction against the climate change cost calculations it used to evaluate new leases, forcing the administration to halt all lease/permit decisions until the court approves a revised methodology. We won’t hazard a guess on exactly how and when this resolves, but the incentives point to “quickly,” given high-and-rising gasoline prices and the freeze’s high unpopularity in oil-producing states—some of which are key to this year’s midterms.

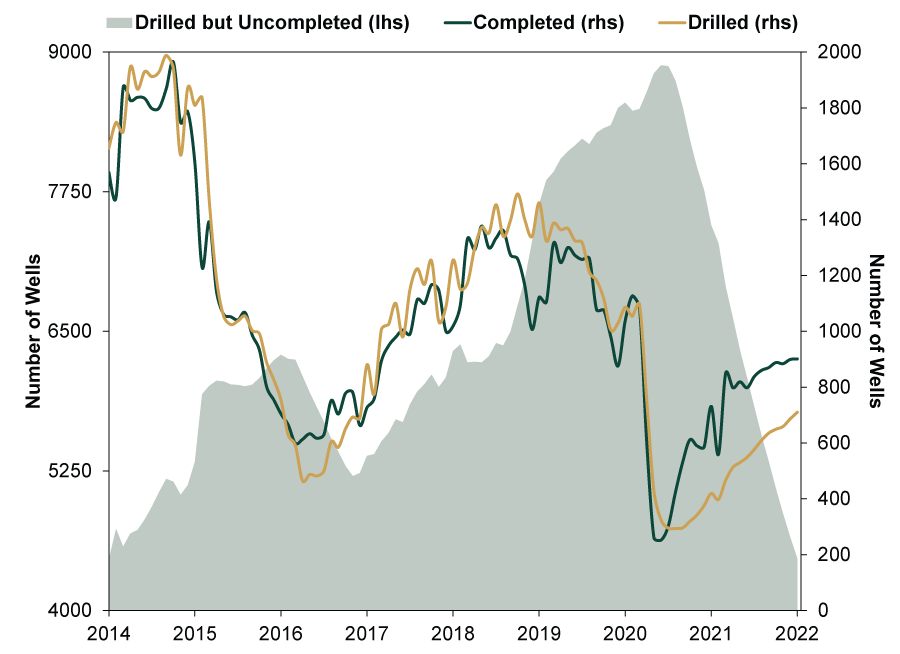

Even if it doesn’t resolve quickly, it shouldn’t slow US oil production growth materially. In 2020, oil producers hedged against President Joe Biden following through on a campaign pledge to curtail hydraulic fracturing: They amassed about 5,600 new permits, which would have been sufficient to cover anticipated drilling activity over a four-year term.[iii] Add to that the thousands of permits secured over the last year, and there is a huge backlog of permitted-but-not-drilled sites. One way to see this is the slow recovery in production despite the record-high issuance. (Exhibit 1)

Exhibit 1: Despite a Wave of New Permits, US Oil Production Is Recovering Slowly

Source: US Energy Information Administration, as of 2/25/2022.

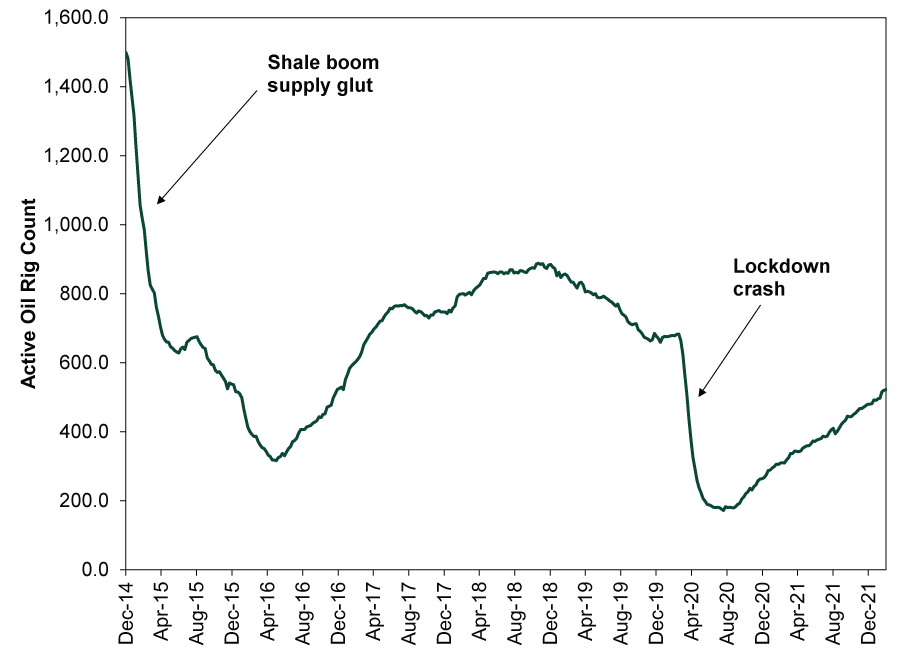

Note, too, that declining US output was tied not to the administration change, but to COVID. Lockdowns destroyed demand, sending oil prices to rock-bottom levels and forcing US producers to cut back and focus on servicing debt instead. As the economy reopened, production slowly recovered in sympathy with rising prices. That is econ 101—high prices encourage more production. But companies moved gradually, remembering the consequences of rapid debt-fueled expansion during the shale boom. When they overshot and created a supply glut, plunging oil prices in 2014 – 2016 made debt difficult to service, creating a mini debt crisis among producers. They have largely worked through those issues and are now focusing on quality, not quantity, but they do have the bandwidth and flexibility to increase production. Just look at oil rig counts, which have more than doubled since late 2020.

Exhibit 2: Active US Oil Rig Count

Source: FactSet, as of 3/3/2022.

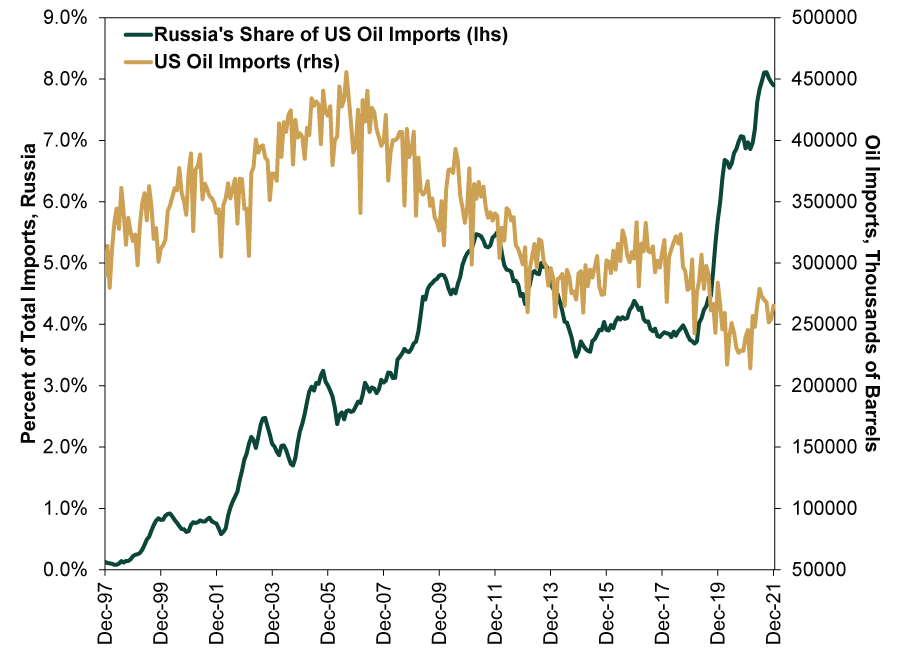

Furthermore, we don’t get all that much oil from Russia. In the 12 months ended in December—the latest data available—the imports from Russia averaged about 8% of total US imported oil and oil products.[iv] To be fair, that is the highest 12-month share in the last 25 years. However, overall US oil and oil products imports are down significantly from the mid-2000s’ highs, and finished 2021 hovering around pre-pandemic lows. (Exhibit 3) Europe is much more reliant on Russia than the US.

Exhibit 3: US Total Oil Imports and Russia’s Share

Source: US Energy Information Administration, as of 3/3/2022. December 1996 – December 2021.

So whether Congress makes a ban official or private companies keep self-sanctioning and avoiding Russian crude voluntarily, it shouldn’t have an outsized impact on US supplies. With or without readily available Russian oil, US producers were recovering from the lockdown sucker punch and ramping back up. Today’s elevated prices probably give them an extra boost, which should help more black gold gush from American wells a lot faster than many seem to expect.

[i] Energy independence is a myth. Oil and gas prices are set globally, regardless of whether we “need” to import oil or not.

[ii] Source: US Bureau of Land Managmeent, as of 2/25/2022.

[iii] Source: US Bureau of Land Management, as of 2/25/2022.

[iv] Source: US Energy Information Administration, 12-month moving average of US oil and oil products imports from Russia, January 2021 – December 2021.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Economics Q2 US GDP’s Stealthy Strength2026-07-31

-

Expert Commentary This Week in Review | Fed Meeting, US GDP, Eurozone GDP

2026-07-31

2026-07-31 -

Market Analysis Don’t Fret the EU’s Low Summertime Gas Storage Levels2026-07-31

-

Economics On Fires and GDP2026-07-30

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today