Personal Wealth Management / Economics

Japanese Godzilla QE Shows Fed Mothra Feckless

If QE is the bee's knees, why did no one tell the Japanese?

On November 3, 2010, the world was forever changed: QE2 became more than an ocean liner. The Fed announced another round of its supposed monetary stimulus, known as quantitative easing, and presto! QE2 became code for more Fed bond buying. Since then, we have seen hundreds of articles arguing this and many other versions of QE globally fueled this bull market. They still pop up almost daily, as QE continues in the eurozone, UK, Japan and Sweden. Any time US markets slow down, we're warned more stimulus might be necessary. We've long said the opposite-in our view, markets are rising despite QE, not because of it. While that's just our opinion, it's fairly easy to test. Just ask: If QE is really rocket fuel, then why isn't the country with the most QE the world's top performer?

We refer, of course, to Japan. Once one of the world's fastest-growing economies. The dynamite nation that was going to own all of us in the 1980s, with its mega conglomerates the world's envy. Then its bubble popped, and an infamous "lost decade" of stagnation and deflation followed. The Bank of Japan invented QE in 2001, used it until 2006, and all it got was Lost Decade: The Sequel.[i] Then came the global financial crisis and a slow Japanese recovery, so the BoJ tried again, resurrecting QE in late 2010, but with a twist. In addition to buying Japanese Government Bonds, better known as JGBs, the BoJ also bought some REITs, equity ETFs and other so-called "risk assets." Over the next six years, they expanded the program multiple times and added a few letters to the acronym. Now it's the world's biggest, befitting of the nation that gave us Godzilla and giant anime robots: ¥80 trillion in annual asset purchases, indefinitely, or 16.6% of nominal GDP.[ii] US QE, by comparison, was just 6.1% of GDP annually at its apex.[iii] The eurozone's QE program is presently 9.2% of GDP.[iv] The UK's, at its peak, was 6%.[v]

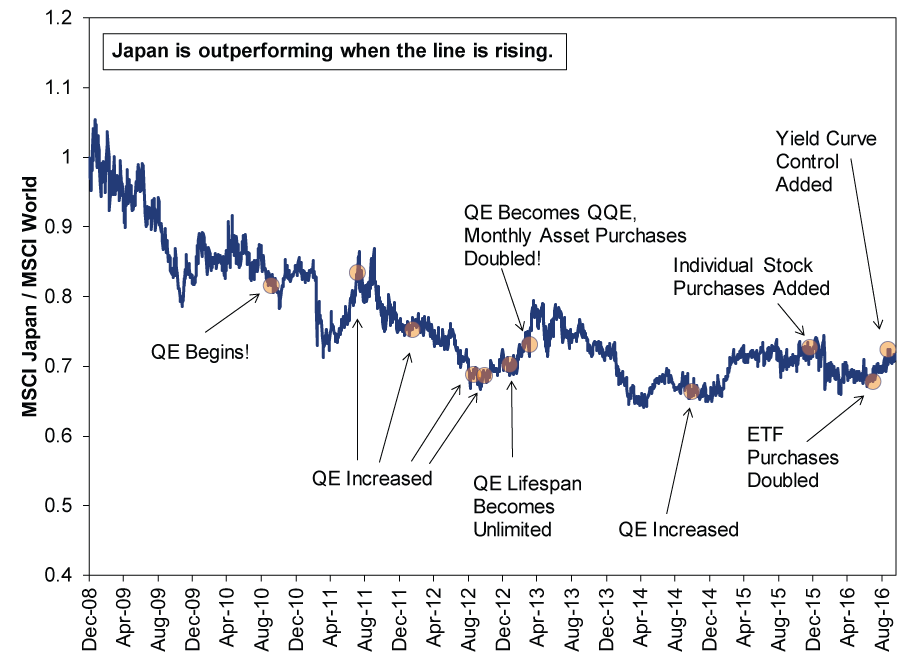

If QE is indeed magical for stocks, then it should follow that Japanese stocks soared high above all other developed nations, getting higher and higher with each QE increase. More mojo! Yet, as Exhibit 1 shows, that isn't what happened.

Exhibit 1: Japanese QE and Relative Performance

Source: FactSet, as of 10/20/2016. MSCI Japan and MSCI World Index returns with net dividends, 12/31/2008 - 10/19/2016, indexed to 1 on 12/31/2008.

Since its QE program began, Japan has underperformed the world.[vi] In dollars, the MSCI Japan is up 41.3% since that fateful day, 10/5/2010, while the MSCI World is up in 61.3%. Some point to Japan's higher yen-denominated returns, 75.8%, but world stocks' 101% gain in yen still dwarfs that. The best developed-world country during this stretch? New Zealand, with a 105% gain and not one drop of QE. Sure, the MSCI New Zealand is tiny and has only seven stocks in five sectors, but it's illustrative. The Kiwis didn't need QE. Neither did Denmark (77.2%) or Hong Kong (45.9%-underperforming the world but beating Japan).[vii]

We can use the same approach to test the claim that QE fueled America's economic expansion. If big QE means big growth-or heck, even just plain growth-then Japan should top the GDP growth leaderboard. Instead, it suffered three recessions and is flirting with a fourth. Now, we aren't saying QE caused all of those. But if it were truly magic elixir, it would have helped Japan overcome the sales tax hike in 2014. Or the 2012 malaise. (We'll grant that the Great Tohoku Earthquake and tsunami probably would have caused a recession in 2011 either way.)

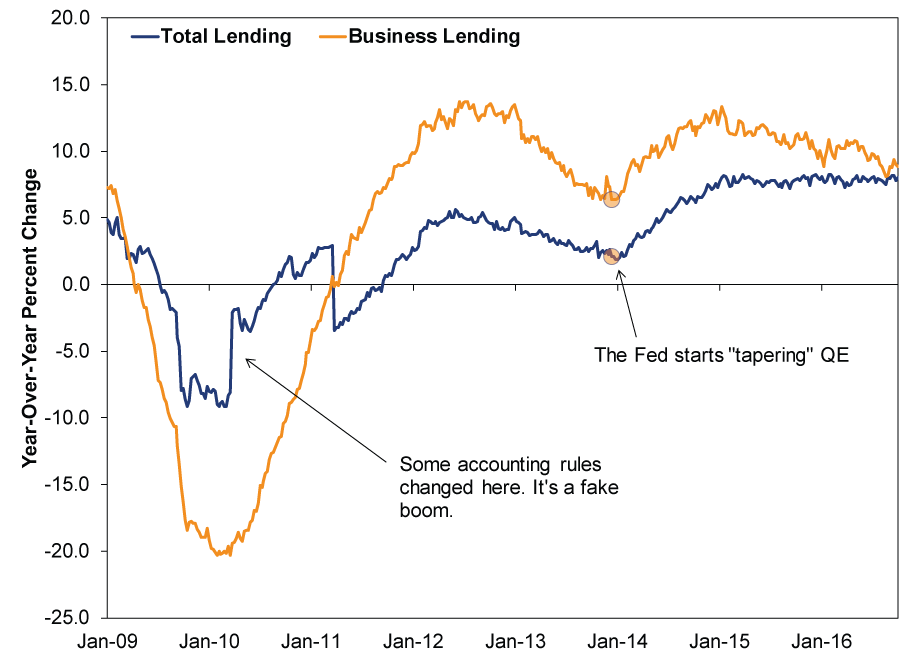

Here's some more evidence this bull market and expansion exist despite QE, not because of it. If US QE were stimulus, it would have shown up in America's economy through faster loan growth. But all it did was sit on bank balance sheets. Not as required reserves, which back loans, but as excess reserves gathering dust. If it were actually stimulus, required reserves would have jumped as banks lent more enthusiastically. Instead, loan growth sagged. Perhaps it's a coincidence, but loan growth really got cooking at the end of 2013, when the Fed finally started reducing bond purchases.

Exhibit 2: QE Winds Down, Lending Heats Up

Source: St. Louis Federal Reserve, as of 10/20/2016.

None of this should surprise when you think about this from the perspective of Milton Friedman's ghost. We have over 100 years of theory, tests and data showing economies grow best when yield curves are steep. To understand why, think like a banker. Banks borrow from all of us depositors at short-term rates, and they lend at long-term rates. The gap between the two-long rates minus short rates-is their potential profit on the next loan made, also known as their net interest margin. Banks are for-profit businesses, not white-hat charities, so they base lending decisions on risk and return. When yield curves are flat, profits are small, so the only people who can get loans are those who don't really need them. When yield curves are steeper, profits are bigger, so banks can lend to a wider swath of households, consumers and businesses. When they lend more, broad money supply grows faster, and the economy has more fuel.

QE flattened the yield curve. It's simple supply and demand. When central banks buy long-term bonds, they take supply off the market, forcing other investors to compete for a smaller pool of securities. Investors thus bid bonds higher, and because yields move opposite bond prices, they fell. Meanwhile, short rates were fixed near zero. Ergo, flatter yield curve, sadder banks.

That is QE's legacy everywhere it has been tried-America, Britain, Japan and most of Europe. All saw yield curves flatten during QE. In the US and UK, curves steepened after it ended, and most economic data firmed up. Oh, and since the Fed announced the Great QE Taper on December 18, 2014, US stocks are beating the world. Returns aren't rip-roaring for anyone, as we had that correction from May 2015 through mid-February, but they're positive, and QE-free America is near the front of the pack.

[i] The Lost Decade Strikes Back? Revenge of the Lost Decade? Return of the Lost Decade? The Lost Decade Awakens? And to prove that we can do more than rip off the Star Wars saga, Son of Lost Decade?

[ii] Bank of Japan and Japan Cabinet Office, as of 10/20/2016.

[iii] Federal Reserve and Bureau of Economic Analysis, as of 10/20/2016.

[iv] European Central Bank and Eurostat, as of 10/20/2016.

[v] Bank of England and Office for National Statistics, as of 10/20/2016.

[vi] You could type the same sentence for the ECB, which launched QE in early 2015.

[vii] Everything in this paragraph comes from FactSet, as of 10/20/2016, and displays returns with net dividends from 10/5/2010 - 10/19/2016.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis The New Tariffs in Town Are Still Old News2026-07-24

-

Expert Commentary This Week in Review | Market Volatility, Tariffs, SpaceX

2026-07-24

2026-07-24 -

Expert Commentary Why Ken Fisher Is Optimistic About European Stocks

2026-07-23

2026-07-23 -

Economics A Summertime Check-in on US Consumers2026-07-23

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today