Personal Wealth Management / Economics

Jawboning, Speculation and Hot Air

With the Fed holding its annual Jackson Hole symposium, talk of QE3 is escalating.

Jackson Hole: 51 weeks of the year, it’s a sleepy, Wyoming resort town, but this week, thanks to the Fed’s annual symposium, it’s the center of the monetary universe. Last year’s summit was the setting for Ben Bernanke’s initial rumblings about QE2, and there’s much chatter QE3 could be introduced during his Friday keynote.

Right now, handicapping whether QE3 will materialize would be a highly speculative exercise. The Fed isn’t a market-based organ. Central banks are monopolies, run by a handful of people; sometimes those people make smart decisions, but sometimes they don’t.

Some point to recent slowness in some readings as evidence the Fed needs to intervene, but in our view, the soft patch has nothing to do with a lack of monetary stimulus—rather, it looks like a fairly normal deceleration, which is typical a year or two into an expansion.

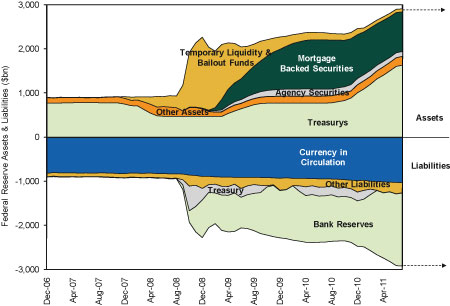

Though we don’t think QE3 is necessary (we just think it’s largely unnecessary, as we did QE2), it’s also not a recipe for disaster. The US economy was growing just fine when QE2 was announced and then implemented (and the market had had a historic boom off the March 2009 bottom). QE2 did likely provide a sentiment boost when it was announced in 2010, but its fundamental impact was seemingly limited given most of the money the Fed pumped went right back to the Fed, on deposit as excess reserves. (See Exhibit 1.) Why?

Exhibit 1: Fed’s Balance Sheet

Source: Federal Reserve, as of 8/22/2011

In the years before 2008, those excess reserves paid nothing. But in one financial crisis-born measure, the Fed began paying banks to hold excess reserves. That rate might be a paltry 0.25%, but that’s roughly equal to prevailing very short term rates, and it’s totally risk-free. In our view, this in no small measure explains the massive size of excess reserves at the Fed. So if QE3 happens, the outcome will probably be the same on both fronts absent other policy changes, like reducing interest paid on excess reserves.

In our view, the benefit of QE3 would mostly be another near-term sentiment boost. Which isn’t immaterial, but sentiment is also fleeting. Keep in mind, too, each new chunk of money the Fed prints increases the risk of inflation down the road. (Which would of course be contingent to a large degree on more of that money moving through the economy instead of sitting parked at the Fed.)

Talk of QE3 may also just be jawboning—a legitimate central banker tactic. After all, Bernanke’s up for reappointment in 2013. Thus, he could do something that makes more political than monetary sense—and that thing might be appearing to “do something.” Even if that something is rather ineffectual. (Heck, maybe in his mind better if that something is ineffectual because a major policy error would mean he’s updating his resume come January 2013.) Either way, expect more hot air than normal from the environs of Jackson Hole.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Pumping Up the Yen?2026-07-17

-

Market Analysis Business Friendly Bureaucracy or No, Britain is Growing2026-07-16

-

Economics Don’t Doubt the Old World2026-07-16

-

Market Analysis On the June Inflation Cooldown2026-07-14

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today