Personal Wealth Management / Economics

Manufacturing Innovation

The Institute of Supply Management released its Index for April, but don’t let the numbers fool you—domestic manufacturing is making a surprising comeback.

The April ISM Manufacturing Index clocked in at 50.7 on Wednesday—a bit slower than March’s 51.3 the month before, but expanding. Aside from fleeting contractions that really look like data variability in 2011 and 2012, US manufacturing has grown at a healthy pace since 2009. April’s acceleration in production and new orders suggests there’s more upside to come. In fact, despite years of chatter about the supposed death or decline of US manufacturing, the sector’s enjoying a renaissance as more firms seek to capitalize on the US’s efficiency.

It’s a little-noticed fact that US manufacturing output has grown steadily over time and is just 3% below all-time highs logged in 2007. Shrinking manufacturing employment often takes center stage, with folks bemoaning manufacturing jobs shipped overseas to countries with cheaper labor, like China. And no doubt, some jobs have moved elsewhere—but this phenomenon is often overstated. And in many ways, it’s not the point. After all, manufacturing jobs aren’t a leading indicator of the economy and they’re not really much of a barometer of the industry’s health. In many cases, jobs were lost to productivity gains as firms implemented time- and labor-saving technologies. In large part, that’s how manufacturing output kept growing despite falling manufacturing employment.

The US has always been an attractive place to do business. Structurally, we have sound and stable legal and political systems, well-established property rights, a wealthy base of potential consumers and more. But the relative attractiveness of the US seems to be on the rise lately for manufacturers to set up shop.

For those jobs that did move due to lower wages, countries like China aren’t quite as attractive manufacturing hubs as they used to be. Wages have risen quite a bit, and the gap between labor costs in some developing-world manufacturing countries and the developed is shrinking. (While the low-wage edge diminishes, it boosts their domestic consumption—a key aim of China’s government). Compounding matters, international shipping costs are increasing, while US energy prices are relatively cheap thanks to the ongoing shale gas boom. The overall cost of producing in the US is now pretty competitive globally.

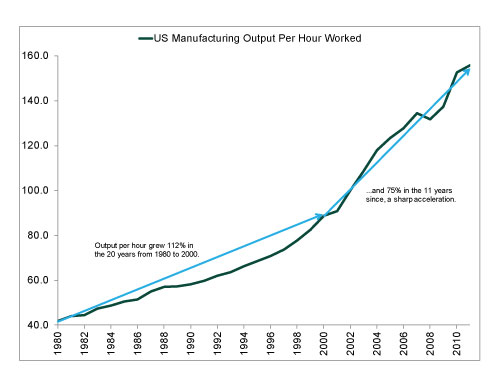

But perhaps the key reason US manufacturing’s competitiveness is rising is also the major culprit for the long-run trend of reduced manufacturing payrolls: its astounding productivity. US factories have adopted a ton of efficiency-enhancing technology over the years. According to the US Bureau of Labor Statistics, manufacturing output per hour worked grew 112% between 1980 and 2000. The growth rate has quickened since—rising 75% in just the last 11 years. (Exhibit 1) Those efficiency gains continued apace in Q1, when manufacturing productivity rose a sharp 3.8%, outstripping the broader economy’s 0.7% increase.

Exhibit 1: US Manufacturing Output per Hour (Indexed to 100 at 2002)

Source: Bureau of Labor Statistics.

Advancements in automation and factory equipment help firms get a whole lot more bang for their buck. That’s huge for firms trying to gain and maintain a competitive advantage.

Now, because firms are doing so much more with less, we likely won’t see astronomical manufacturing jobs gains as more production returns to the US. But a new surge of manufacturing can foster something equally important—innovation. Manufacturing companies have a huge incentive to develop or invest in new technology. When companies can produce more in less time, profits go up! That’s why manufacturing firms tend to spend heavily on R&D. In 2012, the US spent more on R&D than all of Europe combined, twice as much as China and nearly three times Japan. And US manufacturers are by far the biggest spenders, according to a survey published in R&D Magazine. And it’s a virtuous cycle. As firms get more efficient and profit margins grow, they have more capital to invest in better equipment or more research and development, which has big downstream economic effects. For example, money spent on R&D often goes to the scientific and high-tech communities, driving growth. New factory equipment needs highly skilled people to service it—hence, a source of demand for workers. Should that demand be unable to findqualified supply in the short term, it's likelylonger run wages for those positions would rise—attracting more workers, creating training programs, etc.

US manufacturing is not only healthy, it seems to have a bright long-run future ahead. That might be harder to see—the likelihood a factory employing tens of thousands of workers opens, creating a company town is probably lower than in the past. But the evolution of the economy—and the nature of manufacturing itself—shouldn’t be summarily dismissed.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Economics Quick Hit: Durably Broad-Based Growth2026-07-29

-

Market Analysis On the Chop in the Oil Market2026-07-29

-

Politics Takaichi Raises Japan’s Wall of Worry2026-07-27

-

In The News Why Kevin Warsh should think twice about hiking interest rates — even as anxiety over the Iran war grows2026-07-27

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today