Personal Wealth Management / Market Analysis

Market May I?

Markets don’t move on Mayan calendars, astronomy or folklore—so we have a hard time seeing why they should move just because it’s May.

May’s upon us, and so are numerous articles debating the benefits of “sell in May.” In the earliest form we can find, the saying went, “Sell in May, and go away; come again on St. Leger’s Day.” It originated in London—then the economic center of the world—at a time when markets would virtually shut down in the summer, while brokers and other financial professionals vacationed. Supposedly, the end was tied to a mid-September horse race (the St. Leger’s Stakes). As a result, trading volumes were much thinner. Thinner volumes can mean less liquidity, and less liquidity can mean tougher price discovery—hence, more volatility. But nowadays, liquidity isn’t much a problem at any time of the year, thanks to new technologies and growing markets. Yet “sell in May” continues to garner headlines.

The old adage that may have started with May as an exit and St. Leger’s Day as a reentry point has evolved to mean ... well ... we don’t exactly know what. You see, adherents seem to have many different ideas of the timing. And “sell in May” itself doesn’t lay out when the actual selling should occur—May Day? May 31? Or sometime in between? Even if an investor figures out when to sell, there’s conflicting advice about when to buy back in. Some advocate September, others October, some a strict six months and still others November.

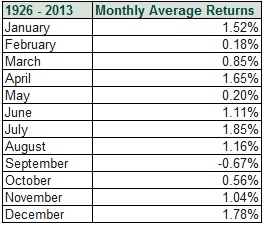

Ultimately, this debate stems from claims summer(ish) average returns are worse than winter(ish) returns. And there’s a grain of truth to that: returns from May to October have been slightly lower than returns the rest of the year ... but, even with big down years dragging down the averages for some months, cumulative returns in each half of the year were positive. Taken on a monthly basis, only average returns for September are negative, and not by much. (And that fact is skewed by a few big bad Septembers dragging down the average. A function of math, not calendar causation.)

Exhibit 1: Monthly Average Returns

Source: Global Financial Data, Inc.; S&P 500 Total Returns 12/31/1925 - 3/31/13, as of 5/8/13.

Yet some may argue corrections in the last three years around the summer months are fine evidence “sell in May” works. We’d argue otherwise. Had you sold in May 2010 and returned to markets in, say, October, not only would you have still been in the market for the beginning of that year’s correction (04/15/2010), you’d have been out of the market for the three months of a sharp snap higher after the correction’s bottom (07/05/2010). 2011’s correction may fit the adage best. Its pre-correction high was hit in April and selling ran until early October. 2012’s correction, however, didn’t, lasting only from 04/02/2012 to 06/04/2012. We’ve never heard anyone argue re-entry should be in early June. And just three years earlier—2009—had huge positive returns during the summer months. So in reality, during this bull market, you could say summer’s been weak in one of four years. In two of the others, corrections began before May and the trough—theoretically, the best reentry point—was during the period the adage says to be out.

If you exited stocks attempting to time this, you needed to reenter at some point before St. Leger’s Day (in mid-September). If not, the market had topped earlier highs and you’d missed successive months of 7.5%, 1.35% and 2.5% positive returns.i Selling in May is little more than playing a game of short-term market timing—a difficult thing to do, especially when trying to time the right exit and entry points. We’re not aware of anyone who has a track record of repeatedly timing corrections. Especially when there’s really no discernible piece of unique knowledge you have to guide those choices.

The bottom line is no matter how tempting or rhymey a seasonal saying seems, selling based on a calendar—information known to nearly anyone in the western world—just isn’t a good investment strategy. Rather, investors should look to fundamentals to make investing decisions—like a strong US private sector, healthy corporations, a more stable eurozone and overall global growth. Those are much more influential to market returns than a fuzzy, old, calendar-based adage with a nifty rhyme.

i Source: Bloomberg. MSCI World Total Returns from 06/04/2012 – 06/30/2012, 06/30/2012 – 07/31/2012, 07/31/2012 – 08/31/2012.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary 3 Things You Need to Know This Week | Q2 Earnings, ECB Meeting, Trump Accounts

2026-07-20

2026-07-20 -

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—July 13 - July 172026-07-20

-

Expert Commentary This Week in Review | US-Iran Conflict, US Inflation, New UK Prime Minister

2026-07-17

2026-07-17 -

Market Analysis Pumping Up the Yen?2026-07-17

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today