Personal Wealth Management / Economics

Mathflation

January's CPI surge is funky math, not something sinister.

It's baaaaaaaaaaaack! The US inflation rate hit 2.5% y/y in January, the fastest since 2012 and a big jump from December's 2.1%. Much of the media coverage took the news in stride, a refreshing sign of sentiment's continued thaw. But there was still a bit of handwringing, with some articles warning of mounting inflation pressures and others fretting the Fed is behind the curve, setting stocks up to suffer as inflation erodes future earnings. We think the more measured commentary has it right. January's jump isn't the sinister erosion of purchasing power-it's just math, an aftereffect of what oil prices did early last year.

At its core, the inflation calculation is pretty simple: Divide current prices by prices a year ago, then subtract 1 and multiply by 100 to convert to percent. When people think about inflation, they tend to overemphasize current prices, while forgetting the denominator is volatile, too-and that sometimes it can have a lot more influence on the inflation rate than current prices. In the UK, for example, January's CPI actually fell -0.5% from December, but the annual inflation rate sped to 1.8% from December's 1.6%, because CPI was really low in January 2016. Econ nerd-types call this a distorted base effect.

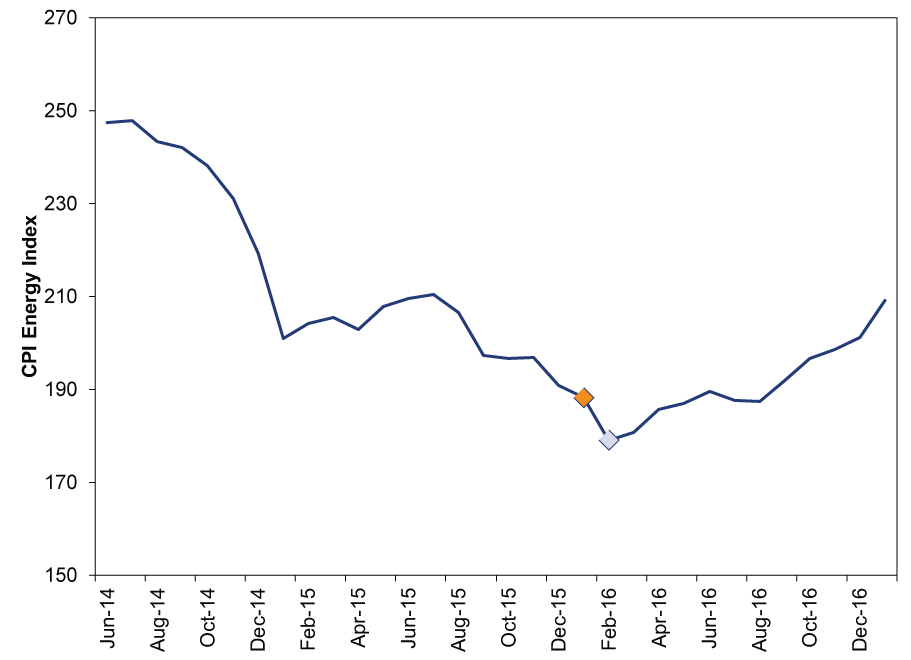

The quirks behind US inflation in January aren't quite that extreme, but there is a similar base effect at work. It's most visible in energy prices, which were the primary force behind January's jump. Exhibits 1 and 2 show two ways of viewing this-WTI Crude Oil Prices and the energy component of CPI, respectively. Both hit new lows in January and bottomed out in February (colored orange and light blue, respectively), making the denominator for January 2017's year-over-year calculation very low.

Exhibit 1: WTI Crude Oil

Source: FactSet, as of 2/15/2017. WTI Crude Oil daily spot price, 6/31/2014 - 1/31/2017.

Exhibit 2: CPI Energy

Source: FactSet, as of 2/15/2017. CPI Energy monthly index level, June 2014 - January 2017.

When energy prices plunged in 2014 and 2015,they dragged CPI down-not just in America, but globally. CPI even turned negative at points, causing some handwringing about deflation. But that was always a misnomer. Prices overall weren't falling. Rather, a drop in one part of the CPI basket was huge enough to outweigh modest price rises elsewhere.

Because energy and food prices are so volatile, most countries also track "core" CPI, which excludes them. The exact definition varies from country to country. In Japan, "core" simply excludes food, while "core-core" excludes both. The UK and its erstwhile EU bedfellows also exclude alcohol and tobacco prices, giving us the chance for the occasional ginflation pun. Core inflation tends to be far more stable than headline CPI, which makes it a more useful barometer for gauging price trends in the "inflation is always and everywhere a monetary phenomenon of too much money chasing too few goods" sense. Sometimes this creates a backlash, as people obviously spend money on food and gasoline, and big changes there can pinch, but inflation was never meant to measure cost of living. Rather, it's a barometer of whether money supply is growing too quickly.

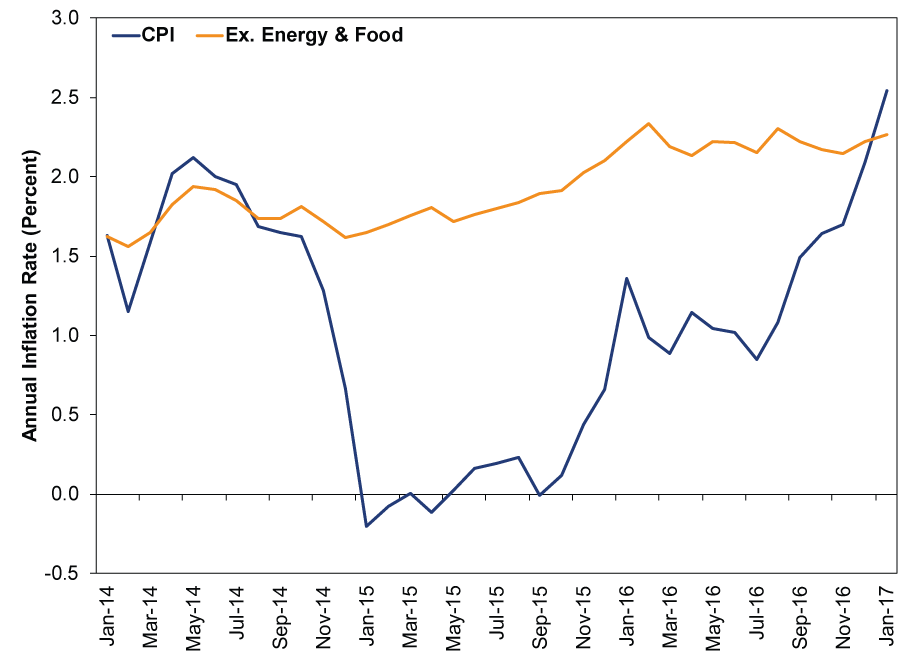

When falling oil dragged US CPI below zero, core CPI stayed largely stable and even accelerated a bit. When oil flipped from the minus column to a plus, and CPI jumped, core CPI was basically flat. Since December 2015, it has wobbled between 2.1% and 2.3%, which happens to be January's reading. Viewed this way, inflation isn't suddenly surging, and January just extends the status quo.

Exhibit 3: US Headline and Core CPI

Source: FactSet, as of 2/15/2017. CPI and CPI Ex. Energy and Food, January 2014 - January 2017.

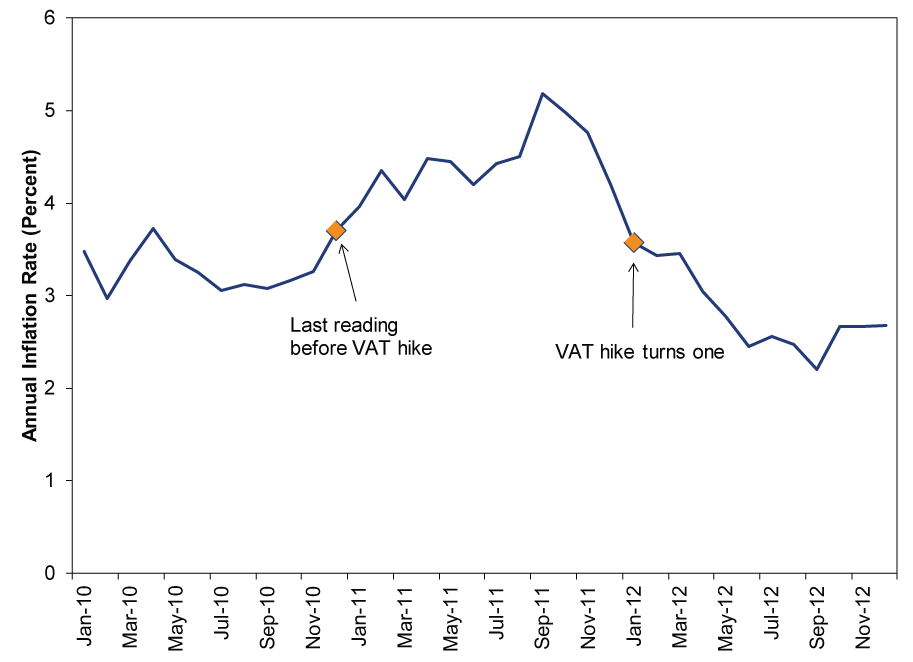

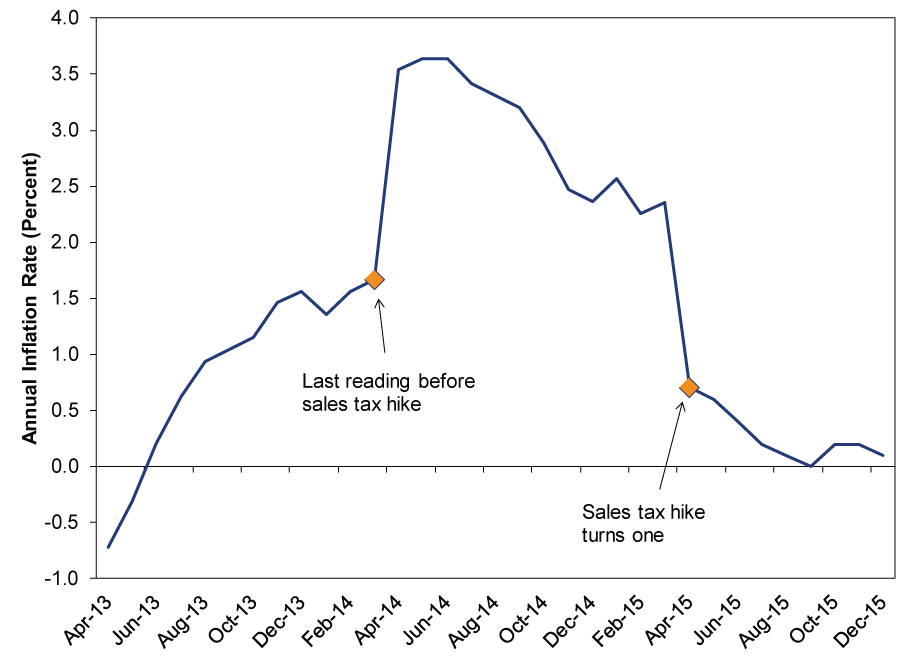

This isn't the first time one-off factors have skewed inflation rates, making it harder to see underlying trends. In January 2011, the UK hiked its value-added tax (VAT), distorting CPI. (Exhibit 4) The higher VAT entered the year-over-year calculation that January and stayed there all year. Even though taxes didn't rise every month, because prices a year ago were pre-tax hike, it created the illusion of steadily rising prices and fed hot inflation fears. But in January 2012, it was out-the base comparison, January 2011, already reflected the higher VAT. Inflation calmed, and so did the fear. Similarly, when Japan hiked its sales tax in April 2014, it artificially boosted CPI for a year, making it look like the BoJ was finally on the verge of meeting its inflation target. Spoiler alert: It wasn't. (Exhibit 5)

Exhibit 4: UK CPI Before, During and After the VAT Hike

Source: FactSet, as of 2/15/2017. UK CPI, January 2010 - December 2012

Exhibit 5: Japan CPI Before, During and After the Sales Tax Hike

Source: FactSet, as of 2/15/2017. Japan CPI, January 2014 - December 2015

Don't let math trick you. Inflation has been benign for years and remains so now. It won't shock us if math plays the same tricks with this month's CPI when it eventually comes out, as oil bottomed a year ago Sunday and oil is up a tad so far in February. Maybe when it comes out we'll write an article called "Inflation Two: The Wrath of Math."[i]

For stocks, this is all just amusing noise. Where oil prices are now relative to a year ago doesn't say anything about corporate earnings a year or two from now. Stocks are forward-looking, and over the foreseeable future, inflation doesn't look poised to bite. Broad money supply hasn't suddenly surged. Loan growth actually cooled off a bit last year after the yield curve flattened. Fed rate moves seem more or less fine thus far, and markets have already proven they don't mind modest inflation.

[i] Perhaps followed this summer by "Dude, Where's My Inflation" if oil stays stable and energy's year-over-year change is flattish.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Pumping Up the Yen?2026-07-17

-

Market Analysis Business Friendly Bureaucracy or No, Britain is Growing2026-07-16

-

Economics Don’t Doubt the Old World2026-07-16

-

Market Analysis On the June Inflation Cooldown2026-07-14

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today